There are no central bank meetings on this week’s agenda, but we do get the minutes from the latest Fed, RBA and ECB monetary policy gatherings, from which we may get some extra clues with regards to those Bank’s future plans.

On Monday, during the Asian morning, we already got Japan’s preliminary GDP for Q4, which slowed by less than anticipated, to +3.0% qoq from +5.3%. The forecast was for a slowdown to 2.3% qoq.

As for the rest of the day, markets in the US and Canada will stay closed due to the President’s Day and the Family Day respectively, while in China, markets will stay closed for the whole week due to the celebrations for the Lunar New Year.

The only noteworthy release on today’s agenda is Eurozone’s industrial production for December, which is forecast to have deteriorated 1.0% mom after expanding 2.5% in November.

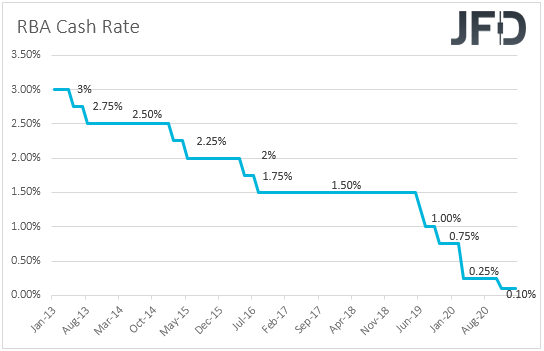

On Tuesday, during the Asian session, the RBA releases the minutes from its latest monetary policy meeting, where officials decided to expand their QE program to to buy additional AUD 100bn of bonds. Although we don’t expect this to be followed by more easing in the next couple of months, we will scan the minutes to see whether our view is indeed correct, or not.

During the European trading, we get the German ZEW survey for February, the 2nd estimate of Eurozone’s GDP for Q4, as well as the bloc’s preliminary employment change for the quarter.

With regards to the ZEW survey, the current conditions index is expected to have declined to -67.0 from -66.4, while the economic sentiment index is forecast to have fallen to 59.5 from 61.8. The 2nd estimate of Eurozone’s GDP is anticipated to confirm its preliminary estimate of -0.7% qoq, while no forecast is available for the employment change.

Later, from the US, we have the New York Empire State manufacturing index for February.

On Wednesday, the main item on the agenda may be the minutes from the most recent FOMC gathering. At that meeting, the Committee decided to keep its monetary policy settings unchanged, with the only material change in the statement being the part saying that “the pace of the recovery in economic activity and employment has moderated in recent months”.

While there was some market chatter over QE tapering, at the press conference following the decision, Fed Chair Powell clearly stated that it’s too early to focus on tapering dates.

We’ve heard from him last week as well, with the tone of his speech staying on the dovish side. He noted that the improvement in the labor market has stalled in recent months, and even if we do see a strong labor market soon, they will not tighten monetary policy solely in response to that.

He affirmed that they will keep interest rates at current levels until the economy has reached maximum employment and inflation stays above 2% for some time. With all that in mind, it will be interesting to search the minutes for clues as to whether other officials are on the same page with their Chief.

If so, the US dollar is likely to stay under selling interest, while equities and other risk-linked assets may continue marching north on expectations that the Fed will do whatever it takes to support an economy severely hit by the coronavirus pandemic.

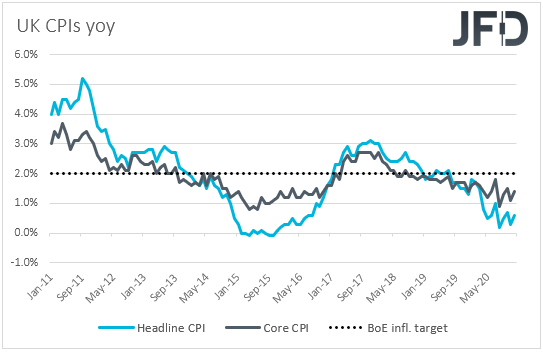

As for Wednesday’s data, during the early European morning, we get the UK CPIs for January. Both the headline and core rates are expected to have ticked down to +0.5% yoy and 1.3% yoy, from +0.6% and +1.4% respectively.

