Last week I predicted a market focus on Syria, expecting President Obama's Tuesday evening speech to be the focal point. My concept was correct, but events moved even more swiftly. The market celebrated as the chance of military action diminished.

This week's theme is easy to predict: It is all about the Fed. Will Bernanke lead the Fed to a new direction, reducing the current stimulus?

Throughout the year, and especially since the May FOMC meeting and announcement, financial markets have reflected concerns about a less stimulative policy. It has been a noisy, pundit's paradise, where each and all can claim expertise and chime in. This creates a minefield for investors, so I will highlight the key issues, and some good sources:

- Will the Fed reduce the pace of bond purchases, a change commonly referred to as "tapering" by everyone except the Fed? According to WSJ polling, 2/3 of economists expect a tapering announcement.

- Does a reduction in bond purchases imply a significant actual price effect? Less than expected, according to this good explanation of why from Mark Dow.

- Do financial markets over-estimate the implications of a change in policy? See the results from the recent Survey of Leading Economic Bloggers

- How much of the market impact has been anticipated by interest rate increases over the last three months? Victor Niederhoffer opines that it is already reflected in the market.

- Who will be the next Fed Chair? Given the apparent nominees, does it really matter for the market? The latest word shows opposition from key Democrats to a Summers nomination. Prof. Hamilton explains why most economists favor Yellen. Michael Hirsh of The Atlantic produces The Comprehensive Case Against Larry Summers.

I have some strongly-held opinions on these question, which I'll report in the conclusion. First, let us do our regular update of last week's news and data.

Background on "Weighing the Week Ahead"

There are many good lists of upcoming events. One source I regularly follow is the weekly calendar from Investing.com. For best results you need to select the date range from the calendar displayed on the site. You will be rewarded with a comprehensive list of data and events from all over the world. It takes a little practice, but it is worth it.

In contrast, I highlight a smaller group of events. My theme is an expert guess about what we will be watching on TV and reading in the mainstream media. It is a focus on what I think is important for my trading and client portfolios. Each week I consider the upcoming calendar and the current market, predicting the main theme we should expect. This step is an important part of my trading preparation and planning. It takes more hours than you can imagine.

My record is pretty good. If you review the list of titles it looks like a history of market concerns. Wrong! The thing to note is that I highlighted each topic the week before it grabbed the attention. I find it useful to reflect on the key theme for the week ahead, and I hope you will as well.

This is unlike my other articles where I develop a focused, logical argument with supporting data on a single theme. Here I am simply sharing my conclusions. Sometimes these are topics that I have already written about, and others are on my agenda. I am putting the news in context.

Readers often disagree with my conclusions. Do not be bashful. Join in and comment about what we should expect in the days ahead. This weekly piece emphasizes my opinions about what is really important and how to put the news in context. I have had great success with my approach, but feel free to disagree. That is what makes a market!

Last Week's Data

Each week I break down events into good and bad. Often there is "ugly" and on rare occasion something really good. My working definition of "good" has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially -- no politics.

- It is better than expectations.

This was a good week, despite the mixed economic data. Here are the positive items.

- Agreement for the destruction of Syria's chemical weapons. The "broad and sweeping" deal (see NYT) between the US and Russia also has grudging approval from Syria. I have no illusions that this will be easy. The process of identification, destruction, and inspection will go on for many months with a background of civil war. It meets our working definition of "good" since it is certainly market-friendly.

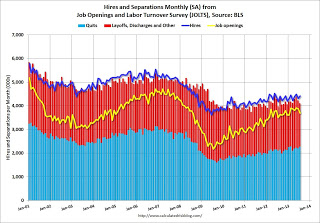

- The "quit rate" is increasing. I was one of the first bloggers to highlight the JOLTS report, which the BLS uses to look beyond the net numbers from the monthly updates. Most people are completely clueless about the churning below the surface. A key element is how many people voluntarily quit their jobs each month. The media would lead most to believe that everyone is desperately clinging to employment. In fact, 2.6 million people were "voluntary separations" last month. This would be a good question to ask pundits in TV interviews. Most could not come within an order of magnitude. As Bill McBride notes, this is best used as a measure of confidence, not net job growth. Here is a good chart from Calculated Risk:

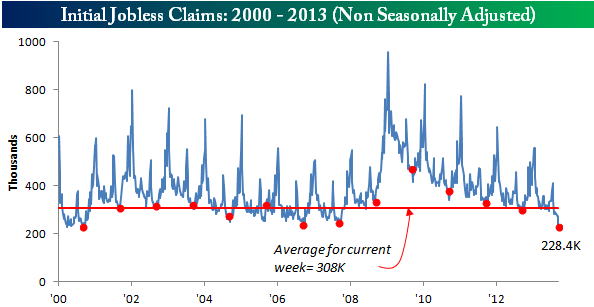

Weekly jobless claims

had a "two handle" although there are issues related to reports from two states. This number could be revised, but for the moment, I'll treat it as "good." Bespoke has a nice post with a package of the charts we love. Here is a sample using the non-seasonally adjusted data:

