Investors looking to add healthcare stocks to their portfolio typically buy a pharmaceutical company like Johnson & Johnson (NYSE:JNJ) or Pfizer (NYSE:PFE). But investors can also gain exposure to the healthcare industry indirectly, through Real Estate Investment Trusts that invest in healthcare properties. The beauty of healthcare REITs is that they commonly offer significantly higher dividend yields than pharmaceutical stocks.

For example, Omega Healthcare Investors Inc (NYSE:OHI) is one of the biggest healthcare REITs in the U.S., and it has a 7.7% dividend yield. It has a very high dividend yield, compared with the S&P 500 Index, which has an average dividend yield below 2% right now. Plus, Omega has potential for future growth, thanks to a huge healthcare trend set to unfold over the next several years. This makes Omega an attractive stock for income investors.

Business Overview & Recent Events

Omega Healthcare Investors is a REIT that owns healthcare properties. The company was founded in 1992, and today has a market capitalization above $6 billion. It utilizes long term triple-net leases. The triple-net structure is advantageous for Omega, as it provides fixed rent payments from tenants with annual escalators. And, property level expenses (such as labor, insurance, property taxes, and capital expenditures) are the operator’s responsibility.

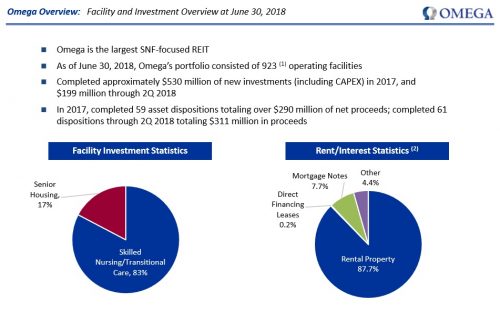

At the end of the third quarter, Omega’s portfolio consisted of 923 healthcare facilities, located in 41 states and the United Kingdom. Its portfolio includes skilled nursing facilities (83% of revenue), senior housing (13% of revenue) as well as a small collection of other properties (4% of revenue).

Source: Investor Presentation, page 4

The past year has been difficult for Omega, due to some problems with two tenants, Orianna and Preferred Care, which entered bankruptcy. Preferred Care was a relatively small tenant with annual contractual revenues of just $3 million, but Orianna was Omega Healthcare’s fifth-largest tenant, with annual contractual revenues of $47 million.

Elevated costs related to the issues facing Orianna and Preferred Care weighed on Omega’s cash flow, but the company is making progress reshaping its portfolio. Omega has transitioned the Mississippi based Orianna facilities and will generate contractual annual rent of $12 million from them. The company reaffirmed it expects $32 to $38 million in annual rent total from these assets once they are transitioned or sold.

Omega’s strong third quarter earnings report showed that the steps taken to improve its property portfolio are having a positive impact. For the quarter, revenue of $222 million increased 1% year-over-year, and beat analyst estimates by $28 million. Funds from operation (FFO) per share of $0.77 also beat by $0.02 per share, and declined 2.5% from the same quarter last year. Higher tenant revenue was more than offset by higher restructuring and interest expenses.

Still, Omega generates more than enough cash flow to reward shareholders with a strong dividend. For 2018, the company expects FFO-per-share in a range of $3.03 to $3.06. Assuming the company reaches its FFO forecast, it will easily cover its $2.64 per share dividend. There could even be room for future dividend increases, as the company is set to grow FFO in the years ahead.

Profiting From The Aging Population

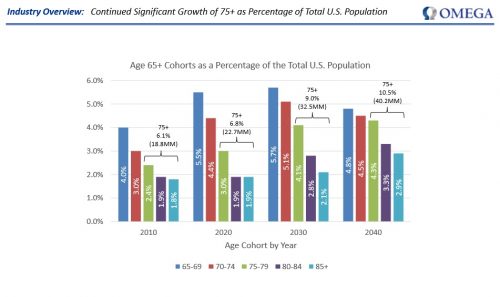

One of the advantages of investing in health care REITs is that the industry has a positive long-term growth outlook. Healthcare REITs like Omega are ideally positioned to capitalize on a major trend: the aging population. Older generations of Americans such as the Baby Boomers are large in size, and growing, relative to other generational groups. To that end, Omega expects the 65+ population to continue growing, as a share of the overall population.

Source: Investor Presentation, page 13

Continued growth of the 65+ cohort means demand for healthcare real estate properties, such as skilled nursing facilities and senior housing facilities, is likely to grow for the foreseeable future. The number of elderly people in need of healthcare is expected to grow at a fast pace over the next decade. In addition, the trend is for the elderly to spend an increasing amount of money on healthcare. Healthcare spending is likely to rise at a faster rate than GDP growth in the United States going forward.

Omega’s portfolio remains in good shape. It will see only a small portion of its leases expire over the next decade. Moreover, it has no material debt maturities until 2022. Therefore, the REIT is likely to enjoy reliable free cash flows in the upcoming years, without any shocks from debt maturities. Omega’s FFO growth could be restrained while the company works through its tenant issues, but the company is well-positioned for the long run.

Omega stock could generate strong returns for shareholders over the next five years, due to FFO growth, a low stock valuation, and dividends. During the last decade, the company grew FFO at a 4.5% average annual rate. As it is likely to complete its asset repositioning this year, it is reasonable to expect the REIT to grow its FFO at a 4.5% average annual rate over the next five years.

In addition, Omega shares appear to be undervalued today. Lingering concerns over its property portfolio caused Omega’s stock valuation to decline in the past year. Now, Omega stock trades for a price-to-FFO ratio of 11.2, compared with a 10-year average ratio of 12.4. This means Omega is valued more cheaply than its long-term historical average, which could signal a buying opportunity. The stock is expected to revert towards its average valuation level, since the company’s turnaround efforts are likely to be successful. If this occurs, the stock will enjoy a 2.1% average annual gain thanks to expansion of the valuation multiple through 2023.

Lastly, dividends are a major component of REIT shareholder returns. In this case, Omega stock pays a current dividend yield of 7.7%. This is a high and appealing dividend for investors searching for yield in a low interest rate environment. Adding it all up, the combination of valuation changes, FFO growth, and dividends cumulatively result in total expected returns of over 14% per year.

Final Thoughts

Stocks with high dividend yields should be approached with caution. It is important for investors to understand the unique risks of high-yield stocks, and make sure the high yield is sustainable. In this case, Omega appears to be a safe high-yield stock, with sufficient cash flow to maintain the dividend payout. And, Omega has positive growth potential for the future, thanks to the aging population and continued need for healthcare real estate. With a 7.7% yield and total expected returns of over 14% per year, Omega is an appealing stock for income investors.