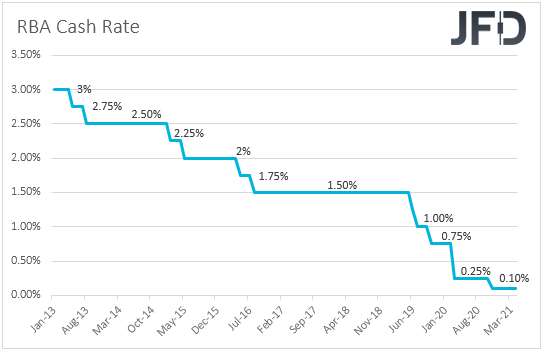

Following the RBNZ last week, this week, it’s the turn of the RBA to decide on monetary policy. We don’t expect any change, but it would be interesting to see whether they are still willing to expand their bond purchases in July. As for the data, Eurozone’s inflation and the US jobs report are among the highlights, as they may reshape expectations around the ECB’s and the Fed’s future policy plans.

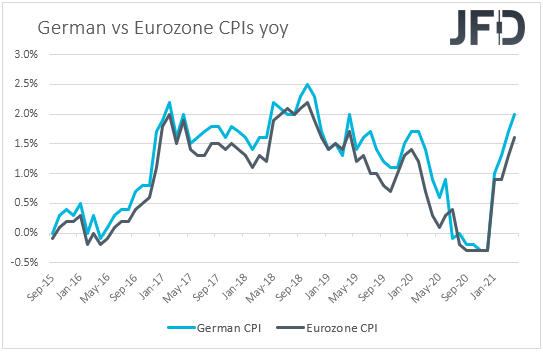

Monday appears to be a light day, with the only release worth mentioning being Germany’s preliminary inflation data for May. Both the CPI and HICP rates are expected to have risen to +2.3% yoy and +2.5% yoy, from +2.0% and +2.1% respectively, something that would raise speculation for a similar reaction in Eurozone’s headline CPI, due out on Tuesday.

Markets in the US and the UK will stay closed. It’s Memorial Day in the US, while in the UK, it’s a Bank Holiday.

On Tuesday, during the Asian session, the RBA decides on monetary policy. At the prior meeting, officials kept policy unchanged, but noted, that, despite the strong economic recovery in Australia, inflation pressures remain subdued in most parts of the economy and that at the July gathering, they will consider further bond purchases.

Since then, the employment report for April showed that the unemployment rate slid to 5.5%, from 5.7%, but bearing in mind that the employment change revealed a 30.6k job loss, we believe that the unemployment rate may have declined for the wrong reasons. Indeed, the participation rate slid to 66.0% from 66.3%, suggesting that more people have been discouraged to register for unemployment benefits, thereby resulting in a slide in the unemployment rate. What’s more, the wage price index ticked up to 1.5% yoy from 1.4%, but, although this is a move in the desired direction, it confirms the Bank’s view that inflation is likely to stay subdued, or at least, any spikes are likely to be due to transitory factors.

With all that in mind, we expect RBA policymakers to stand pat at this gathering, but to reiterate the view that they may add to their bond purchases at the July gathering. The Aussie may slide somewhat in the aftermath of this meeting, but we expect its broader faith to depend on developments surrounding the overall market sentiment.

Later in the day, we get Eurozone’s preliminary CPIs for May. The headline rate is expected to rise further, to +1.9% yoy from +1.6%, while the HICP excluding energy and food rate is forecast to have ticked up to +0.9% yoy +0.8%. Although the headline rate is expected to match the ECB’s objective of “below, but close to 2%”, the weak underlying inflationary pressures suggest that the improvement in headline inflation may be due to transitory factors.

After all, last week, ECB Chief Economist Philip Lane has pushed against the inflation-is-back narrative, adding that markets will take years to return to pre-crisis levels and that stimulus is still needed to secure the recovery. On top of that, a week earlier, ECB President Christine Lagarde said that it is “essential that monetary and fiscal support are not withdrawn too soon”. Therefore, we don’t expect an increasing headline CPI rate in Eurozone to support the euro much at the time of the release, or hurt European equity markets.

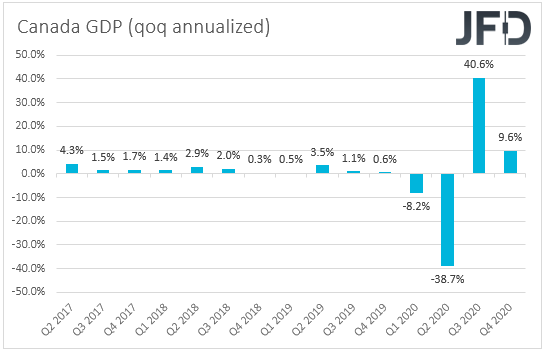

Later in the day, Canada’s GDP for Q1 and March is due to be released. The annualized qoq rate for the first three months of 2021 is expected to have declined to + 6.6% from +9.6% in the last quarter of 2020. However, the mom rate for March is anticipated to have risen to +1.0% from +0.4%, which following the surge in both the headline and core CPI rates for the month of April, is likely to dismiss questions as to whether the BoC has acted correctly at its last gathering when it scaled back its QE purchases. That said, a lot with regards to speculation on that front may depend on the results of Canada’s employment report on Friday. In our view, for the Loonie to return on the driver’s seat again, we need to see improvement in the labor market as well.

