RBA meeting minutes are on the agenda. UK, EUR and Canada inflation numbers fall into the spotlight on Wednesday. Also, on Wednesday we will get the FOMC meeting minutes. On Thursday, the ECB will publish its account of monetary policy meeting. UK and Canada will deliver their retail sales on Friday. UK, EU and US preliminary PMIs are also to be monitored on Friday.

Monday will be a relatively quiet day on the economic calendar. The only worthwhile information, which we will keep an eye on, will be the Japanese GDP figures on a QoQ and YoY basis. The data is already out and we see that the Japanese GDP on a QoQ basis came out as a slight disappointment, missing the forecast by minus two-tenths of a percent. The expectation was for a number at -7.6%, but it came out at -7.8%. The previous reading was at -0.6%. The YoY reading showed up at -27.8%, when the initial forecast was for a -27.2%. The previous reading was at -2.2%.

During the early hours of the Asian morning on Tuesday, we will receive the RBA meeting minutes. Two weeks ago, the RBA held its meeting and as it was expected, the Bank didn’t go ahead with moving its cash rate from the current position, at +0.25%. In the recent MPC statement, the RBA outlined that they will not increase the cash rate until progress will be made towards full employment and reaching the inflation target, which is between 2%-3%. The board also expects unemployment for December to be around 10%, then around 8.5% for December 2021 and around 7% for December 2022. Also, the RBA sounded a bit more pessimistic about Australia’s YoY GDP for 2020, as the Bank believes it may contract 6%. The Bank continues to monitor carefully the economic situation in the country and to support the liquidity of the domestic financial system. The current times of the pandemic are strongly affecting Australian households, as their consumption deteriorates due to the uncertainty of the future economy.

Also, on Tuesday, we will receive the US building permits for the month of July, together with the housing starts for the same period. Both numbers are believed to have improved. The building permits are forecasted to have gone from 1.258m to 1295m and the housing starts are expected to have risen from 1186m to 1230m. We believe that the figures will not affect the market significantly.

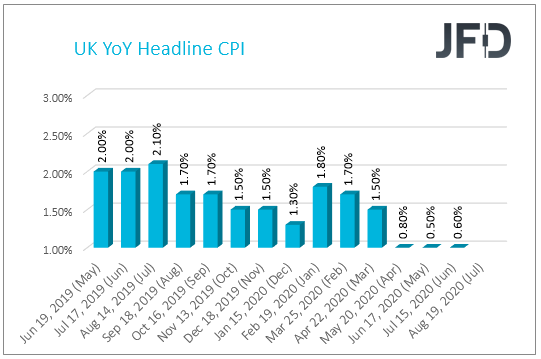

Wednesday will be an inflation report day, where several nations will deliver their CPI figures for the month of July. UK will kick off with their part, delivering the core and the headline numbers on a MoM and YoY basis. Both MoM and YoY core readings, which exclude food and energy, are believed to have declined somewhat. The YoY number is forecast to have moved from the previous +1.4% to +1.3%, and the MoM number is believed to have drifted into negative territory, from +0.2% to -0.1%. However, the headline MoM and YoY figures are expected to come out mixed. The MoM reading is forecasted to follow the core number, going from +0.1% to -0.1%, but the YoY one is expected to have risen from +0.6% to +0.7%. If the actual readings come out better than expected, this might prove to be positive for GBP. That said, the positivity may be short-lived, if the actual figures are still well below BoE’s inflation target of +2%.

Next in-line will be the Eurozone with their inflation readings for July. The ECB has also set its inflation target at close but below 2%. The expectations for now are sat at +0.4% and -0.3% for the YoY and MoM figures respectively. If the forecasts are correct, then that would mean that the YoY number remained the same as previous and the MoM figure had declined, as the last reading was at +0.3%.

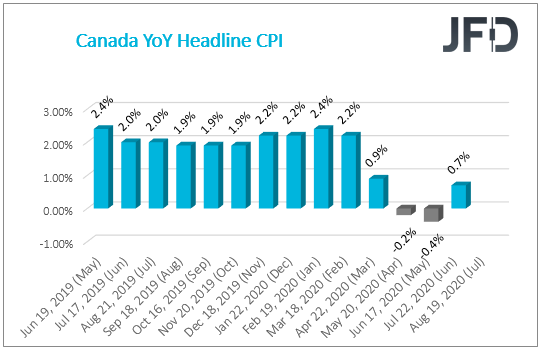

Canada will also be the one, which will release its inflation numbers. It is believed that in July, the Canadian headline MoM and YoY figures have fallen twice from its previous +0.8% and +0.7%. The forecast currently stand at +0.4% for MoM and +0.3% for YoY. Unfortunately, there are no estimates for Canada’s core CPI readings at the moment.

Another important piece of information on Wednesday will be from the FOMC’s, which will release its Meeting Minutes. At the end of July, the FOMC kept its interest in the range of 0% and +0.25%. According to the CME’s FedWatch Tool, there currently no expectations for the target range to change all the way till March 2021. The FOMC had noted in their last statement, quote: “The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” The main concern for the FOMC right now is the coronavirus and its effects on the US and global economies. Also, tensions with China are also monitored, as that may force the Fed to adjust their policy accordingly, if there won't be any progress in the US-China talks.

