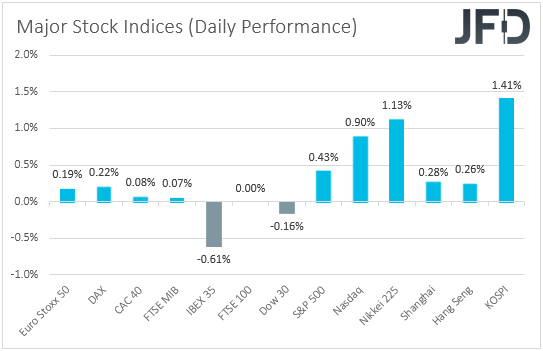

Both the S&P 500 and NASDAQ climbed to fresh records on Monday, perhaps due to the dovish remarks by Fed Chief Powell in his Jackson Hole speech on Friday. That said, in our view, market participants are likely to get more careful as we get closer to Friday’s US jobs data for August. As for today, the main item on the economic agenda may be Eurozone’s CPIs for August, but with an ECB pledged to stay accommodative for long, we don’t expect an acceleration to prove a game changer for the euro.

Powell's Jackson Hole Remarks Boost Risk Appetitie

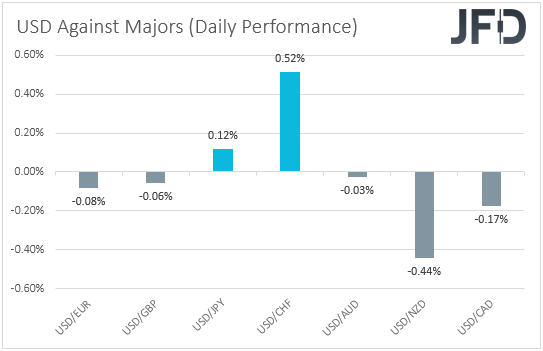

The US dollar traded mixed against the other major currencies on Monday and during the Asian session Tuesday. It gained only versus CHF and JPY, while it underperformed against NZD and CAD. The greenback was found nearly unchanged, within a ±0.10% range, against EUR, GBP, and AUD.

The weakening of the safe havens yen and franc, combined with the strengthening of the commodity-linked Kiwi and Loonie, suggests that markets traded in a risk-on manner yesterday and today in Asia. European shares traded slightly higher or unchanged from their opening levels as a UK holiday may have resulted in a subdued trading activity. However, later, during the US session, market appetite was boosted further, with the S&P 500 and NASDAQ hitting fresh record highs, although Dow Jones slid somewhat. As for today in Asia, sentiment remained supported.

The driver behind the new records in the S&P 500 and NASDAQ may have been the cautious remarks by Fed Chair Powell on Friday at the Fed’s Jackson Hole Symposium. The Committee’s Head acknowledged the progress of the US economy towards their objectives but refrained from providing clear signals with regards to when they may begin tapering their QE purchases. He added that he wants to avoid chasing “transitory” inflation and potentially discouraging jobs growth in the process. This gave the green light to investors to buy more stocks as a delayed and slower process could mean later rate hikes, and thereby low borrowing costs for companies for longer. Lower interest rates also mean higher present values for companies the valuation of which is based on discounted expected future cash flows.

That said, market participants are likely to get more careful as we get closer to Friday’s US jobs data for August. Expectations are for another strong report, which may raise the volume of the hawkish voices among the FOMC, something that may result in a majority vote in favor of tapering sooner than Powell thinks. Therefore, a decent employment report on Friday may be the catalyst for a rebound in the US dollar, which came under selling interest following Powell’s Jackson Hole remarks. Equities could pull back, but we don’t expect a major trend reversal, as improving data also mean better economic recovery, which is encouraging for equity traders.

