The AUD/USD is testing above 1.0500, and the EUR/USD is checking out the first major retracement levels ahead of a key batch of FOMC minutes up this evening. Meanwhile, new JPY lows continue.

The U.S. dollar continues to struggle, as it has regressed back to trading like the flipside of risk appetite now that the “US leading the recovery” story has been at least dented, if not smashed, by the latest round of weak U.S. data. The euro is strong as the ECB remains in a holding pattern (wildly hawkish compared to the exuberant money printing from, in order from least to most, the BoE, the Fed, and especially the BoJ). Japanese investors, long used to a bond-investing mentality, may look at the fat yields available at the European periphery and want in on the action. The damage this will inflict on Europe from a strong currency/weak demand perspective is obvious, and the political resistance to further EUR/JPY appreciation will accelerate from here. It’s always a question of how long trends can extend before they are exhausted. One also wonders how far we are from an ECB easing of any kind.

Zero Hedge reposted an interesting piece by Chris Martenson: he says the BoJ is is essentially eroding trust in the Japanese currency ,and scaring savers out of holding cash. As he and the likes of Richard Koo have said, expanding the monetary base in an economy like the current one in Japan or the U.S. does not have the textbook effect it is supposed to have at present. It certainly is a risky experiment, particularly as JGB volatility remains very high. JGB’s sold off sharply again overnight after a couple of recent trading interruptions, and were limit down at one point for 10-years. The belly of the Japanese yield curve is actually higher relative to where it was several months ago than the long end of the curve, which came down ahead of Kuroda’s Big Move, as 5-year JGB yields are closing in on 1-year highs – admittedly that only means they are trading at 26 basis points. Let’s call 50 basis points “really interesting”. The 3-year high, by the way, was 2010’s 64 bps.

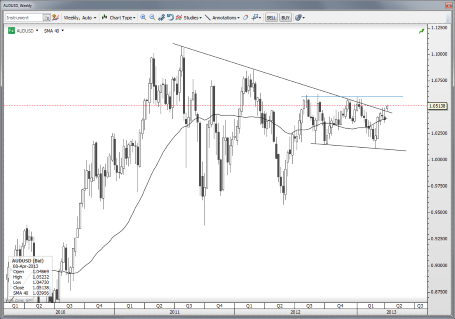

Chart: AUD/USD

The AUD/USD pair is breaking through local resistance at 1.0500, and having another go at that long-standing descending line of consolidation as the currency world goes risk-happy. Non-believers in the rally will note that we’re still below that near term 1.0600 range resistance level, and that the short end of the yield curve in Australia has failed to support this move from a fundamental perspective – quite the opposite, in fact. AUD buyers are now probably more focused on playing AUD versus the weak JPY and on the strength in equities and commodities – particularly metals. Keep a look out for the latest Australia employment report tonight after last month’s crazy positive outlier – these tend to mean revert.

AUD/USD" title="AUD/USD" width="455" height="319" />

AUD/USD" title="AUD/USD" width="455" height="319" />

Looking ahead

All eyes on tonight’s FOMC meeting, where we get the latest mix of opinions from FOMC members on the benefits and risks of Fed policy. The dissenting contingent is fairly large, but not the ones in power. These minutes are three weeks old, so at the time, the committee wouldn’t have seen some of the latest, rather discouraging numbers from the U.S. economy. The dollar has been on such a steep tumble over the last several days that it is hard to imagine the minutes providing any further fuel for the sell-off.

Economic Data Highlights

The U.S. dollar continues to struggle, as it has regressed back to trading like the flipside of risk appetite now that the “US leading the recovery” story has been at least dented, if not smashed, by the latest round of weak U.S. data. The euro is strong as the ECB remains in a holding pattern (wildly hawkish compared to the exuberant money printing from, in order from least to most, the BoE, the Fed, and especially the BoJ). Japanese investors, long used to a bond-investing mentality, may look at the fat yields available at the European periphery and want in on the action. The damage this will inflict on Europe from a strong currency/weak demand perspective is obvious, and the political resistance to further EUR/JPY appreciation will accelerate from here. It’s always a question of how long trends can extend before they are exhausted. One also wonders how far we are from an ECB easing of any kind.

