Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

We have a very busy week ahead of us, with three central banks deciding on monetary policy: the BoJ, the BoC and the ECB. No major changes are expected, and thus, we will scan the accompanying statements for clues over their future policy plans. We also get several data from the UK, but GBP-traders may stay focused on Brexit as a new round of talks is set to begin. New Zealand’s CPIs and Australia’s employment data are also due to be released.

Monday is the week’s only light day, with no major events or economic releases scheduled on the economic agenda.

On Tuesday, during the Asian morning, Australia’s NAB business survey for June is coming out, but no forecast is currently available. Although this is not a major market mover, given the RBA’s emphasis on the labor market, we will pay attention to the Labor Costs index, which in May showed that wages slid 0.9% QoQ, after falling 2.7% in April. Further improvement, combined with a decent employment report on

Thursday may allow RBA policymakers to continue sitting comfortably on the sidelines.

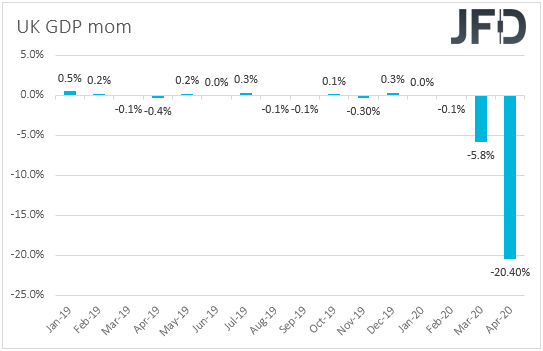

During the early European morning, we get the UK’s monthly GDP, as well as the industrial and manufacturing production rates, all for the month of May. No forecast is currently available for the GDP, but the industrial and manufacturing production rates are expected to have returned within the positive territory. Specifically, IP is expected to have rebounded 6.0% mom after sliding 20.3% in April, while MP is anticipated to have rebounded 8.0% mom after tumbling 24.3%. This would drive both the YoY rates up to -20.0% and -23.9%, from -24.4% and -28.5% respectively. The case for improving IP and MP is supported by the UK manufacturing PMI for the month, which rose to 40.7 from 32.6.

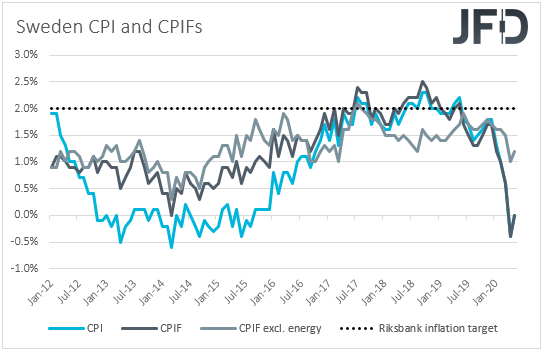

From Sweden, we have the inflation numbers for June. Both the headline CPI and CPIF rates are expected to have risen to +0.5% YoY from 0.0%, but as it is always the case, we prefer to pay more attention to the core CPIF metric, which excludes the volatile items of energy. That rate rose to +1.2% YoY in May from +1.0% in April.

Germany’s final CPIs for June are also due to be released, but as always, they are expected to confirm their preliminary estimates. The nation’s ZEW survey for July and Eurozone’s industrial production for May are also coming out. With regards to the ZEW survey, the current conditions index is expected to have risen to -65.0 from -83.1, while the economic sentiment one is anticipated to have slid to 60.0 from 63.4. Eurozone’s industrial production is forecast to have rebounded 14.5% mom after tumbling 17.1%.

Later in the day, we have the US CPIs for June. The headline rate is expected to have risen to +0.6% YoY from +0.1%, but the core one is anticipated to have ticked down to +1.1% YoY from +1.2%.

On Wednesday, two central banks decide on their respective monetary policy. During the Asian morning, we have the BoJ, while later in the day, it’s the turn of the BoC.