Although such prints will keep the door open for an increase in the BoE’s QE purchases if deemed necessary, we don’t expect them to hurt the pound much. At its latest gathering, the BoE pushed back the idea of negative interest rates, which combined with the fact that the UK is going further ahead in the covid vaccination race, encouraged GBP-traders to buy more of the British currency.

In our view, the same catalysts are likely to continue supporting the pound, and bearing in mind that we see market appetite staying supported in the foreseeable future, sterling may perform better against the safe-havens yen and franc.

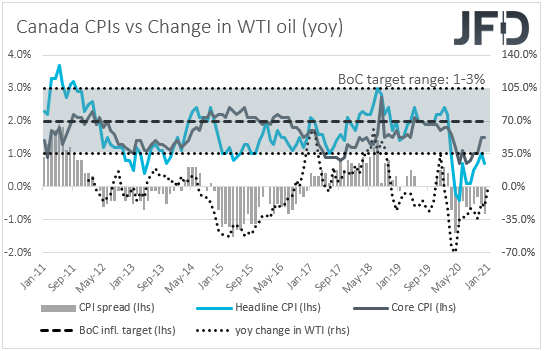

Later in the day, we get inflation data from Canada as well. The headline rate is expected to have ticked up to +0.8% yoy from +0.7%, while no forecast is available for the core rate. At its prior meeting, the BoC decided to keep interest rates and the pace of its QE purchases unchanged, disappointing those expecting a small cut or even a re-increase in QE.

Officials also noted that “As the Governing Council gains confidence in the strength of the recovery, the pace of net purchases of Government of Canada bonds will be adjusted as required", which suggests that the next policy step for BoC may be tapering QE.

However, the employment report for January disappointed, with the unemployment rate rising to 9.4% from 8.9%, and the net change in employment showing that the economy has lost 212.8k jobs. With that in mind, although a bit higher, an inflation rate well below the BoC’s inflation aim of 2% is unlikely to suggest that tapering may be on the cards in the months to come.

A disappointment could even push back expectations on that front, something that may prove negative for the Canadian dollar. That said, with oil prices climbing higher, and the overall market sentiment staying supported, we believe that such a reaction will prove to be temporary. Eventually the commodity-linked currency may recovery its inflation-related losses and continue to trend north, at least against the safe havens.

In the US, we have the retail sales and industrial production data for January. Both headline and core sales are expected to have rebounded 1.0% mom, after falling 0.7% and 1.4% respectively, while industrial production is forecast to have slowed to +0.4% mom from +1.6%.

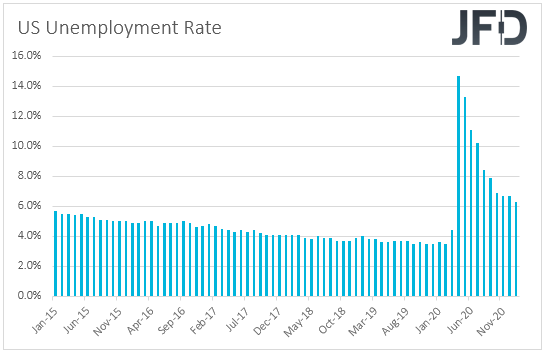

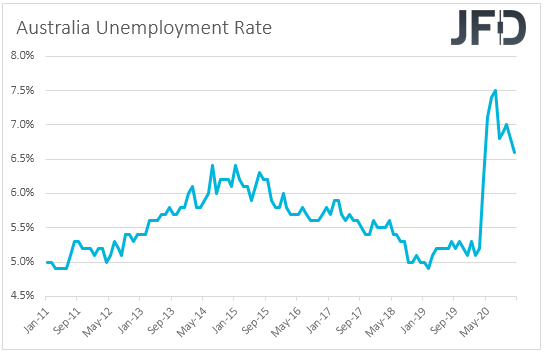

On Thursday, Asian time, we get Australia’s employment report for January. The unemployment rate is forecast to have slid to 6.5% from 6.6%, while the net change in employment is expected to show that the economy has added another 40.0k jobs, a slowdown from the 50.0k in December.

