Tuesday January 17: Five things the markets are talking about

Investor nervousness over U.S President elect Trump’s policies and the U.K.’s position in the E.U has encouraged a move towards safer assets, sending the ‘mighty’ dollar tumbling, while rallies in haven assets, like gold and the yen, have stretched into another trading session. Global sovereign bond yields again have fallen while equity indexes are making a tough go of it.

The markets focus will be on U.K PM Theresa May’s speech in a few hours (06:45 am EST) where she will say that the U.K. is likely to pull out of the E.U’s single market for goods and services and seek a completely new trading relationship with the bloc and will not settle for partial membership in the E.U.

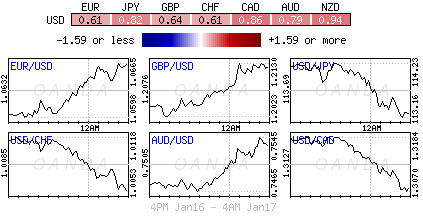

When rumors of PM May’s speech surfaced over the weekend, it pushed the pound to trade atop of its 31-year lows outright, akin to last October’s “flash” crash levels (£1.1987). Sterling since then has made a resounding recovery, gaining another +1% this morning as the market covers ‘short’ positions (£1.2170) on the back of stronger inflation data (see below).

Details from this morning’s speech from PM May are expected to determine the direction of GBP over the coming days and weeks.

1. Equities continue to embrace the negative trade

Asian shares were mixed overnight ahead of this morning’s crucial speech by U.K. Prime Minister Theresa May, with stocks in China reversing early declines in another roller-coaster session.

In China, the Shenzhen Composite Index ended up +1.2%, after dropping as much as -1.5% intraday, while the Shanghai Composite Index edged up +0.2%, reversing from losses of as much as -1%. Despite ending in positive territory, overall sentiment remains weak on the fact that Beijing seems committed to accelerating the approval of new listings.

Note: Analysts believe government-backed funds intervention by Chinese authorities contributed to the aggressive intraday turnaround.

Elsewhere, the Nikkei Stock Average ended down -1.5% on the back of a stronger yen (¥113.17) hurting exporters. The Aussies ASX 200 was off -0.9% while the Singapore’s Straits Times Index fell -0.3%.

In Europe, it’s no surprise to see equities trade lower ahead of PM Theresa May’s speech. Major banking stocks in the Eurostoxx are trading mixed, while commodity and mining stocks are weighing in the FTSE 100 with copper prices continue its sell off.

U.S futures are set to open in the ‘red’ (-0.4%).

Indices: Stoxx50 -0.6% at 3,279, FTSE -0.3% at 7,304, DAX -0.7% at 11,473, CAC 40 -0.5% at 4,857, IBEX 35 -0.1% at 9,401, FTSE MIB +0.2% at 19,276, SMI -0.5% at 8,320, S&P 500 Futures -0.4%

2. Oil prices mixed, investors look to inventories for direction

Oil prices are mixed ahead of the U.S open, supported by the Saudis saying they would adhere to a commitment to cut output, but held back by rising U.S. production and skepticism that OPEC would comply with its commitments to reduce supplies.

Brent futures are at +$55.76 per barrel, down -10c from Monday’s close, while U.S. West Texas Intermediate (WTI) crude futures are up +15c at +$52.51 per barrel.

Note: Under the November agreement, OPEC, Russia, and other non-OPEC producers have pledged to cut oil output by nearly -1.8m bpd, initially for six-months to bring supplies back in line with consumption.

The market continues to eye U.S. output with interest, as this could offset supply cuts elsewhere.

Gold has climbed +0.9% to +$1,212.91 per ounce, extending its winning streak to seven-days, the longest since November 23.

Note: If the market continues to price in three to four Fed rate hikes for this year, it will likely be the crippling factor for gold ‘bulls’, as real yields start to rise, particularly if inflation remains modest.

3. Tweaking allows ECB to move down the curve

The ECB bought a record-breaking €24.7B worth of debt last week, taking advantage of a bumper supply of bank bonds to boost its economic stimulus program.

It’s expected that the new ‘flexibility’ powers given to ECB policy makers will allow them to shift down the Euro curve to the short-end, affecting long-end eurozone government bond yields (30-years at +1.06%). New powers allows authorities to avoid having to buy much more of the 30-year, if there is flexibility on the short-end.

With the ECB tweaking, Germany secured the lowest on record two-year average allotment yield this morning (the terms now allow for buying bonds at yields below the -0.40% deposit rate and for bonds with one-year maturity).

Germany sold €4B December 2018 Schatz (Two-year Treasuries) with an average yield of -0.75% vs. -0.71% December 7. The bid-to-cover was 1.3 vs. 1.8.

Ahead of the U.S open, 10-Year Treasuries have dropped -7bps to +2.33%, after dropping -2bps last week. Treasuries are playing catch up after being closed for Martin Luther King Day.

4. Pound finds support, Trump vocal on Dollar strength

Sterling has extended its overnight gains, rising +1% (£1.2178) outright before this mornings Brexit speech by U.K. Prime Minister Theresa May and after U.K’s inflation data (see below) beat forecasts. Unless they are still surprises to be divulged by PM May, dealers are anticipating a further short squeeze higher for the pound supported by vulnerable ‘short’ positions that have been taken.

Mr. Trump has broken with the convention that U.S Presidents do not comment on the USD – the President-elect said the U.S. dollar was already “too strong” in part because China holds down its currency, the yuan. Knowing the new President-elect, the market can expect more ‘off the cuff’ remarks to move currency prices going forth.

JPY (¥113.14) continues to be supported from risk aversion over the past two-sessions over hard Brexit and potential protectionism by the incoming Trump Administration. The EUR/USD (€1.0685) is higher by +0.7% as the pair sets its sights on the psychological €1.0700 handle.

5. U.K Inflation beats expectations

Data this morning shows that U.K consumer prices grew at the fastest annual rate in over two years in December, driven by the pound’s weakening in the aftermath of the Brexit vote.

U.K annual inflation stood at +1.6% – this was +0.4% above the previous month’s annual inflation rate. Compared to November, prices grew by +0.5%.

Analysts note that the surge in inflation came as companies began to pass on rising input costs linked to a weaker pound onto consumers (costs of materials and fuels used in production rose by +15.8% y/y, the fastest rate of growth in six-years).