As for the rest of Tuesday’s scheduled data releases, we have Switzerland’s GDP for Q1, which is expected to reveal that the economy has contracted 0.5% after expanding 0.3% in Q4 2020, as well as the final manufacturing PMIs for May from the Eurozone, the UK, and the US, which as it is always the case, are expected to confirm their preliminary estimates.

The ISM manufacturing index for the month is also coming out and expectations are for an unchanged print, at 60.7. Staying at elevated levels, the ISM manufacturing index is likely to confirm that the US economy is recovering from the damages of the pandemic at a decent pace, but how the markets will be traded in the near term may depend more on the outcome of Friday’s employment report for the month.

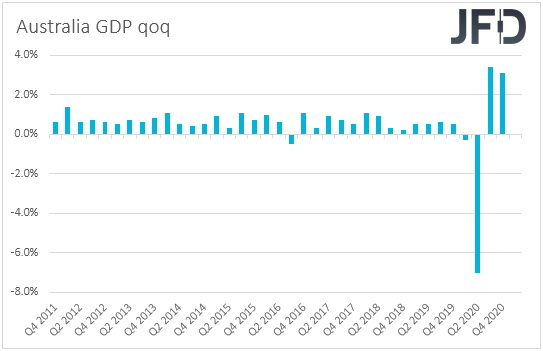

On Wednesday, Asian time, Australia releases its GDP data for Q1, with the qoq rate expected to have declined to +1.0% from +3.1%, but the yoy one to have rebounded to +0.2% from -1.1%. In our view, although we may see an improvement in yoy terms, a second consecutive slowdown in quarterly terms may add more credence to the RBA’s choice to expand its stimulative efforts in July, and thereby hurt the Aussie a bit more.

On Thursday, we have more data coming out from Australia, and this is the trade balance and retail sales, both for April. The nation’s trade surplus is expected to have increased to AUD 8.00bn from AUD 5.57bn, while retail sales are anticipated to have expanded 1.0% mom, the same pace as in March. The final Markit services and composite PMIs for May from the Eurozone, the UK, and the US, as well as the US ISM non-manufacturing PMI for the month, are also due to be released. The final Markit prints are expected to confirm their preliminary estimates, while the ISM index is forecast to have inched up to 63.0 from 62.7.

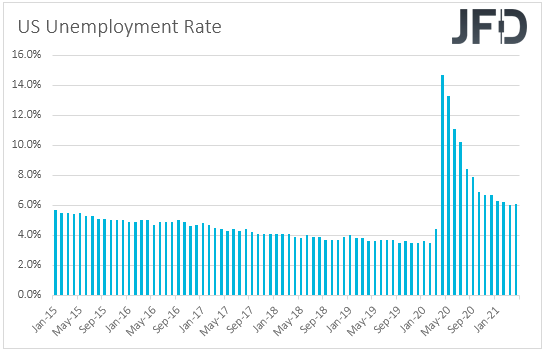

Finally on Friday, the main event is likely to be the US employment report for May. Nonfarm payrolls are anticipated to have accelerated to 650k from 266k in April, while the unemployment rate is forecast to have slid to 5.9% from 6.1%. Average hourly earnings are expected to have slowed to +0.2% mom from +0.7%, but this is likely to take the yoy rate up to +1.6% from +0.3%, suggesting that increasing wages are likely to translate to even higher inflation in the months to come.

Something like that, combined with the recent surge in both headline and core inflation, as well as remarks by several Fed policymakers over QE tapering, may add to speculation that the Fed may need to withdraw policy sooner than previously anticipated, and thereby, support the dollar. Strangely, although this would still suggest a recovering economy, it could hurt equity markets, as scaling back QE sooner could result in raising interest rates sooner as well. Let’s not forget that high-growth companies are valued based on earnings expected years into the future, and thus, when expectations over higher interest rates rise, there is more concern that the discounted present values of those companies will decline.

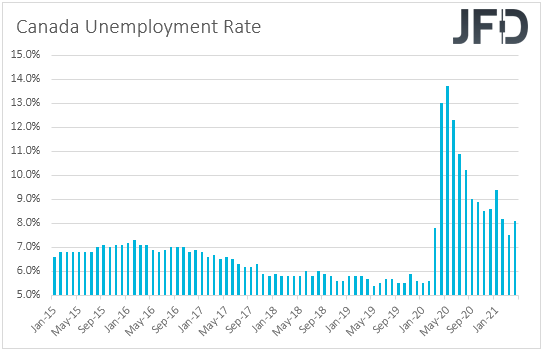

At the same time as the US jobs data, we get the employment report for May from Canada as well. The unemployment rate is expected to have ticked up to 8.2% from 8.1%, but the net change in employment is anticipated to show that the economy has lost much less jobs than it did in April. Specifically, it is expected to show a 22.5k jobs loss following a 207.1k tumble in April. In our view, this is not the best report Loonie traders could get, but it is better than the previous one. Thus, they may not sell the currency massively if the results are near their forecasts, especially if the GDP data, due out on Tuesday, come on the decent side.