Monday November 14: Five things the markets are talking about

New U.S President elect Donald Trump continues to have a massive impact on capital markets.

Global bond markets have lost more than $1 trillion in value; their worst rout in 18-months, on investors bets that Trumps new administration would boost business investments and spending while firing up inflation.

In emerging markets, there is an exodus of capital as speculation builds that the U.S. is heading into an era of rising interest rates and more protectionist trade policies.

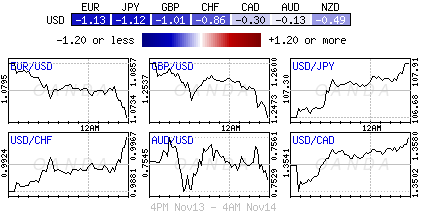

In forex, there have been broad gains for the “mighty” dollar as the market seems content, for the time being, to push aside some of their initial concerns about protectionism, and instead focus on rate differentials.

Is the market getting ahead of itself, or is this the ‘real’ beginning of a shift in market thinking?

1. Global equities divided

Asian equity indexed were mixed overnight, with Japan’s Nikkei outperforming regional markets following stronger-than-expected economic data (Q3 GDP +2.2% vs. +0.9%) and a weaker yen.

The Nikkei Stock Average closed up +1.7%, becoming the region’s biggest outperformer. The Aussies S&P/ASX 200 ended down -0.5%, Singapore’s FTSE Straits Times Index was off -0.9%, and Hong Kong’s Hang Seng Index was down -1.4%.

In Europe, equity indices are trading sharply higher on hope that a Trump victory will boost economic growth. Banking stocks are leading the gains in STOXX 600 while commodity and mining stocks are leading the gains in the FTSE 100.

S&P 500 Index futures are trading +0.4% higher.

Indices: Stoxx50 +1.2% at 3,061, FTSE 100 +1.1% at 6,802, DAX +0.9% at 10,767, CAC 40 +1.2% at 4,545, IBEX 35 +0.6% at 8,694, FTSE MIB +0.4% at 16,886, SMI +0.8% at 7,940, S&P 500 Futures +0.4%

2. Crude stable, industrial metals rally

Crude oil prices continue to hover near their three-month lows on concerns of another year of oversupply. The market is not convinced that OPEC will reach a deal to cut output at its Nov 30 meeting in Vienna.

Brent crude futures are down -2c at +$44.73 a barrel, while light crude futures (WTI) are down -6c at +$43.35 a barrel.

If a lack of agreement is confirmed, the psychological $40 a barrel will come under immediate pressure, on the other hand, if a surprise consensus is agreed upon, crude prices are expected to rally aggressively north of +$50 a barrel.

On Friday, OPEC said its output hit a record +33.64 million barrels per day (bpd) in October, and forecasted an even larger global surplus next year.

Ahead of the U.S open, gold has fallen to a five-month low ($1,224), after sliding last week by the most in three-years as the prospect of a Dec Fed rate hikes is strengthening the ‘mighty’ dollar.

Industrial metals are performing very differently on the back of Trump infrastructure spending possibilities – copper is trading +3.4% higher (last week it surged +11%) while iron ore has climbed to a two-year high. Are the prices moves for metals a tad excessive?

3. Bond rout persists on ‘reflection’

U.S. 10-Year notes backed up +37bps last week, the most in three-years, on traders speculation that Trump’s plans to boost spending and cut taxes will widen the U.S budget deficit and stoke inflation.

Overnight, U.S 10’s have rallied another +8bps to +2.23% supported further by Fed Vice-Chair Fischer comments on Friday stating that the Fed “was close to achieving its goals of maximum employment and price stability.” This type of rhetoric is supporting the case for an interest-rate increase next month. Fed fund futures prices indicate a +84% chance of a Dec rate hike.

It’s not just the states, sovereign debt have extended their losses across the Australasia and Europe, pushing benchmark bond yields higher in Australia, France and Germany.

In emerging markets, the flow of capital out of those countries has yields also spiking – in Thailand, foreign investors pulled a record +$763m from the domestic bond market Friday, while similar-maturity debt in China dropped for a seventh consecutive day, its longest losing streak in three-years.

4. Look to the future

How nervous are forex traders on emerging market currencies?

The non-deliverable-forward market or NDF’s of Asian currencies are a good barometer to gage investor nervousness about the health of Asian pairs.

The forward premium to buy dollars against Asian block currencies is rising, and for some pairs, aggressively so. This is pressurising some traders to hedge against regional forex depreciation and they do this by buying USD.

On Friday, the one-year NDF for IDR has widened by about +2.7%. Elsewhere, the one-year NDF for the MYR has widened about +3.5% and the SGD +1.1% since Trump’s victory last Wednesday morning.

5. Mixed data from Asia

Data overnight showed that China’s fixed assets growth rallied to a new four-month high.

Property sales values were up over +40%, while investment was up about +7%. The industrial output data headline was more mixed, with growth of power generation rising to +8% from +6.8% despite slower headline growth.

In Japan, Q3 GDP was much better than expected, with a six-month high in both q/q and y/y prints – Q +0.5% vs. +0.2%e, Annualized Q +2.2% vs. +0.8%e.

Digging deeper, corporate Capex did not fall for the first time in three-quarters, while consumption resumed its marginal growth of +0.1%, in line with Q2 and better than the markets +0.0% consensus.

BoJ’s Governor Kuroda testified that the central bank is to continue its easy policy with a flexible outlook on whether to ease rates further. The overnight data and a weaker JPY should deter the BoJ for more easing any time soon