Bernanke puts everyone to sleep at town hall meeting in Michigan, offers no surprises. In Japan, a government minister’s comments fretting excessive JPY weakness trigger a sharp dip in JPY crosses.

Bernanke’s performance last night failed to provide anything of note as he basically pedantically rehashed why the Fed is doing what is doing and expressed “cautious optimism” on the course of the economy and confidence that Fed policy had done good. When asked good questions like whether the Fed’s actions were aiding the irresponsible behaviour of the US government, he completely evaded the question. No real policy hints or feelings of the mood among FOMC members were relayed to the audience, so the USD drifted lower again overnight, especially hit by USD/JPY selling on developments in Japan.

Japan’s economy minister Amari noted (I noted this yesterday!) that excessive JPY weakness would cause a spike in import prices and expressed concern for “people’s livelihoods.” The comments are probably not aimed at halting the JPY’s weakness, but perhaps the pace of the currency’s declines is causing some degree of caution among Japanese officialdom.

The JPY hit a three day low versus the USD in the wake of these comments as the market wonders if it has taken things too far, too fast. A stable to slightly rallying bond market was also supportive of the JPY strengthening move.

Chart: USD/JPY

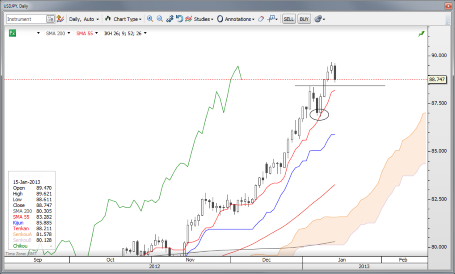

Last time I looked for USD/JPY support, the Ichimoku Tenkan line proved the important trend support. That line currently comes in at around 88.20, which is just below the flatline support at 88.40. Below that, we have endless territory to traverse in the event large Fibonacci retracements come into play starting with the 0.382 for the move from below 82 to the recent 89.67 high at 86.62.

USD/JPY" title="USD/JPY" width="455" height="274" />

USD/JPY" title="USD/JPY" width="455" height="274" />

With the unwinding of eurozone tail risks, EUR/CHF is finally on the move, trading at new highs overnight and into this morning. I prefer for moves in this pair to take place during European trading hours if I am to believe they are sustainable.

The fact that so much of the move took place overnight on no specific news is a bit fishy, i.e., this represents a running of stops in thin trading hours that could leave to an air-pocket now to the downside in the shortest term. Still, the aggravation of the rally suggests perhaps that market participants have been too short the cross previously. If Euro spreads continue to improve, we could see this continue higher to test the 1.2475 high that came after the 1.20 floor declaration. 1.2400 last traded in December 2011.

I noticed this article from Bloomberg on hedge fund leverage at new highs since 2004 with great interest. As well, the article says that “margin debt at NYSE firms rose in November to the most since February 2008” – that was a few months before the epic crash of 2008 got underway.

There’s something ironic about a low volatility environment like the one we have seen of late. It usually means that risk takers will put on more leverage, which this article bears out. And higher leverage actually increases risk even as the apparent risk is very low. In other words – the best cure for low volatility is high leverage because low apparent risk means market participants quickly become overaggressive. High leverage can only mean danger ahead – it’s just a question of timing.

So be careful out there and watch out for the US data up at 1330 GMT.

Economic Data Highlights

Bernanke’s performance last night failed to provide anything of note as he basically pedantically rehashed why the Fed is doing what is doing and expressed “cautious optimism” on the course of the economy and confidence that Fed policy had done good. When asked good questions like whether the Fed’s actions were aiding the irresponsible behaviour of the US government, he completely evaded the question. No real policy hints or feelings of the mood among FOMC members were relayed to the audience, so the USD drifted lower again overnight, especially hit by USD/JPY selling on developments in Japan.

Japan’s economy minister Amari noted (I noted this yesterday!) that excessive JPY weakness would cause a spike in import prices and expressed concern for “people’s livelihoods.” The comments are probably not aimed at halting the JPY’s weakness, but perhaps the pace of the currency’s declines is causing some degree of caution among Japanese officialdom.

The JPY hit a three day low versus the USD in the wake of these comments as the market wonders if it has taken things too far, too fast. A stable to slightly rallying bond market was also supportive of the JPY strengthening move.

Chart: USD/JPY

Last time I looked for USD/JPY support, the Ichimoku Tenkan line proved the important trend support. That line currently comes in at around 88.20, which is just below the flatline support at 88.40. Below that, we have endless territory to traverse in the event large Fibonacci retracements come into play starting with the 0.382 for the move from below 82 to the recent 89.67 high at 86.62.

USD/JPY" title="USD/JPY" width="455" height="274" />With the unwinding of eurozone tail risks, EUR/CHF is finally on the move, trading at new highs overnight and into this morning. I prefer for moves in this pair to take place during European trading hours if I am to believe they are sustainable.

The fact that so much of the move took place overnight on no specific news is a bit fishy, i.e., this represents a running of stops in thin trading hours that could leave to an air-pocket now to the downside in the shortest term. Still, the aggravation of the rally suggests perhaps that market participants have been too short the cross previously. If Euro spreads continue to improve, we could see this continue higher to test the 1.2475 high that came after the 1.20 floor declaration. 1.2400 last traded in December 2011.

I noticed this article from Bloomberg on hedge fund leverage at new highs since 2004 with great interest. As well, the article says that “margin debt at NYSE firms rose in November to the most since February 2008” – that was a few months before the epic crash of 2008 got underway.

There’s something ironic about a low volatility environment like the one we have seen of late. It usually means that risk takers will put on more leverage, which this article bears out. And higher leverage actually increases risk even as the apparent risk is very low. In other words – the best cure for low volatility is high leverage because low apparent risk means market participants quickly become overaggressive. High leverage can only mean danger ahead – it’s just a question of timing.

So be careful out there and watch out for the US data up at 1330 GMT.

Economic Data Highlights

- New Zealand December REINZ House Price Index fell -06% MoM

- UK December RICS House Price Balance out at 0% vs. -8% expected and -9% in November

- Japan December Machine Tool Orders out at -27.5% YoY vs. -21.3% in November

- Norway December Trade Balance out at +35.2B vs. +31.9B in November

- UK December PPI Input/Output out at -0.2%/-0.1% MoM vs. 0.0%/0.0% expected, respectively

- UK December CPI out at +0.5% MoM and +2.7% YoY as expected and vs. +2.7% YoY in November

- UK December RPI out at +0.5% MoM and +3.1% YoY vs. +0.4%/+3.0% expected, respectively and vs. +3.0% YoY in November

- Eurozone November Trade Balance (1000)

- UK BoE’s King, other BoE officials to Testify (1000)

- US Fed’s Rosengren to Speak (1300)

- US January Empire Manufacturing (1330)

- US December Advance Retail Sales (1330)

- US December Producer Price Index (1330)

- US Fed’s Kocherlakota to Speak (1350)

- Canada December Existing Home Sales (1400)

- US November Business Inventories (1500)

- US Fed’s Plosser to Speak (1730)

- US Weekly API Crude Oil and Product Inventories (2130)

- Australia January Westpac Consumer Confidence (2330)

- Japan December Domestic Corporate Goods Price Index (2350)

- Japan December Machine Orders (2350)

- Japan December Consumer Confidence (0500)