The first week of 2021 appears to be relatively busy, with the main items on the agenda being the elections in the US state of Georgia on Tuesday, which will determine who controls the Senate, the Eurozone CPIs on Thursday, and the US employment report on Friday, which may impact the Fed’s thinking with regards to how they will implement monetary policy in the foreseeable future. The minutes from the latest FOMC gathering and Canada’s jobs data are also coming out, on Wednesday and Friday respectively.

Monday is a relatively light day, with the only economic releases worth mentioning being the final PMIs for December from the Eurozone, the UK, and the US. However, as it is almost always the case, all the final prints are forecast to confirm their preliminary estimates.

On Tuesday, traders will have an eye on the runoff election in the US state of Georgia, which will determine who controls the Senate, as there are two seats to be voted for. Georgia has not elected a Democrat senator in 20 years, and if either or both Republican incumbents win, their party would retain a narrow majority. However, if Democrats win both seats, each party will have 50 seats, giving the tiebreaking vote to Vice President-elect Kamala Harris. With that in mind, a Democratic sweep could raise speculation that with a Democratic controlled Congress, President-elect Biden’s fiscal agenda will pass much more easily, which could mean higher stimulus spending. Therefore, the dollar is likely to continue to slide, while equities are likely to continue marching north.

The opposite may be true if Republicans retain control, but we expect any declines to be short-lived, as market participants are still happy with the passing of the latest spending bill. The prospect of a global economic rebound during 2021 due to the coronavirus vaccinations may also keep risk-linked assets supported, and safe havens under selling pressure.

As for Tuesday’s data, during the European morning, we get Switzerland’s CPI for December, which is expected to have stayed unchanged at -0.7% yoy. With consumer prices deep in deflationary territory, the SNB is likely to maintain the view that the Swiss franc remains highly valued, while remaining willing to intervene more strongly in the FX market.

Germany’s retail sales for November, and the nation’s unemployment rate for December are also coming out. Retail sales are expected to have declined 2.0% mom after rising 2.6% in October, while the unemployment rate is forecast to have held steady at 6.1%. Later in the day, from the US, we get the ISM manufacturing PMI for December, which is expected to have declined to 56.5 from 57.5.

On Wednesday, the main release may be the minutes from the latest FOMC gathering, at which officials kept policy unchanged, but changed their forward guidance saying that they will continue to buy bonds “until substantial further progress has been made towards the Committee’s maximum employment and price stability goals.” At the press conference following the decision, Fed Chair Powell said that the recovery has been quicker than expected, but he added that they remain open to increasing bond purchases or moving to longer maturities, and if they feel that this will help the economy, they will do it. With that in mind, we will scan the minutes for clues as to how willing Fed officials are to loosen their policy further, and if so, when further action may take place.

As for Wednesday’s, economic releases, during the Asian session, we get China’s Caixin services PMI for December, for which no forecast is available, while later in the day, the final services PMIs for the month from the Eurozone, the UK, and the US, are also due to be released. As always, they are expected to confirm their preliminary estimates. We also get Germany’s preliminary inflation numbers for December. The CPI rate is expected to have remained unchanged at -0.3% yoy, while the HICP one is forecast to have ticked up to -0.6% yoy from -0.7%.

On Thursday, during the Asian morning, Australia’s trade balance and building approvals for November are coming out. The nation’s trade surplus is expected to have declined to AUD 5.800bn from AUD 7.456bn, while the building approvals are forecast to have declined 3.0% mom, after rising 3.8%.

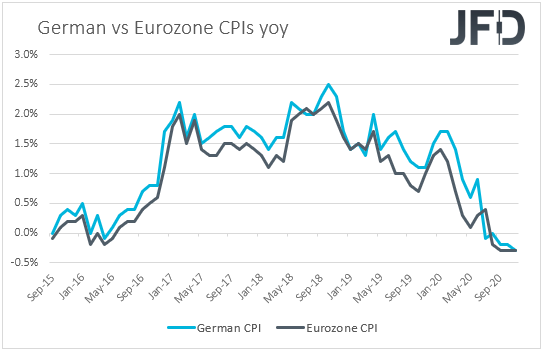

During the European morning, we get Eurozone’s preliminary CPIs for December. The headline rate is expected to have ticked up, but to have stayed within the negative territory. Specifically, it is expected to have risen to -0.2% yoy from -0.3%. The HICP excluding energy and food is expected to have slowed to +0.3% yoy from +0.4%.