Zero Hedge reposted an interesting piece by Chris Martenson: he says the BoJ is is essentially eroding trust in the Japanese currency ,and scaring savers out of holding cash. As he and the likes of Richard Koo have said, expanding the monetary base in an economy like the current one in Japan or the U.S. does not have the textbook effect it is supposed to have at present. It certainly is a risky experiment, particularly as JGB volatility remains very high. JGB’s sold off sharply again overnight after a couple of recent trading interruptions, and were limit down at one point for 10-years. The belly of the Japanese yield curve is actually higher relative to where it was several months ago than the long end of the curve, which came down ahead of Kuroda’s Big Move, as 5-year JGB yields are closing in on 1-year highs – admittedly that only means they are trading at 26 basis points. Let’s call 50 basis points “really interesting”. The 3-year high, by the way, was 2010’s 64 bps.

Chart: AUD/USD

The AUD/USD pair is breaking through local resistance at 1.0500, and having another go at that long-standing descending line of consolidation as the currency world goes risk-happy. Non-believers in the rally will note that we’re still below that near term 1.0600 range resistance level, and that the short end of the yield curve in Australia has failed to support this move from a fundamental perspective – quite the opposite, in fact. AUD buyers are now probably more focused on playing AUD versus the weak JPY and on the strength in equities and commodities – particularly metals. Keep a look out for the latest Australia employment report tonight after last month’s crazy positive outlier – these tend to mean revert.

AUD/USD" title="AUD/USD" width="455" height="319" />Looking ahead

All eyes on tonight’s FOMC meeting, where we get the latest mix of opinions from FOMC members on the benefits and risks of Fed policy. The dissenting contingent is fairly large, but not the ones in power. These minutes are three weeks old, so at the time, the committee wouldn’t have seen some of the latest, rather discouraging numbers from the U.S. economy. The dollar has been on such a steep tumble over the last several days that it is hard to imagine the minutes providing any further fuel for the sell-off.

Economic Data Highlights

- Australia Apr. Westpac Consumer Confidence out at 104.9 vs. 110.5 in Mar.

- China Mar. Trade Balance out at -$0.88B vs. +$15.15B expected and +$15.25B in Feb.

- France Feb. Industrial Production out at +0.7% MoM and -2.5% YoY vs. +0.2%/-3.9% expected, respectively and vs. -3.6% YoY in Jan.

- Spain Feb. Industrial Output out at -6.5% YoY vs. -4.9% expected and vs. -4.9% in Jan.

- Sweden Feb. Industrial Production out at +0.5% MoM and -0.9% YoY vs. +1.0%/-1.9% expected, respectively and vs. -8.0% YoY in Jan.

- Sweden Feb. Industrial Orders out at +3.5% MoM and +2.1% YoY vs. -5.7% YoY in Jan.

- Italy Feb. Industrial Production out at -0.8% MoM and -3.8% YoY vs. -0.5%/-4.0% expected, respectively and vs. -3.4% YoY in Jan.

- Norway Mar. CPI out at +0.3% MoM and +1.4% YoY vs. +0.4%/+1.3% expected, respectively and vs. +1.0% YoY in Feb.

- Norway Mar. CPI Underlying out at +0.2% MoM and +0.9% YoY vs. +0.4%/+1.1% expected, respectively and vs. +1.1% YoY in Feb.

- US Fed’s Lockhart to be interviewed (1130)

- US Weekly DoE Crude Oil and Product Inventories (1430)

- US FOMC Minutes (1800)

- US Fed’s Fisher to Speak (2100)

- New Zealand Mar. Business NZ PMI (2230)

- Japan Mar. Domestic CGPI (2350)

- Japan Feb. Machine Orders (2350)

- Australia Mar. Employment Change/Unemployment Rate (1030)