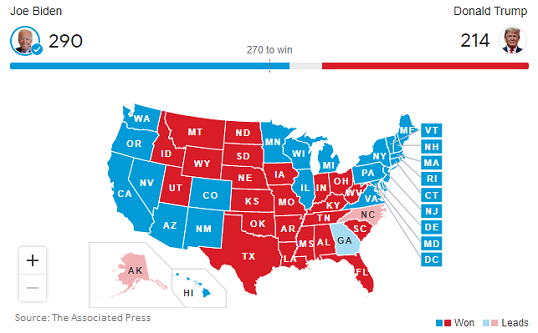

On Saturday, Joe Biden secured 290 electoral votes, officially winning the US presidential elections. Markets had been trading in a risk-on manner last week in anticipation of such a result, and they may continue trading in such fashion this week as well. We also have an RBNZ policy decision on Wednesday, but we don’t expect officials of this Bank to proceed with any action at this gathering.

On Monday, there are no top tier indicators on the economic agenda. Thus, we believe that market participants will still be digesting the outcome of the US elections. On Saturday, Joe Biden secured 290 electoral votes, officially wining the election race to become the 46th President of the United States. His victory was already largely priced in from last week, with equities around the globe and other risk-linked assets recording gains, as investors diverted flows out of the safe havens.

As we noted several times last week, a Biden victory is seen as positive for stock indices around the globe as it is believed that the Democrat will adopt a softer stance than Trump in handling the trade relationships of the US with the rest of the world. Indeed, at the time of writing, Asian indices are a sea of green. Although we said that a Biden presidency may prove negative for stocks in the US, due to his pledge to increase corporate taxes and tighten regulations, the fact that Republicans are likely to stay in control of the Senate allowed Wall Street to march higher as well.

This will make it hard for Biden to proceed with the aforementioned plans. In the FX world, Biden is seen as negative for the US dollar due to his fiscal agenda being looser than Trump’s. Yes, a Republican-controlled Senate may object any suggested package by Biden, but investors continue to sell dollars, perhaps in anticipation that this could pressure the Fed to step up its stimulus efforts at some point in the not-too-distant future.

On Tuesday, during the Asian morning, we get China’s CPI and PPI for the month of October. The CPI is expected to have slowed to 0.8% yoy from 1.7%, while the PPI rate is forecast to have ticked up to -2.0% from -2.1%.

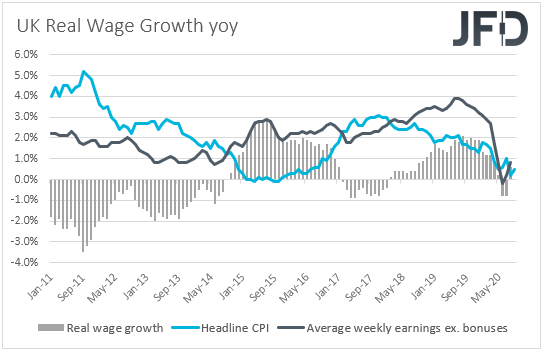

In the early European morning, the UK employment report for September is due to be released. The unemployment rate is forecast to have risen to 4.8% from 4.5%, while average weekly earnings including bonuses are expected to have increased 1.0% yoy after stagnating in August. The excluding bonuses rate is also anticipated to have risen, to 1.5% from 0.8%.

That said, according to the KPMG and REC UK report on jobs for September, starting salaries awarded to permanent workers continued to fall solidly, with the rate of decline accelerating slightly since August. Meanwhile, temp wages fell only modestly. With that in mind, we would consider the risks surrounding the earnings’ forecasts as tilted to the downside.

From Germany, we have the ZEW survey for November. Both the current conditions and economic sentiment indices are expected to have declined, to -65.0 and 40.0 from -59.5 and 56.1. At its latest meeting, the ECB noted that in December, the new macroeconomic projections will allow a thorough reassessment of the economic outlook and that the Governing Council will recalibrate its instruments as appropriate. In other words, the ECB is very likely to expand its stimulative efforts in December, and declining ZEW indices will only add to that likelihood.