At the last meeting for 2020, the ECB decided to expand its Pandemic Emergency Purchase Programme (PEPP) by EUR 500bn and extended the scheme by nine months to March 2022. That said, the euro gained on the decision, as, due to the currency’s prior appreciation, many may have expected the Bank to deliver more. Currently the EUR/USD exchange rate is trading at a higher level than back then, which is a negative for consumer prices. After all, President Lagarde said at the press conference following the last decision that the appreciation of the euro exercises downward pressure on prices and that they will monitor it very carefully. Thus, another round of negative headline and very low core inflation prints may raise speculation that the ECB may decide to act again in the first months of the new year.

The bloc’s retail sales for November and the UK’s construction PMI for December are also coming out. Euro area’s retails sales are anticipated to have fallen 3.6% mom after rising 1.5%, while the UK construction PMI is forecast to have inched up to 55.0 from 54.7.

Later in the day, from the US we have the ISM non-manufacturing PMI for December and the trade balance for November. The ISM print is expected to have declined to 54.6 from 55.9, while the trade deficit is forecast to have widened to USD 64.50bn from USD 63.10bn. We get trade data for November from Canada as well, with the nation’s deficit expected to have narrowed somewhat, to CAD 3.30bn from USD 3.76bn.

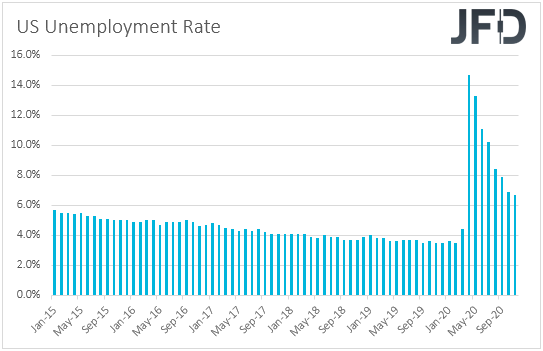

Finally, on Friday, the main event may be the US employment report for December. Nonfarm payrolls are expected to have slowed to 100k from 245k in November, while the unemployment rate is forecast to have ticked up to 6.8% from 6.7%. Average hourly earnings are expected to have ticked down to +0.2% mom from +0.3%, which, barring any deviations to the prior monthly prints, is likely to keep the yoy rate unchanged at +4.4%.

A softer-than-previously employment report may add to speculation that the Fed will do whatever it can to support the economy, which could push the US dollar lower. The big question is how equities will react. On the one hand, they could slide on signs of a weaker labor market, while on the other, they could gain on expectations of more support by the Fed.

That said, whatever the reaction is, we stick to our guns that the overall path remains positive and we would expect equities to continue marching north in the near-term, even if they correct lower on a soft employment report. As we noted several times, the vaccinations, a stimulus package in the US, and a Biden Presidency, may continue benefiting risk assets. Why Biden? Because we expect him to adopt a softer stance on global trade than Trump did, and also push for a looser fiscal agenda. The Brexit accord paints an even brighter picture.

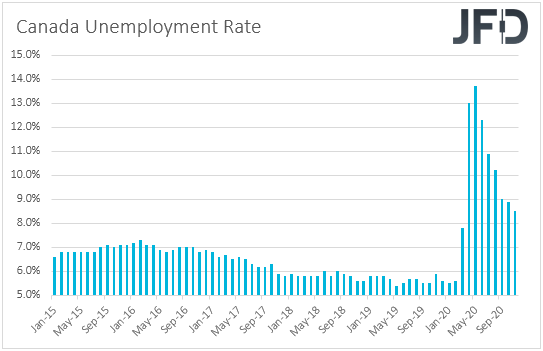

At the same time with the US employment report, we get jobs data from Canada as well. The unemployment rate is expected to have inched up to 8.6% from 8.5%, while the net change in employment is forecast to show that the Canadian economy has lost 20.0k jobs after gaining 62.1k in November.

After scaling back its QE purchases in October, the BoC decided to keep its policy unchanged in December, noting that the rebound in the global and Canadian economies has unfolded largely as the Bank anticipated in its October Monetary Policy Report. Officials acknowledged that the positive vaccine news is providing some reassurance but added that the pace and breadth of the global rollout of vaccinations remain uncertain.

Overall, the language was on the neutral side, and a weak employment report is unlikely to spark speculation for more reductions in QE purchases. On the contrary, it may add to chances of a QE re-increase, which could hurt the Canadian dollar. That said, we believe that the overall path of this commodity currency will depend on developments surrounding the broader sentiment. As we already noted, we see risk appetite improving in 2021, at least in the first months, something that could prove supportive for oil prices and thereby for the Canadian dollar.

As for the rest of Friday’s data, we have Germany’s trade balance for November, and Eurozone’s unemployment rate for the same month. Germany’s surplus is expected to slightly decline, while Eurozone’s unemployment rate is expected to have ticked up to 8.5% from 8.4%.