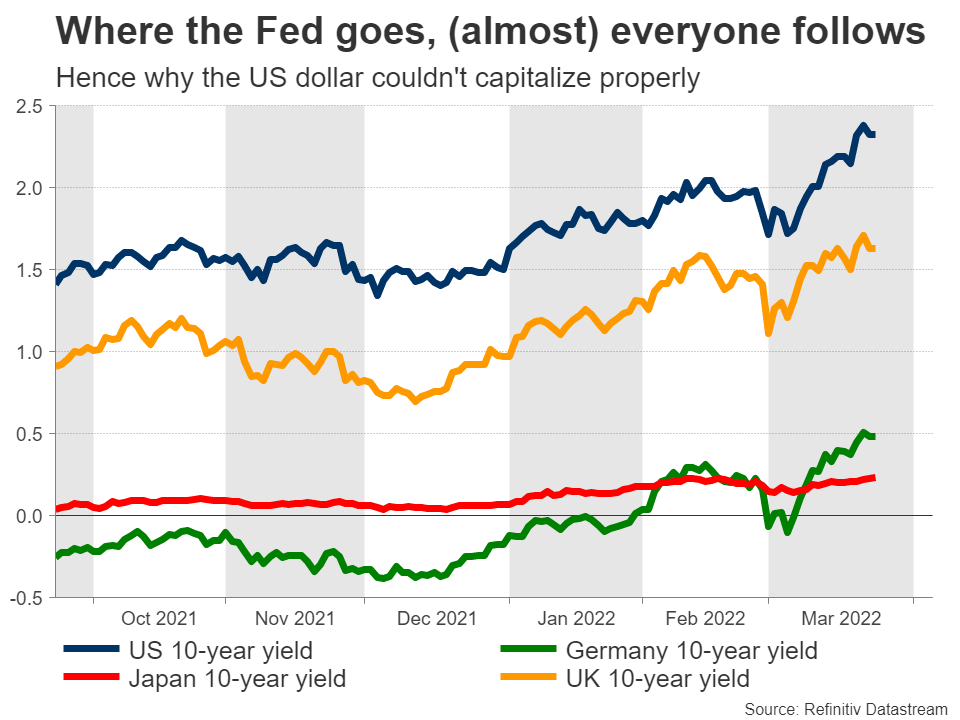

Fed leads the pack

Fed officials are saying they are prepared to do whatever it takes to cool inflation. That means raising interest rates as quickly as possible to slow down the US economy, hopefully without tipping it into recession. This message rocked global markets lately.

Treasury yields went through the roof, eclipsing pre-pandemic levels as traders scrambled to price in faster tightening. Another seven and a half quarter-point rate increases are now baked in for this year, which would push the federal funds rate to around 2.25% by December.

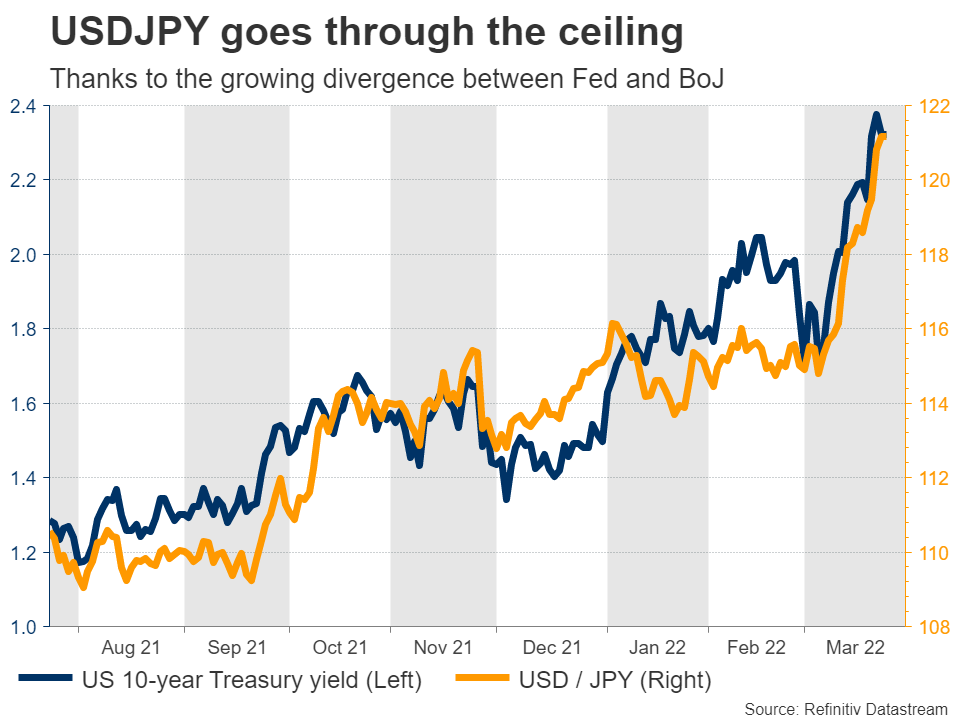

With US yields powering higher, one would have expected the dollar to bulldoze its way through the FX arena. But that hasn’t really happened. Instead of the dollar strengthening, it is the yen that has been demolished. This boils down to a signaling effect.

