- Dollar gains as NFPs beat estimates

- But June pause probability stays unmoved as wages slow

- RBA faces dilemma to hike or stay sidelined

- Saudi Arabia pledges oil cuts from July

Dollar rebounds as US economy adds 339k jobs

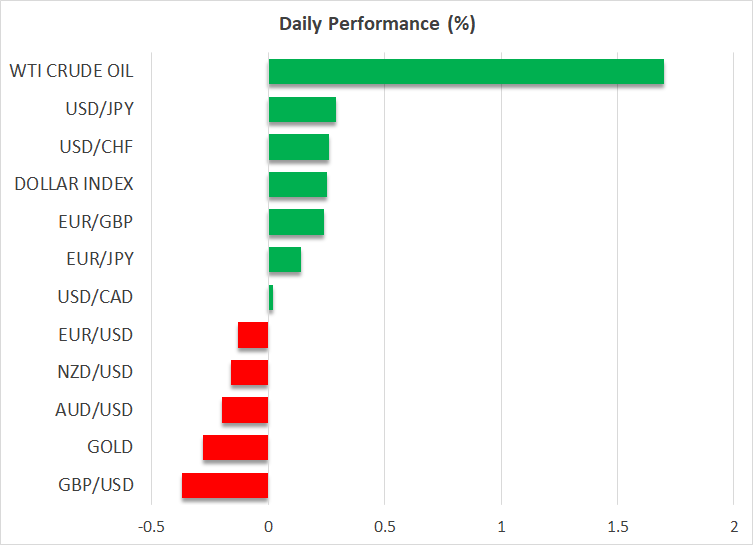

The US dollar traded higher against most of its major peers on Friday and continued to gain today after the US employment report revealed that the economy added 339k jobs in May, up from an upwardly revised 294k in April, and much more than the 180k forecast.

The stellar employment gains may have added credence to the “higher for longer” narrative regarding interest rates in the US, but it was not enough to boost expectations about a potential rate increase in June. Although investors are now pricing in 20bps worth of a hike by July compared to 18bps ahead of the jobs data, they continue to assign a 70% probability for a June pause.

The Achilles’ heel of the report may have been the increase in the unemployment rate to 3.7% from 3.4%, as well as the slowdown in wage growth. Coming on top of a downside revision in the Unit Labor Costs index for Q1, and other surveys corroborating the case of a slowdown in May’s wages, Friday’s data may have bolstered speculation that inflation could ease further in the months to come and that, consequently, there is no need for officials to rush on interest rates.

The next test for the US dollar may be the ISM non-manufacturing PMI for May, due out later today. The index is expected to have ticked down to 51.8 from 51.9, but traders may pay extra attention to the prices subindex, where a notable decline could further validate the view that inflation may drift south faster than previously thought. Nonetheless, the release that could prove determinant on how the Fed could proceed henceforth is the CPI numbers for the month, scheduled to be released next week, on Tuesday.

Wall Street cheers prospect of June Fed pause

The rise in the unemployment rate and the slowdown in wages allowed equity investors to continue increasing their risk exposure, despite Treasury yields climbing north. It seems that the likelihood of a potential pause in June urged investors to add to their positions before a hike prompts them to liquidate, or the fact that they see interest rates being cut to current levels by the end of the year after a potential hike in July does not affect their portfolio assessment.

Following the debt-ceiling resolution that erased fears of an economic destabilization, the stellar NFP gains may have suggested that the economy is performing well at a time when not many more hikes are needed. In other words, fears that the Fed’s tightening could have severely damaged the economy are diminishing.

Nonetheless, the debt-ceiling deal may be acting as a boost pill for now but a potential liquidity squeeze from Treasury issuance may have the opposite effect. With the Nasdaq now nearly 40% up from its October low, the risk of a downside correction in the foreseeable future may be increasing.

RBA policy decision awaited, Saudi Arabia cuts oil output

Back to the FX world, the aussie was among the few currencies that managed to gain ground against the US dollar on Friday, perhaps on the decision of Australia’s Fair Work Commission to raise wages by 5.75%. This confused investors regarding what the RBA will decide at tomorrow’s gathering, with market pricing suggesting that the chances of raising rates are actually the same as of a coin toss.

Therefore, the aussie could gain in the case the RBA pushes the hike button, while it could come under renewed pressure should officials pause and hint that they will base their future decisions on incoming data.

Regarding the energy market, oil prices opened with a large positive gap today, after Saudi Arabia said it will cut production by another 1mn barrels per day (bpd), starting in July. This was a decision on top of a broader OPEC+ consensus to extend the previous cuts into 2024 as the cartel seeks to offer support to prices.

Despite the surprising decision to cut supply back in April, the related gains were short-lived, with prices coming under pressure since then on concerns that the weakness of economic activity in China will weigh on demand.