However, following the stellar gains in October and November, we see the case for slowing jobs’ growth as more than normal and thus, we don’t expect this to raise speculation for more easing by the RBA in the months to come, especially given that the Bank has already expanded its QE purchases at its latest gathering.

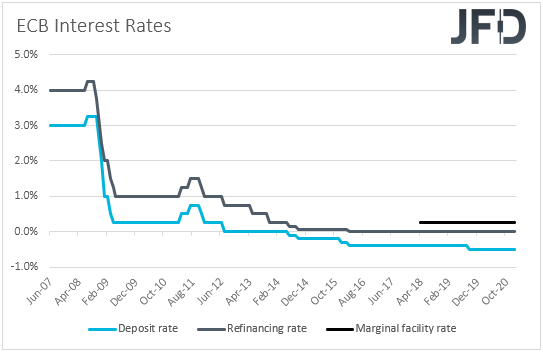

Later in the day, during the EU session, we have the minutes from the latest ECB monetary policy meeting. Despite the lockdown measures around the Eurozone, President Lagarde said that the downside risks to the economic outlook are now “less pronounced”, making investors skeptical over further easing by the ECB, although the Bank repeated once again that it stands ready to adjust all of its instruments as appropriate.

Therefore, we will scan the minutes to see whether Lagarde’s view is shared among other officials as well, and whether indeed the chances for more easing have lessened for now. Something like that may benefit somewhat the euro.

The US building permits and housing starts for January are also coming out, and they are both expected to have declined somewhat from their December readings.

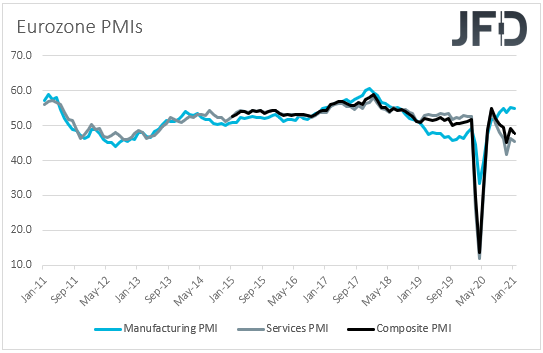

Finally, on Friday, investors may lock their gaze on the preliminary PMIs for February from several Eurozone nations, the Eurozone as a whole, the UK and the US. The Eurozone manufacturing PMI is forecast to have declined fractionally, to 54.4 from 54.8, but the services one is anticipated to have risen to 46.0 from 45.4.

This is likely to drive the composite index slightly higher, but to keep it within the contractionary territory. Specifically, the bloc’s composite index is forecast to have inched up to 48.0 from 47.8. In our view, this is unlikely to change expectations around the ECB’s future course of action, especially if the minutes point to a sidelined Governing Council for the next couple of months.

There are no forecasts for the UK prints, while in the US, both the manufacturing and services PMIs are expected to have declined somewhat. The manufacturing index is forecast to have fallen to 58.5 from 59.2, and the services one to 57.5 from 58.3.

As for the rest of Friday’s data, during the Asian morning, Japan’s National CPIs for January are coming out. No forecast is available for the headline rate, while the core one is anticipated to have increased to -0.7% yoy from -1.0%.

Later in the day, we have the UK and Canadian retail sales for January and December respectively. Both the headline and core UK sales are expected to have declined 1.6% mom and 1.8% mom, after rising 0.3% and 0.4%, while in Canada, the headline rate is anticipated to have fallen to -2.6% mom from 1.3%. The core rate is forecast to have fallen as well, to +0.3% mom from +2.1%. The US existing home sales for January are also due to be released and expectations are for a slight decline.