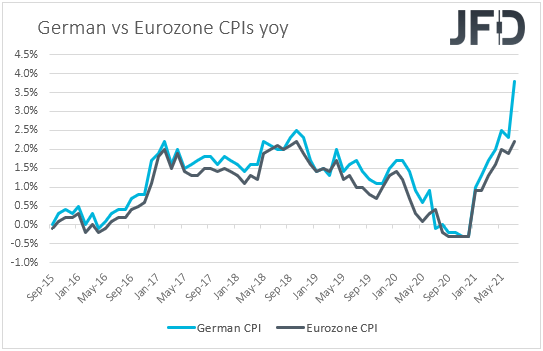

As for today, the main item on the agenda may be Eurozone’s CPIs for August. The headline rate is expected to have moved further above the 2% mark. Specifically, it is expected to have risen to +2.8% yoy from +2.2%. The HICP excluding energy and food rate is also expected to have risen, but to have stayed below 2%. The forecast is for a rise to +1.4% yoy from +0.9%.

At its latest gathering, the ECB kept all of its settings untouched, but changed its forward guidance, saying that it will keep interest rates at present or lower levels until it sees inflation reaching 2% well ahead of the end of its projection horizon, which may also imply a period during which inflation moderately overshoots that objective. In our view, this translates into willingness to hold rates low for much longer than the previous guidance suggested. Yes, accelerating inflation could bring forth the hike timing, but bearing in mind that the preliminary Euro area PMIs for August slid by more than anticipated, and also that underlying inflation is still expected to stay decently below 2%, we don’t expect ECB officials to change their minds with regards to their future policy plans. With the ECB pledged to stay accommodative for long, we see the case for the euro to stay under pressure against currencies the central banks of which are expected to start normalizing their respective policies soon, the likes of the Kiwi and, conditional upon a strong NFP report on Friday, the US dollar.