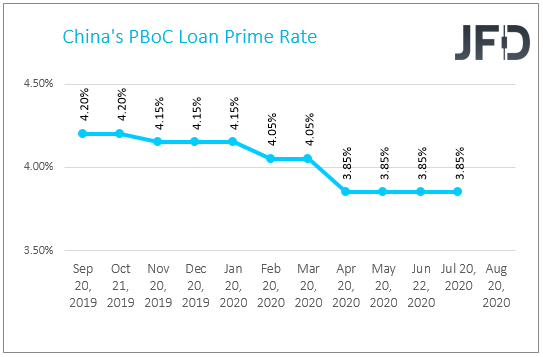

On Thursday, during the early hours of the Asian morning, the People’s Bank of China will deliver its loan prime rate, which is expected to have remained the same, at +3.85%.

During the early European morning, two Scandinavian countries will release some of their data into the market. Sweden is set to show their unemployment level and Norway’s Norges Bank will deliver its interest rate. Unfortunately, there is no forecast for the Swedish unemployment number, but we know that the previous was at 9.8%. Norges Bank is expected to have kept their interest rate unchanged, at 0.00%.

Later on, the spotlight will fall on the ECB, as it publishes the account of monetary policy meeting. During the last meeting, the Bank decided to raise its PEPP (its pandemic emergency purchase program) by EUR 600bn to a total of EUR 1350bn, extending to “at least the end of June 2021”. The committee also said that they are ready to adjust their policies accordingly, to ensure inflation moves towards their aim in a sustained manner.

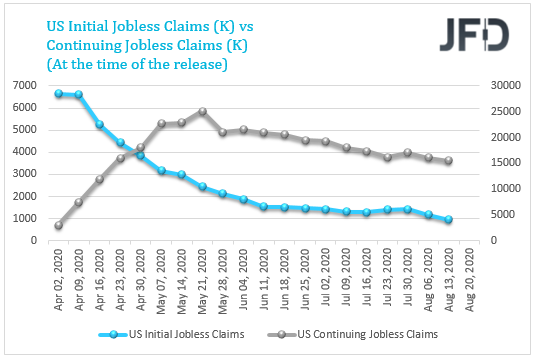

And finally, we will get the US initial and continuing jobless claims for the past week. As we can see, both readings continue to decline, which is a good sign that Covid-19 related labor market issues are being managed well. Although the current expectations are for another decline in both data sets, if by any chance, the actual numbers show up on the worse side, that may shake up the US market positivity, which has been dominating so far. However, the negative effect from that might be short-lived, as market participants will focus on other key factors, such as preliminary PMIs and the coronavirus daily cases.

During the early hours of Friday morning, Australia will produce its preliminary manufacturing and services PMIs. So far there is no forecast for the figures, but we know that both of them have been slowly crawling back up in the expansionary territory.

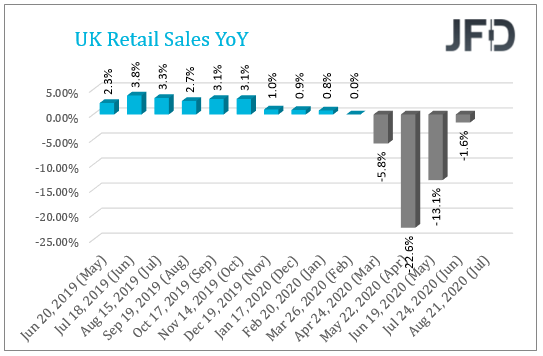

In Europe, UK will start off with showing its core and headline retail sales figures for the month of July on a MoM and YoY basis. Both core and headline MoM readings are expected to have fallen drastically from the previous month's figures. The core MoM is believed to have declined from +13.5% to +0.2% and the headline is expected to have moved from +13.9% to +2.3%. Although these look as significant slides, the forecasts are actually similar to what it was prior to the lockdown period. The core YoY figure is also expected to have moved lower, from +1.7% to +1.5%, whereas the headline YoY forecast currently sits on the higher side from the previous -1.6%, at +0.1%.

Later on, several nations will be delivering their preliminary composite, manufacturing and services PMIs. For instance, Germany’s preliminary manufacturing PMI reading for August is believed to have ticked up from 51.0 to 52.5. The eurozone preliminary manufacturing PMI is also expected to improve, going from 51.8 to 53.0. However, eurozone’s services are forecasted to slide a bit, from 54.7 to 54.2. If we get much better than expected readings that initial expectations, this may prove to be positive for the euro, giving the common currency a bit of a push higher against its major counterparts.

Currently, there is no forecast for the UK’s preliminary composite, manufacturing and services PMIs.

Canada’s core and headline retail sales for June will be on the agenda as well. The country is expected to show a better than the previous core number, going from 10.6% to 15.0%. The headline one is believed to have risen drastically, from 18.7% to 24.5%. If the actual numbers come out as expected or above, this may help strengthen the Canadian dollar.

And finally, it will be the US’ turn to deliver the same set of data. There is no forecast for the preliminary composite PMI reading, at the moment. That said, both the manufacturing and services PMIs are believed to have improved from 50.9 to 51.8 and from 50.0 to 51.0 respectively.

In addition to the PMIs, US will release its existing home sales for the month of July, where the number is expected to have improved. The previous reading was at 4.72M, whereas the forecast is sat at 5.39M. If the actual figure comes out as expected, or even better, that will bring the indicator back to its pre-April levels.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Weekly Outlook: RBA, ECB, FOMC Meeting Minutes, CPIs, Preliminary PMIs

Published 08/17/2020, 04:57 AM

Updated 07/09/2023, 06:31 AM

Weekly Outlook: RBA, ECB, FOMC Meeting Minutes, CPIs, Preliminary PMIs

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.