When the Fed hits the brakes, everyone else is expected to follow suit. Even in Europe, traders have cranked up their bets for rate hikes lately, propelling European yields higher. While the ECB will be slower than the Fed, this repricing has been enough to negate the impact on euro/dollar.

The yen is the exception to this rule as the Bank of Japan is the only major central bank that’s not expected to raise rates this year. It also remains committed to its yield curve control strategy, which prevents Japanese yields from rising beyond a certain level and therefore makes the yen less attractive as foreign yields soar.

Dollar turns to nonfarm payrolls

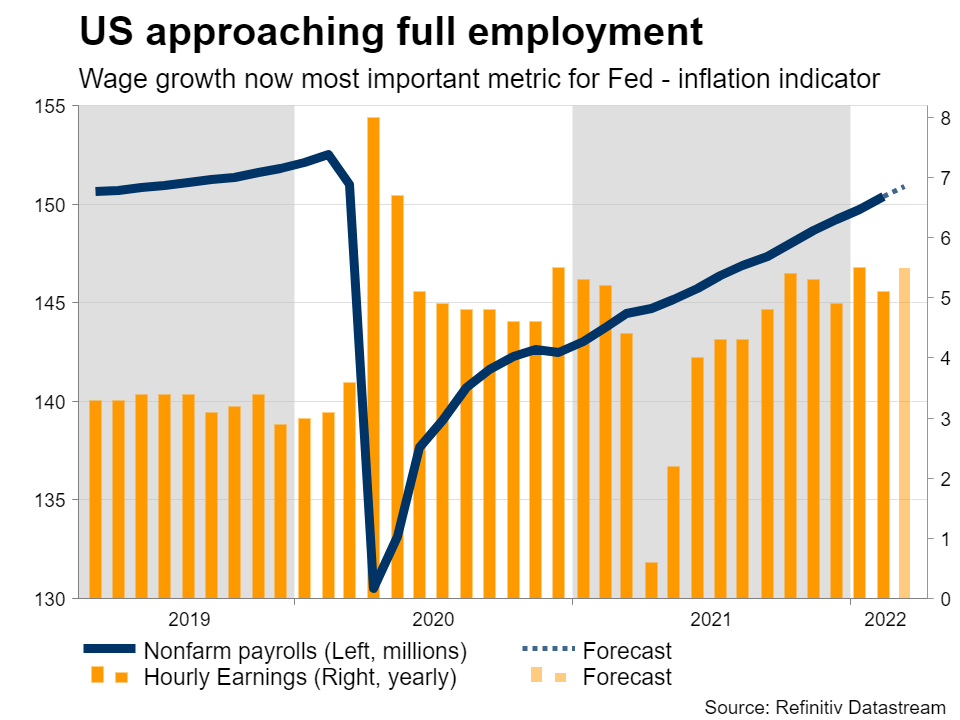

The main event next week will be the US employment report for March, due on Friday. Forecasts point to another solid month for the labor market. Nonfarm payrolls are expected to clock in at 450k, pushing the unemployment rate down one tick to 3.7%. Wage growth is also expected to pick up steam.

With the economy approaching full employment, wage growth is now the most important metric for the Fed. It is considered an early indicator of what inflation will do in the future, so it’s crucial for how many rate hikes are required.

So far, early employment indicators point to a stellar report. Jobless claims fell substantially during the survey week and the composite Markit PMI report showed that the rate of job creation was the sharpest in a year.

Investors are split on whether the Fed will raise rates another seven or eight times this year, so a solid report could help tip the scales towards eight and by extension re-energise the dollar’s rally.

Aside from the employment report, the ISM manufacturing PMI for March will also be released on Friday. The core PCE price index will be published one day earlier, but this is not a market mover.