Kicking off with the BoJ, last time, Japanese officials maintained short-term interest rates at -0.1% and the target of the 10-year government bond yields at around 0% as was widely expected, noting that the economy will likely improve as the fallout from the pandemic subsides. That said, they noted that they are likely to increase the size of money pumped out via market operations and lending facilities to combat the virus, from the current JPY 75trln to JPY 110trln. Policymakers are not expected to proceed with any changes to their main policy tools this time either, but it would be interesting to see whether they will expand further some of their emergency lending programs. In any case, we doubt that the yen will react massively to this decision. We expect the safe-haven currency to stay mostly linked to headlines and developments surrounding the broader market sentiment, and especially anything surrounding the coronavirus.

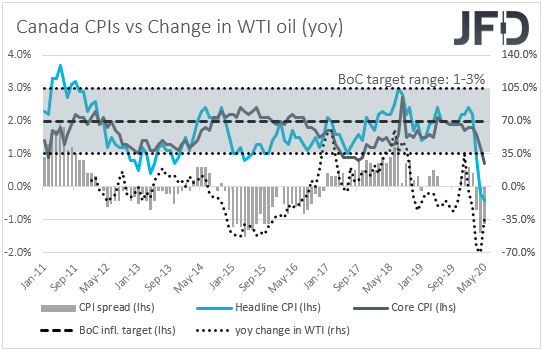

Passing the ball to the BoC, at its most recent meeting, it kept interest rates unchanged and said that given the improvement in short-term funding conditions, it reduced the frequency of its term repo operations and its program to purchase bankers’ acceptances. Officials also said that the Canadian economy appears to have avoided the most severe scenario presented in the Bank’s April Monetary Policy Report and that the economy is expected to resume to growth in the third quarter. That said, despite last week’s better-than-expected employment report, inflation remains very low, with the headline rate at -0.4% YoY. Therefore, with the Bank also publishing its updated economic projections, it would be interesting to see what officials’ plans are moving forward, even if they are not expected to act this time around.

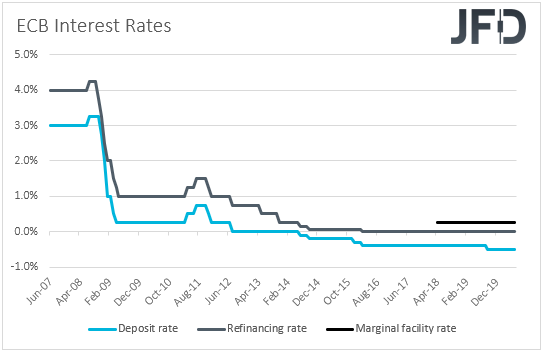

On Thursday, the central bank torch will be passed to the ECB. At its latest meeting, this Bank decided to increase its pandemic emergency purchase program (PEPP) by EUR 600bn to a total of EUR 1350bn, extending the horizon of the purchases to “at least the end of June 2021.” Officials also repeated that they remain ready to adjust all of their instruments as appropriate, to ensure that inflation moves towards their aim in a sustained manner.

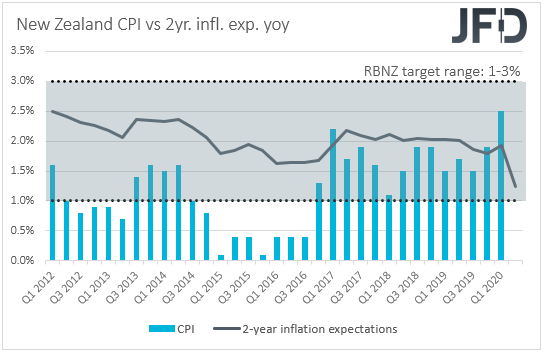

As for Thursday’s data, during the Asian morning, New Zealand’s CPI for Q2 is coming out. The forecast suggests that inflation slowed to +0.4% QoQ from +0.8%, something that will drive the YoY rate down to +2.1% from 2.5%.

