Following the ECB and the BoC last week, there are three more central bank gatherings on this week’s agenda. Those Banks are the Fed, the BoE and the BoJ, with market participants eager to find out whether any of them will follow the footsteps of the ECB to counter the quick rally in bond yields.

However, with Fed and BoE policymakers sharing a relaxed view over the matter, we don’t expect any action from these two Banks. The BoJ is unlikely to act either, as Governor Kuroda put at ease earlier rumors that they may widen the 10-year JGB yields band.

On Monday, there are no major events or released on the economic agenda.

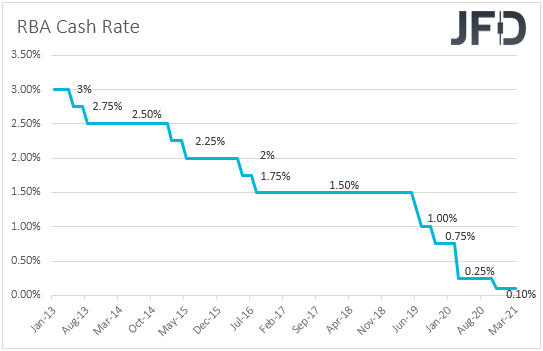

On Tuesday, during the Asian morning, we get the minutes from the latest RBA monetary policy meeting. At that meeting, Australian policymakers kept their monetary policy settings unchanged and noted that the economic recovery is well under way and has been stronger than earlier expected.

However, they also put at ease concerns over high inflation, noting that wage and price pressures are subdued and are expected to remain so for some years. In our view, this means that the Bank is unlikely to alter its policy in the foreseeable future, and thus, we will scan the minutes to confirm that this is the case.

As far as the Australian dollar is concerned, given that we believe that the RBA is likely to stay sidelined in the months to come, we expect it to stay dependent mostly on developments surrounding the broader market sentiment. Further optimism is likely to prove positive for this currency.

Later in the day, we get Germany’s ZEW survey for March, the US retail sales for February, and the US industrial production for the same month. With regards to the German ZEW survey, both the current conditions and economic sentiment indices are expected to have improved, while in the US, retail sales are anticipated to have seen a setback and industrial production to have slowed.

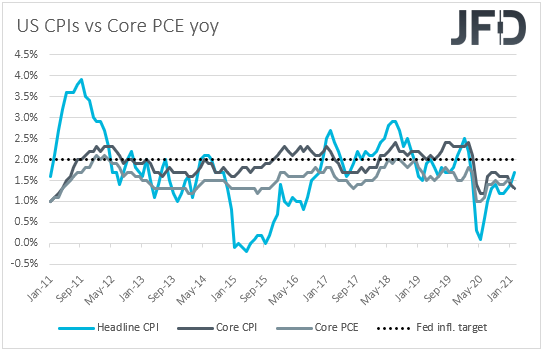

On Wednesday, all eyes will be turned to the FOMC interest rate decision. Following the most recent surge in US Treasury yields, some market participants may be on the lookout on any comments on that front, whether the Fed is considering reacting, and if so, how.

While the rally in yields was fueled by speculation that the Fed may have to tighten policy sooner than previously anticipated due to surging inflation, we don’t expect policymakers to add to such expectations.

After all, when testifying before Congress, Fed Chair Powell clearly noted that they will look beyond any temporary spikes in prices and that it may take more than three years for inflation to reach the Fed’s goal. Remember that the Fed wants inflation to rise above 2% for some time, something, which according to the minutes of the latest Fed gathering, is expected to happen in the years after 2023.

Now, on the other hand, there may be some investors waiting to see whether the Fed will follow the footsteps of the ECB and accelerate its bond purchases in order to avoid any unwarranted tightening in financial conditions due to the rise in bond yields. However, several Fed officials have noted that the rally in borrowing costs just reflects the optimism over a rapid recovery, brushing aside concerns about a return to the dysfunction in markets that dominated the early days of the coronavirus pandemic. Thus, we don’t expect the Fed to ease further either, especially with market sentiment improving towards the end of last week.

With all that in mind, both groups of investors are likely to get disappointed and thus, we don’t expect the US dollar to react much at the time of the event. That said, we stick to our guns that the greenback is likely to stay under selling pressure as inflation fears continue to ease, especially after last week’s soft US inflation data, while equities are likely to continue to trend north.

