Following the ECB and BoC decisions last week, this week, it’s the turn of the Fed, the SNB, and the BoJ to conclude on monetary policy. We don’t expect any of these three Banks to alter its policy settings, but the Fed gathering may attract some special attention following the latest surge in US inflation and remarks by some policymakers over a potential discussion on QE tapering.

The UK and Canadian CPIs may also receive some extra attention.

On Monday, the economic calendar is light, with no major events or indicators scheduled.

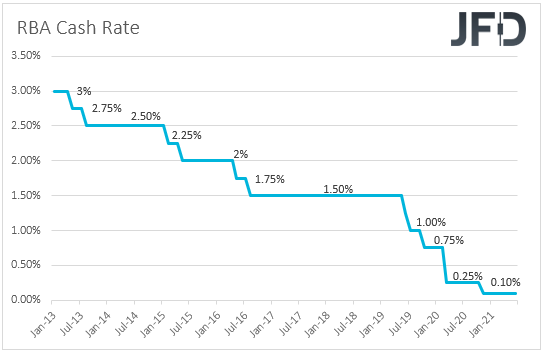

On Tuesday, Asian time, the RBA releases the minutes of this month’s gathering, where policymakers stood pat and reiterated that, at the July meeting, they will consider further bond purchases. With that in mind, we will scan the minutes for clues and hints as to how strong the likelihood for such an action is.

During the early EU session, the UK employment report is expected to reveal that the unemployment rate ticked down to 4.7% from 4.8%, and that the economy has added 150k jobs in the three months to April, more than the 84k in the three months to March.

Average weekly earnings, both including and excluding bonuses, are forecast to have accelerated notably.

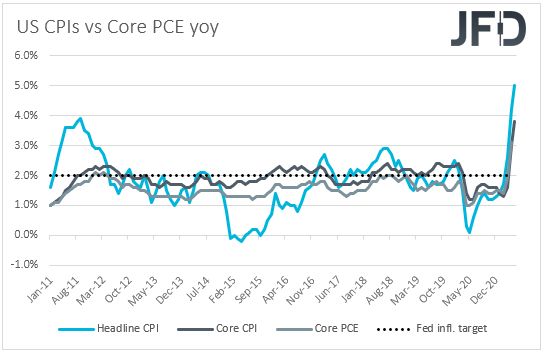

Later, from the US, we get the retail sales and PPIs for May, as well as the New York Empire State manufacturing index for June. The headline PPI is expected to have ticked up to +6.3% yoy from +6.2%, while the core rate is forecast to have jumped to +4.8% yoy from +4.1%.

Headline sales are anticipated to have fallen 0.8% mom after stagnating in April, but core sales are expected to have rebounded 0.4% mom after sliding 0.8%. The New York index is expected to have declined slightly, to 22.00 from 24.30.

On Wednesday, investors are likely to lock their gaze to the FOMC monetary policy decision. The prior decision was back on Apr. 28, when the Committee decided to keep its policy untouched, and repeated that they will keep it that way “until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time."

They acknowledged the improvement in economic activity, but at the press conference following the decision, Fed Chair Powell stuck to his guns, saying that the economy is a “long way” from their goals and that it’s not the time to start discussing about tapering QE.

However, since then, inflation surged in several nations of the world, with the US seeing a spike well above the Fed’s 2% objective in both headline and core terms. Several policymakers have already expressed their desire to discuss withdrawing monetary policy, and therefore, all the attention at this meeting will fall on that.

Despite the abnormal surge in inflation, the details in last week’s data suggest that indeed, there may be some temporary factors contributing to the rally. Thus, we don’t expect officials to rush into taking a decision now.

However, it would be interesting to see whether there will be a discussion around the matter, and if so, whether we will get any hints over a potential desired pace of withdrawal. A fast pace may suggest that Fed officials do not see the surge in inflation as transitory as they did in the past and may hurt equities.

At the same time, the US dollar and other safe havens could come under some buying interest. On the other hand, any discussion suggesting that the time for scaling back monetary policy has not come yet, or anything pointing to a very slow pace of tightening, may encourage market participants to increase their risk exposure a bit more.