Hot inflation unlikely to save euro

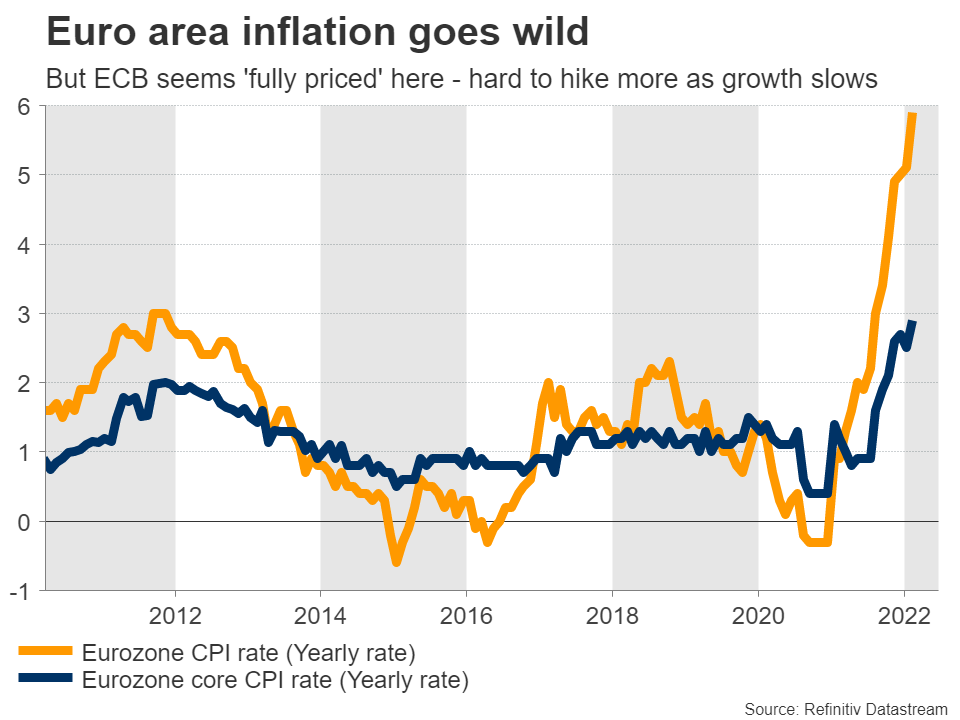

In the Eurozone, preliminary CPI inflation stats for March will hit the markets on Friday. With the war in Ukraine catapulting raw material prices higher and PMI surveys suggesting businesses raised their selling prices at a new record pace, it is safe to assume the yearly CPI rate will edge higher than the 5.9% it printed in February.

But perhaps not much higher. This is the period when inflation really started to heat up last year, so going forward, it will be much harder for the yearly CPI rate to keep rising so dramatically as tougher base effects kick in.

For the euro, even a very hot print is unlikely to change much. Money markets are already pricing in two rate hikes from the ECB this year, which is probably as much as the central bank can do without breaking the economy.

Growth is already slowing down as consumers get squeezed by rising energy and food costs. Stepping on the policy brakes too hard would raise the risk of recession even further. That’s a gamble the ECB wants to avoid.

For now, the main variable for the euro is whether there’s a ceasefire in Ukraine soon. That would set the stage for a relief rally. However, it’s going to be difficult to sustain any rally until the growth outlook improves.

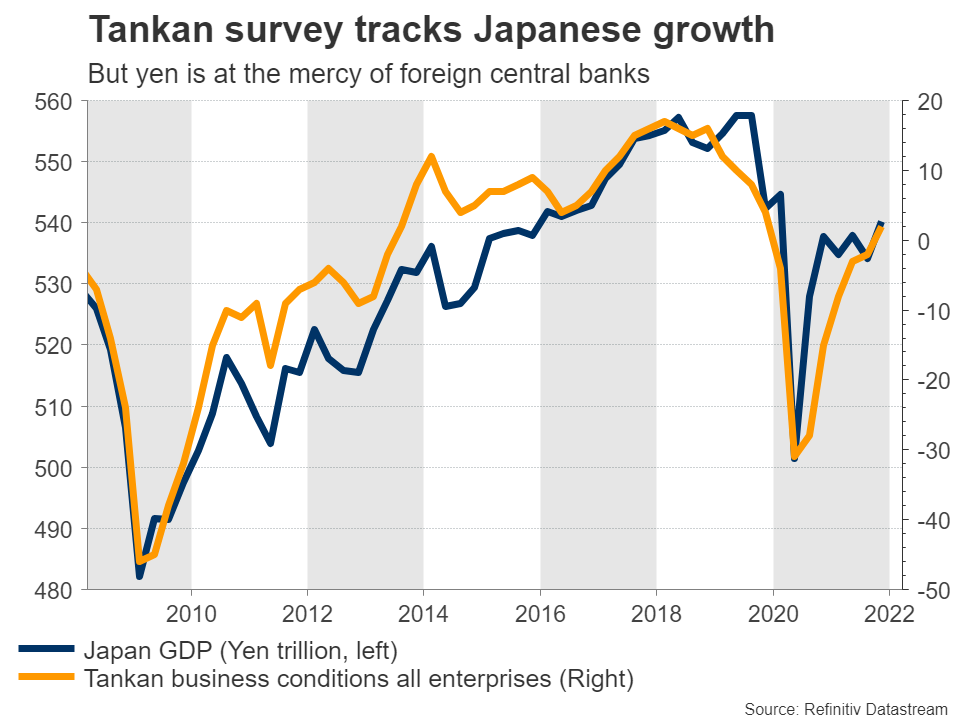

Japan’s Tankan and Chinese PMIs

The Bank of Japan will also release its quarterly Tankan survey on Friday. Forecasts suggest businesses are becoming less optimistic as they grapple with soaring energy prices and geopolitical uncertainty. As for the yen, it’s difficult to envision a trend reversal until the BoJ joins the global normalization party.

In China, the official PMIs for March are out on Thursday and are likely to reflect the latest lockdowns across Chinese cities. On the bright side, the government has pledged to open the spending taps to support the economy.

With Chinese authorities promising more stimulus and commodity prices surging, the Australian dollar has come back to life. The Australian economy has recovered too, with the unemployment rate reaching record lows lately.

That said, markets are already pricing in the first RBA rate increase for June and a total of eight hikes for the year. This seems overly aggressive considering that wages haven’t fired up yet and the RBA continues to preach patience.