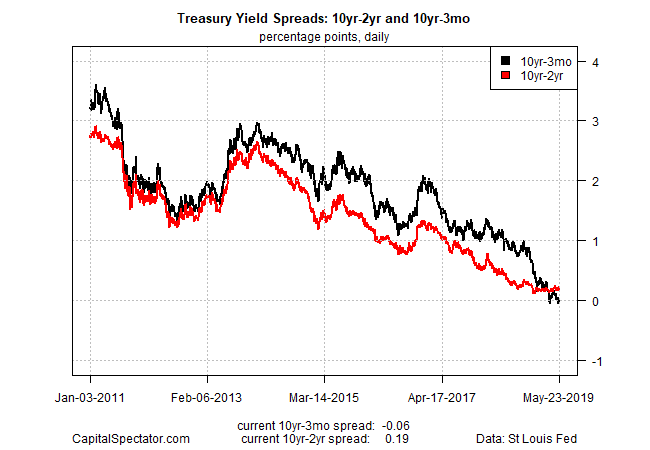

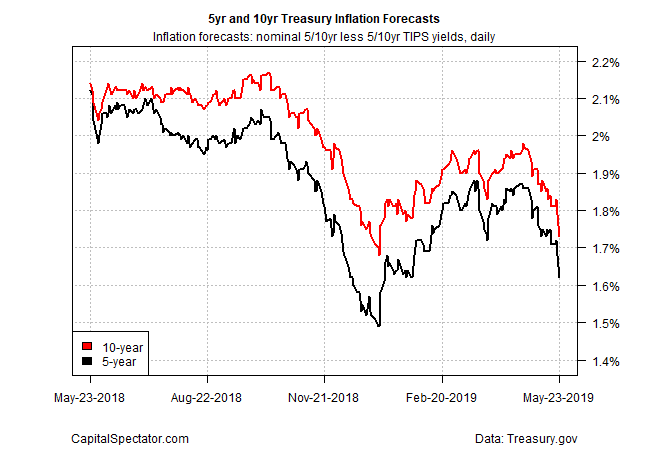

The Treasury market’s outlook has turned grim, based on the inverted yield curve of late. Another dimension of the cautious outlook is yesterday’s sharp drop in the implied inflation outlook, based on yield spreads for nominal less inflation-indexed Treasury rates.

Let’s start with the yield curve, which is inverted for the 10-Year maturity vs. short rates ranging from 3 months up to 1 year.

“The market is obviously telling you that it’s quite worried about some of the incoming data, including the PMIs this morning, the ongoing trade rhetoric and the move in risk assets,” Mark Cabana, who oversees short US rate strategy at Bank of America Merrill Lynch (NYSE:BAC), told CNBC on Thursday. “The concern the market has right now is that we’re moving toward a worst-case scenario, and that could persist for quite some time. If that’s the case, then the market is believing the [weak] economic data, and the Fed will likely need to respond to that by trying to offset and prevent a recession.”

Another analyst reminds that there’s still room for debate on what comes next. Jon Hill, an interest rate strategist at BMO Capital Markets, told the FT that “the strength of the signal increases the deeper and longer the inversion.” He added that “a small move lower is a lot less concerning than 20 or 50 basis points. At the moment, the market is pricing that things will, on average, be flat over the next 10 years.”

Meantime, the Treasury market is repricing the inflation outlook sharply lower these days. For example, the yield spread for 5-year nominal maturity less its inflation-indexed counterpart tumbled to 1.62% yesterday (May 23), based on daily data via Treasury.gov. That’s the lowest level since January and is well below the Fed’s 2.0% inflation target.

The recent slide in inflation expectations is another sign that the crowd is becoming anxious about the economic outlook. If already tame inflation in the official data is set to slide further in the coming months, the deceleration in pricing pressure will be widely interpreted as a warning that economic activity is weakening.

The latest survey of economic expectations via PMI data for the US also paints a cautious outlook. The Composite PMI for May slipped to a three-year low, IHS Markit reports. This index — a proxy for GDP — eased to 50.9. That continues to reflect growth, but just barely as it’s only fractionally above the neutral 50 mark that separates expansion and contraction.

“Growth of business activity slowed sharply in May as trade war worries and increased uncertainty dealt a further blow to order book growth and business Confidence,” advised Chris Williamson, chief business economist at IHS Markit, in a press release. The latest PMI reading implies that US GDP growth is on track to slow to a sluggish 1.2% annualized rate in May. “Worse may be to come, as inflows of new business showed the smallest rise seen this side of the global financial crisis.”

It’s important to keep in mind that market-based projections of economic activity are subject to a high degree of noise. The same can be said of survey data. The acid test in the weeks ahead: Will the hard data in the official numbers confirm the weakening expectations in the Treasury market and PMI figures?

The jury’s still out, in part because the broad set of economic indicators published to date continue to show that recession risk is low and more of the same is likely for the immediate future (for details, see this week’s economic profile update).

Meanwhile, we’re all data dependent, more so than usual. But the economic schedule is light for next week and so the guessing game will continue. The next major reality checks are due on June 5 and June 7, when the May updates will be published for the /ADP Employment Report and the Labor Department’s estimate of payrolls, respectively. Using the recent numbers on initial jobless claims as a guide – a leading indicator that remains solidly bullish – the outlook for the next round of labor market releases appear set to offer optimistic counterpoints to the Treasury market’s gloom.