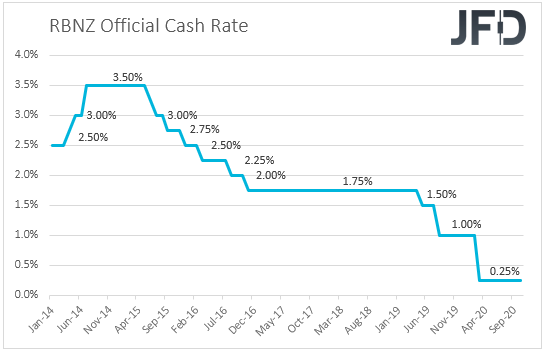

On Wednesday, during the Asian session, the RBNZ decides on monetary policy. When they last met, policymakers of this Bank kept their Official Cash Rate (OCR) and their Large-Scale Asset Purchase (LSAP) program unchanged, repeating that further monetary stimulus may be needed in the foreseeable future, including a Funding for Lending Program, a negative OCR, and purchases of foreign assets.

That said, a few weeks ago, RBNZ Assistant Governor Christian Hawkesby said that some economic data have surprised to the upside, reducing the chances for the adoption of negative interest rates by this Bank. However, he added that the discussion of negative rates is “not a game of bluff”, keeping the prospect well on the table.

With that in mind, we don’t expect the Bank to act at this gathering, but we do expect it to keep the prospect of further easing well on the table. Officials’ willingness to take interest rates into the negative territory if needed may hurt somewhat the Kiwi, but we expect the currency to stay mostly linked to developments surrounding the broader market sentiment. If the risk-on trading due to the outcome of the US elections continues, any RBNZ-related slide may stay limited and short-lived.

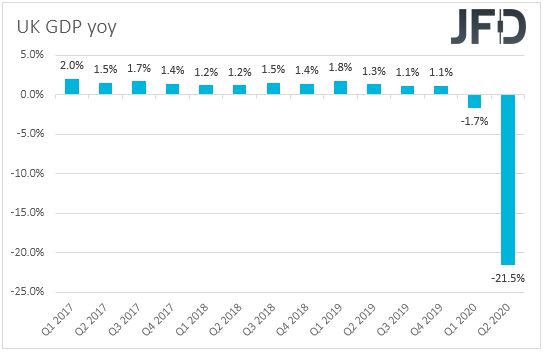

On Thursday, the first estimate of the UK GDP for Q3 is coming out and the forecast points to a 15.8% qoq rebound after a 19.8% tumble in Q2. This will drive the yoy rate up to -9.4% from -21.5%. The nation’s industrial and manufacturing production rates for September are also due to be released and expectations are for both to have improved in yoy terms, but to have stayed in the negative territory.

In any case, we don’t expect this week’s data to prove determinant with regards to the pound’s forthcoming direction. We stick to our guns that traders of the British currency are likely to keep their gaze locked on developments surrounding the Brexit landscape.

Negotiations over a post-Brexit trade accord between the UK and the EU are set to continue this week, with both sides appearing willing to work hard in order to reach common ground. With all that in mind, anything suggesting that a deal could be found in the next few weeks may prove supportive for the currency, while signs that the differences-gap is not narrowing may result in weakness.

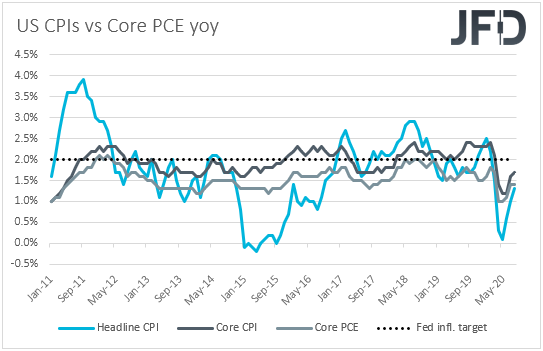

Later in the day, we have the US CPIs for October. The headline rate is forecast to have ticked down to +1.3% yoy from +1.4%, while the core one is anticipated to have held steady at +1.7%. In our view, a downtick in the headline rate is unlikely to increase speculation with regards to additional easing by the Fed in December, especially after Friday’s better-than-expected employment data.

Therefore, we don’t expect the dollar to react much on this release, rather we believe that its driver may continue to be the outcome of the US election. Namely, after Biden’s victory, the dollar may continue to drift lower.

Finally, on Friday, Eurozone’s 2nd estimate of GDP for Q3, and the employment change for the quarter are coming out. The 2nd estimate of GDP is forecast to confirm its preliminary print of 12.7% qoq, while no forecast is available for the employment change.

Later, from the US, we get the PPIs for October and the preliminary UoM consumer sentiment index for November. Both the headline and core PPI rates are expected to have held steady at +0.4% yoy and +1.2% yoy respectively, while the UoM index is forecast to have risen fractionally, to 82.0 from 81.8.