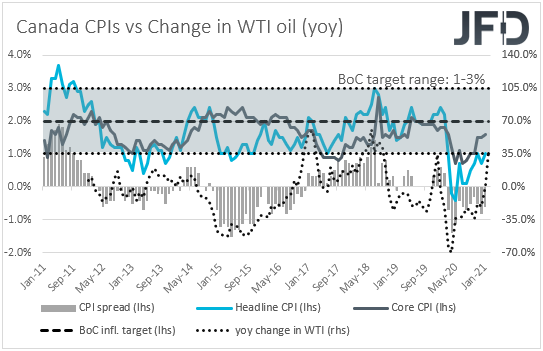

As for Wednesday’s data, the most important one seems to be Canada’s CPIs for February. The headline rate is expected to have risen to +1.3% yoy from +1.0%, but the core one is anticipated to have slid to +1.4% yoy from +1.6%.

At last week’s gathering, the BoC stood pat, noting that the economic recovery continues to require extraordinary monetary policy support, and that the 2% inflation goal is not expected to be sustainably achieved until into 2023, which means that any QE tapering may be unlikely in the next months.

Although officials kept the door on that front open, a rising headline CPI combined with a sliding core rate would mean that any increase in consumer prices may be due to the rise in oil prices and thus, it may be temporary. This will confirm the Bank’s view and may lessen even more the tapering likelihood.

Eurozone’s final CPIs for February are also coming out and they are expected to confirm their preliminary estimates, while in the US, we get building permits and housing starts for the same month with the forecasts pointing to small declines.

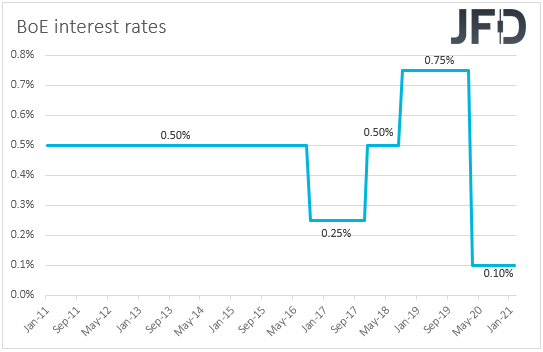

On Thursday, the central Bank torch will be passed to the BoE. At its latest gathering, this Bank kept its policy unchanged and pushed back the idea of negative interest rates. The central bank said that British banks will need at least six months to prepare for a shift into negative interest rates, but that doesn’t mean that the central bank is intended to set a negative rate at some point in the future. It was just concluded that it would be appropriate to start preparations in order to provide the capability to do so if necessary.

With BoE policymakers being aligned with the relaxed views of the Fed over the recent rally in bond yields around the globe, we believe that they have no immediate plans to counter the market reaction. Thus, taking also into account that the covid vaccinations proceed very well in the UK, we believe that this Bank is likely to maintain a degree of optimism, which may allow the pound to perform well, especially against the US dollar and the safe-havens yen and franc.

As for the data, during the early Asian morning, New Zealand’s GDP for Q4 is due to be released, with the forecast pointing to a slowdown to +0.1% qoq from +14.0%, something that would, however, take the yoy rate up to +0.5% from +0.4%. A few hours later, we get Australia’s employment report for February. The unemployment rate is forecast to have ticked down 6.3% from 6.4%, while the net change in employment is anticipated to show that the Australian economy has gained 30.0k jobs after adding 29.1k in January.

Finally, on Friday, we have another central bank deciding on monetary policy, and this is the BoJ. At their previous meeting, officials of this Bank kept monetary policy unchanged, and revised up their economic forecasts for the next fiscal year. However, they repeated that they will take additional steps without hesitation if deemed necessary. With this Bank committed to keep its long-term government bond yields around zero, we don’t expect any major reaction to the recent rally in other nation’s yields. After all, this is something negative for the yen, which works in favor of the Bank, as it may help boost the nation’s inflation. Although there were some rumors that the ±0.20% band around the 10-year JGB yields may be widened, Governor Kuroda has already denied that this is an option, which means that the Bank is most likely keep all its policy settings unchanged.

The Japanese yen is unlikely to react much, but, overall, we expect it to continue to trend south. If yields around the rest of the world rebound again, the yield-differential between other nations and Japan is likely to widen, which could prove negative for the yen. On the other hand, further retreat in yields is likely to keep equities and the broader market sentiment supported, as it will mean that inflation fears are fading, which is also negative for the yen. So, either way, the path of least resistance for the yen is to the downside.

As for Friday’s economic releases, during the Asian morning, we have Japan’s National CPIs. No forecast is currently available for the headline rate, while the core one is anticipated to have risen somewhat, but to have stayed in the negative territory. Specifically, it is expected to have inched up to -0.4% yoy from -0.6%. Later in the day, we get Canada’s retail sales for January. Both the headline and core mom rates are expected to have risen, but to have stayed in the negative territory.