Despite expectations over a slowdown, the YoY CPI rate is expected to stay near the midpoint of the RBNZ’s 1-3% target range, and also well above the Bank’s own forecast, which is at +1.3%. This may allow RBNZ policymakers to stand pat for another meeting, but with the Kiwi slightly higher against the dollar than it was the last time they met, we also expect them to reiterate concerns over its appreciation, as well as their readiness to ease further if needed.

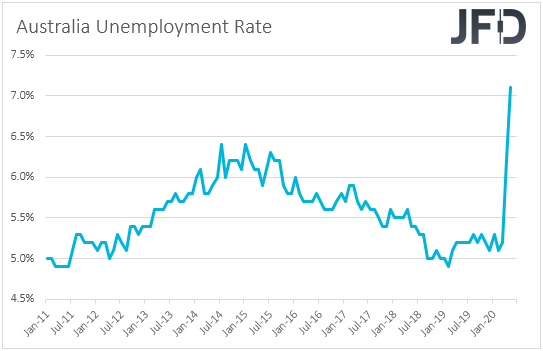

Australia's employment report for June is also coming out. The unemployment rate is expected to have ticked down to 7.0% from 7.1%, while the net change in employment is forecast to show that the economy has lost 100k jobs, less than the 227.7k loss in May. That said, the participation is expected to have increased to 63.7% from 62.9%, which combined with a slide in the unemployment rate suggests that the people who have joined the labor force may have actually found a job. This means that the employment change may come in positive this time around. Thus, we would consider the risks as tilted to the upside. As we already noted, a decent employment report may allow the RBA to avoid scaling back up its QE purchases, although we expect them to stay willing to do so if things fall out of orbit. The risk to that view is expanding QE purchases in light of the newly adopted lockdown measures in Melbourne. However, we believe that policymakers may prefer to wait for data to reveal weather this had a serious economic impact or not.

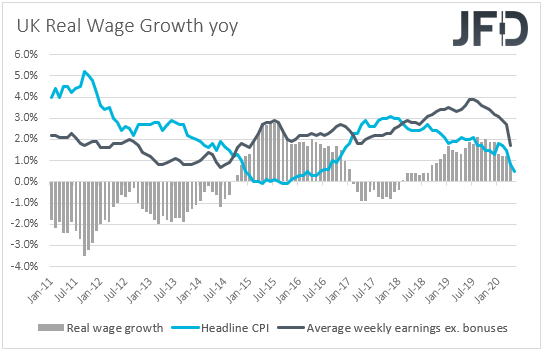

During the early European morning, we get the UK employment report for May. The unemployment rate is expected to have risen to 4.3% from 3.9%, while the net change in employment is forecast to show that the economy has lost 83k jobs in the three months to May, after gaining 6k in the three months to April. Average weekly earnings including bonuses are expected to have declined 0.3% YoY after increasing 1.0%, while the excluding bonuses rate is forecast to have declined to +0.7% YoY from +1.7%. The case for declining wages is also supported by the KPMG and REC UK report on jobs, where it was mentioned that weak demand for staff had driven down pay for the month. With the headline inflation rate falling to +0.5% YoY, a 0.7% wage growth would result in a slowdown in real wages, to +0.2% YoY from +0.9%.

Finally, on Friday, during the European morning, we have Eurozone’s final CPIs for June, but as it is always the case, they are expected to confirm their preliminary prints. Later, the US building permits and housing starts for June, as well as the preliminary UoM consumer sentiment index for July are coming out.

To be successful, active investors have to watch (and create) indicators that the mainstream media do not follow.Trading is hard, requiring discipline and a strict set of...

Most NFL general managers (GMs) are optimistic and displaying overconfidence today as they prepare for tomorrow’s NFL draft. The draft is a once-a-year opportunity for GMs to...

The bad news is that the contraction in the money supply appears to be over. That’s not bad news per se (see below), but it’s bad in that the anti-inflationary work...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.