As for Wednesday’s data, during the Asian morning, we get China’s fixed asset investment, industrial production, and retail sales, all for the month of May. New Zealand’s current account balance for Q1 and Japan’s trade balance for May are also due to be released.

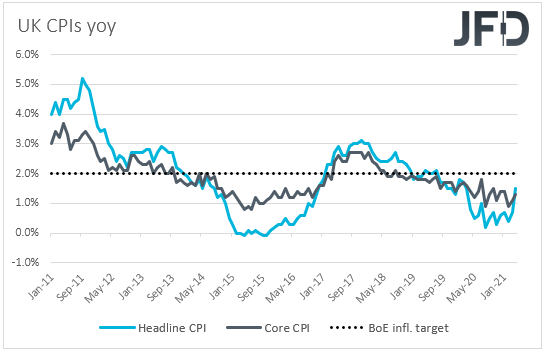

During the early EU trading, we have the UK CPIs for May. Both the headline and core rates are expected to have increased to +1.8% yoy and +1.5% yoy from +1.5% and +1.3%.

Last time, British policymakers kept interest rates unchanged, but they proceeded with a technical change in which the pace of weekly bond purchases slowed down. That said, they reaffirmed that "as measured by the target stock of asset purchases, that stance remains unchanged," adding that the QE slowdown is not a material change and that they are ready to reverse it if deemed necessary.

With regards to their economic projections, they expected the UK economy to recover to pre-pandemic levels over the course of this year, while on the inflation front, they said that it may rise above 2% towards the end of the year, but this is likely to be due to transitory effects and thus, the rise may prove to be temporary.

With that in mind, and also taking into account that there is a risk of delaying the reopening of the UK economy due to the rising coronavirus cases, even if inflation accelerates somewhat, we don’t believe that it will spark speculation for more action by the BoE at its upcoming gathering.

Thus, the pound is unlikely to receive any strong support. On the contrary, with all this uncertainty surrounding the spreading of the coronavirus, it may correct somewhat lower. Just to be clear though, we don’t believe that we will see a trend reversal yet, perhaps only a correction, and this is because the UK economy appears to have been performing very well recently.

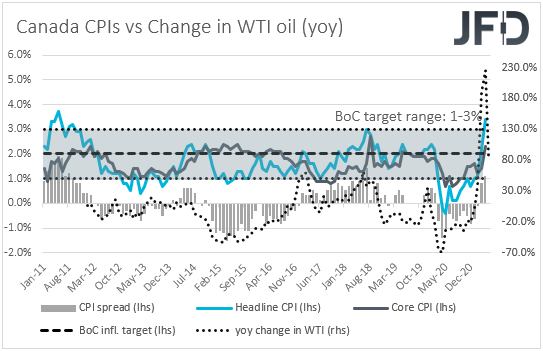

Later in they day, we get more CPI data for May, this time from Canada. The headline CPI is anticipated to have ticked up to +3.5% yoy from +3.4%, while no forecast is available for the core rate.

Last week, the BoC kept its policy unchanged and noted that any adjustments to the pace of their QE purchases will be guided by the ongoing assessment of the strength and durability of the economic recovery.

Although the Bank scaled back its bond purchases at the gathering before that, we now believe that inflation may need to decently overshoot its forecasts for market participants to start discounting the chance for further tapering taking place soon.

In the US, building permits and housing starts for May are due to be released, and expectations are for both to have increased somewhat.

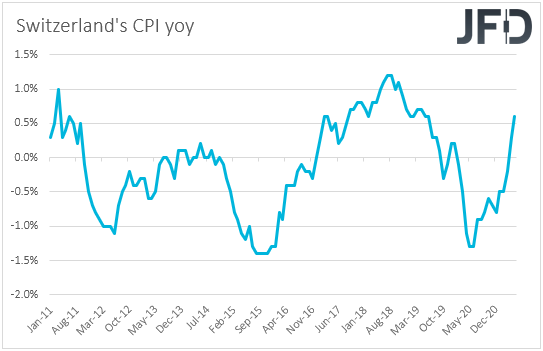

On Thursday, the central bank torch will be passed to the SNB. The last gathering of this Bank was back in March, and resulted in no fireworks. The Bank kept its policy unchanged, reiterating that the Swiss franc remains highly valued and that they are willing to intervene more strongly in the FX market.