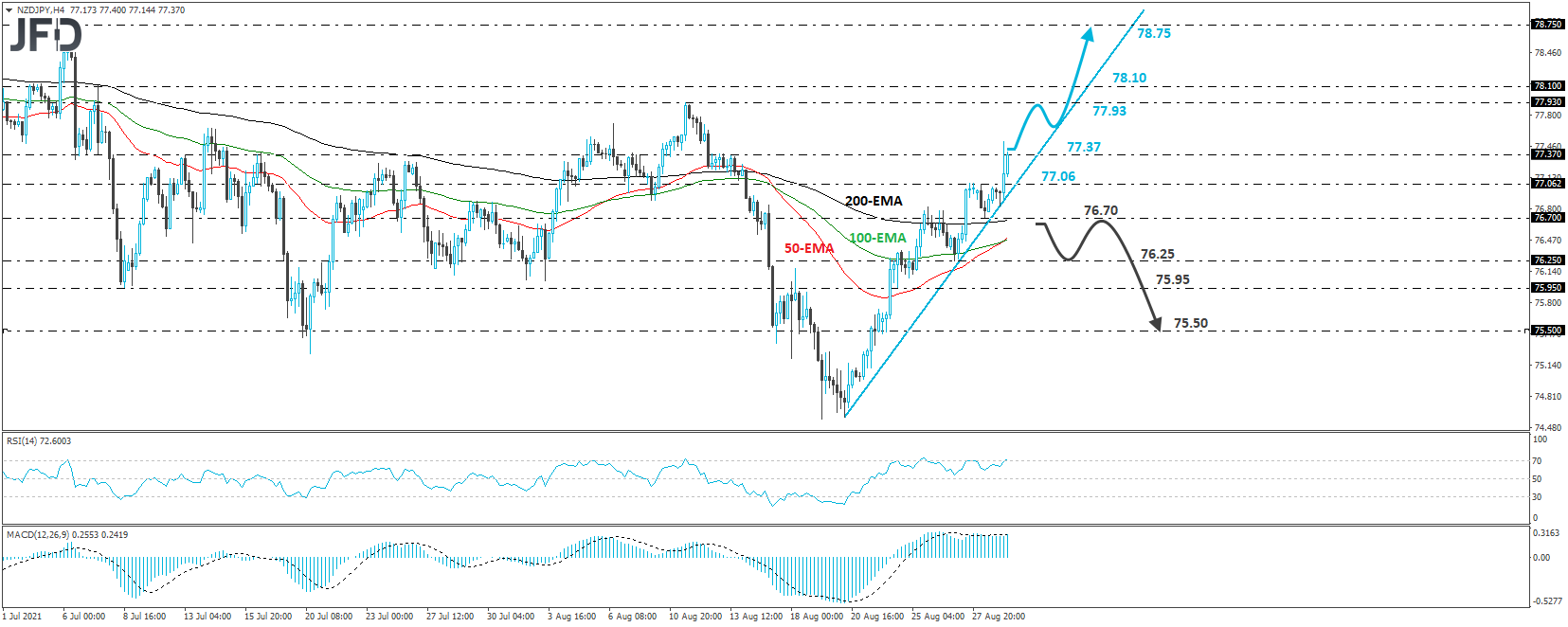

NZD/JPY Technical Outlook

NZD/JPY edged north during the Asian session today, after hitting support at the upside line drawn from the low of Aug. 20. As long as the rate continues to trade above that line, we would consider the short-term picture to be positive.

At the time of writing, NZD/JPY is testing the 77.37 resistance zone, market by the high of Aug. 13, the break of which could pave the way towards the 77.93 barrier, marked by the high of Aug. 11t or the 78.10 territory, defined by the peak of July 7. If the bulls don’t stop there, then we could see them pushing towards the peak of July 6, at 78.75.

On the downside, we would like to see a dip below 76.70, yesterday’s low, before we start examining the case of a bearish reversal. The rate would also be below the aforementioned upside line, with the bears perhaps driving the action towards the low of Aug. 27, at 76.25, or the 75.95 barrier, marked by an intraday swing low formed on Aug. 24. Another dip, below the latter level could carry declines towards the low of that day, at around 75.50.

EUR/NZD Technical Outlook

EUR/NZD fell during the Asian session today, breaking below the 1.6810 barrier, marked by Aug. 27, thereby confirming a forthcoming lower low. That said, the decline was stopped by the 1.6735 level and then, the rate rebounded somewhat. In any case, EUR/NZD continues to trade below the downside resistance line drawn from the high of Aug. 23 and thus, we would consider the short-term outlook to be negative.

We would expect the bears to retest the 1.6735 level soon, where a break could pave the way towards the low of Aug. 11, at 1.6640. They may decide to take a break after reaching that area, thereby allowing a corrective bounce, but they could recharge from near the downside line, and eventually break the 1.6640 zone.

This could see scope for extensions toward the 1.6350 territory, defined as a support by the low of Mar. 16.

On the upside, we would like to see a rebound back above 1.6880 before we start examining whether the outlook has turned bullish. This may confirm the break above the downside line taken from the high of Aug. 23, and could initially target the 1.6950 zone, marked by the highs of Aug. 25 and 27. Another break above that level could aim for the 1.7010 barrier, which is the inside swing low of Aug. 23, but if the bulls do not stop there, we may experience larger advances, towards the peak of 1.7140.

As For The Rest Of Today's Events

Germany’s unemployment rate for August is also coming out and the forecast points to a downtick to 5.6% from 5.7%.

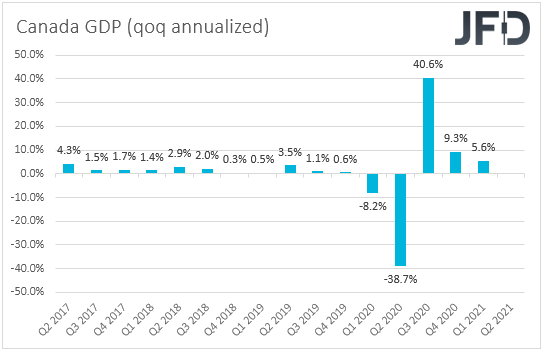

Later in the day, we have Canada’s GDP for Q2 and June. The qoq annualized rate is expected to have slid to +2.5% from +5.6%, but the monthly rate for June is expected to have risen to +0.7% from -0.3%.

At its prior gathering, the BoC appeared less hawkish than expected, saying that they continue to see the output gap closing in H2 2022, which suggests that their expectations over when they may start raising interest rates have not come forth. What’s more, both the headline and core Canadian inflation rates for July declined, while the employment report for the month fell short of its own forecasts, which may have added credence to that view. However, the Canadian dollar enjoyed decent gains in the last 10 days, perhaps driven by the rebound in oil prices. Therefore, we believe that the currency is likely stay linked mainly to that instead of data releases.

From the US, we get the Conference Board consumer sentiment index for August, which is forecast to have slid to 124.0 from 129.1.