Despite the surge in inflation in other places of the globe, Switzerland’s consumer prices remain subdued, well below the SNB’s objective of 2%, and thus, we don’t believe that the SNB will risk sounding less dovish, as this may result in an even stronger franc, something they seem not to want.

After all, a few weeks ago Chairman Thomas Jordan reiterated the view that the franc remains very strong and that he sees no reason to change the current policy settings. Thus, we expect policymakers to keep policy steady and maintain their willingness to intervene when deemed necessary.

As for Thursday’s data, during the Asian trading, we have New Zealand’s GDP for Q1 and Australia’s employment report for May. New Zealand’s GDP is forecast to have rebounded 0.5% qoq after contracting 1.0% in the last three months of 2020, which could diminish further the chances for the RBNZ to lower its OCR further, and thereby support the kiwi.

Remember that at their latest meeting, officials appeared more optimistic than previously and instead of clearly saying that they remain ready to lower the OCR if required, officials just agreed that the OCR is the preferred tool to respond to future economic developments in either direction.

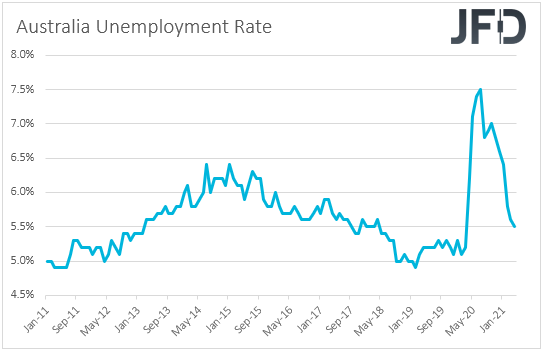

Now, flying to Australia, the unemployment rate is expected to have held steady at 5.5%, while the net change in employment is anticipated to reveal that the economy added 30.0k jobs in May, after losing 30.6k in April. At this month’s gathering, the RBA reiterated that, at the July meeting, it will consider further bond purchases, and a decent employment report may bring them a step closer to that decision.

Finally, on Friday, it’s the turn of the BoJ to decide on monetary policy. The last time they met, policymakers of this Bank did not proceed with any policy change either. They kept all their settings unchanged, revising up their growth forecasts, but downgrading their inflation ones.

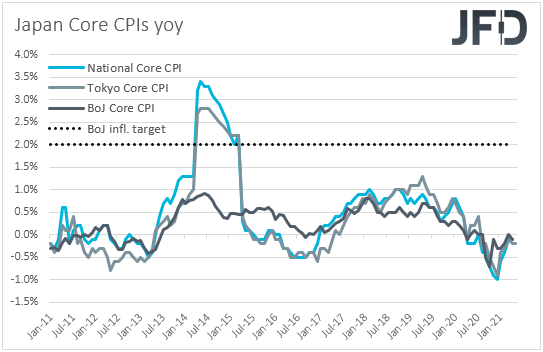

Since then, inflation in Japan remained in negative waters during the month of April, in both headline and core terms, while, during the first three months of 2021, the Japanese economy contracted 1.0% qoq after expanding 2.8% in Q4 2020.

With all that in mind, we expect the BoJ to stay on the dovish side and keep its main policy settings unchanged. The only item of interest with regards to this Bank, is that it is considering to expand the September deadline for its pandemic relief program.

According to market chatter, a 6-month extension is the most likely outcome. However, the official announcement may not come at this gathering, as policymakers can still delay the decision to July.

As for Friday’s data, the only release worth mentioning is the UK retail sales for May. Both headline and core sales are expected to have slowed to +1.8% mom and +2.0% mom, from +9.2% and +9.0% respectively.