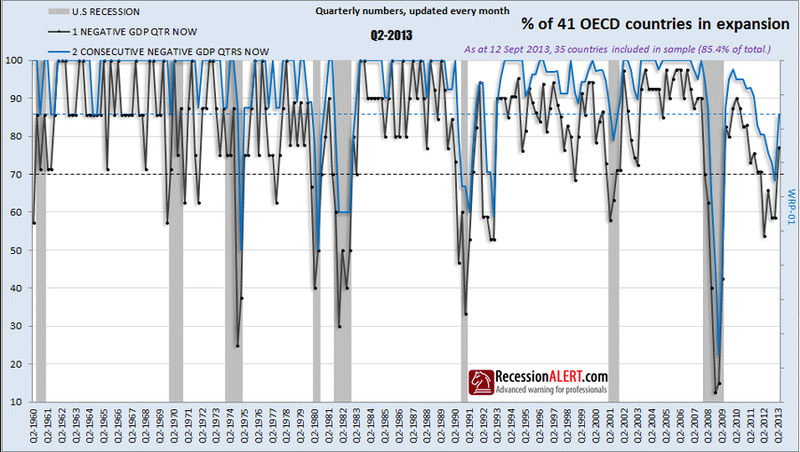

A world economic rebound, now representing over 85% of the countries in RecessionALERT.com's sample. This group of 41 countries represents 97% of the world economy. The chart below shows the solid improvement from the recent near-recession readings. For the full story, including more great charts, read the entire report. (See also Ed Yardeni). (Somewhat contra – Kate McKenzie on Chinese economic growth).

The Bad

Despite the good news on Syria, the economic data were a bit disappointing.

- Retail sales missed expectations. This was a decline and Doug Short plays it straight with a good analysis and his famous charts. Steven Hansen of GEI has a more positive take, pointing to the prior month revisions and year-over-year comparisons. Bespoke leans more toward Hansen, and includes some intriguing tables and charts. The Capital Spectator takes a more balanced view. This is why I read and highlight many sources! If one seems clear to me, that is what I highlight. In this case, you need to read them all to understand the varying interpretations on this key issue.

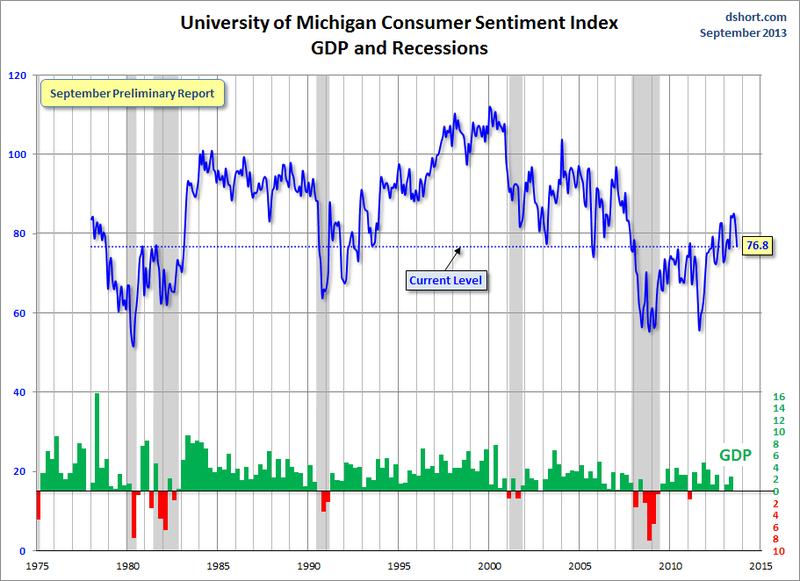

- Michigan consumer sentiment badly missed expectations. This is disappointing, especially in light of recent gains. I see this as a good concurrent indicator of employment and consumer spending, but it is sometimes distorted by politics, gas prices, or world events. The recent preliminary readings have had later upward revisions. While I take each data point at face value, it is possible that this one will get an upward boost from the Syria news and lower oil prices. Here is the impact via my favorite chart. See Doug Short's post for full descriptions and context.

- Five-year financial crisis post-mortem. Neil Irwin of Wonkblog has a "complete list of Wall Street CEO's prosecuted for their role in the financial crisis. There is no way to summarize, so just take a look.

House may cancel September recess

planned for the week of the 23rd. House Majority Leader Cantor says that they may need the time to work on a budget resolution to avoid a government shutdown. (See The Hill).

The Ugly

Attempted scams are prevalent and some of them are working. A FINRA study finds that 84% of respondents had been solicited with at least one type of potentially fraudulent activity. (The other 16% must not have an email account!) Older folks and men are especially susceptible, with 4% admitting to have lost money. FINRA thinks that is under-reported since people do not like to admit embarrassing decisions.

Why are they susceptible? See if you would agree with these offers:

"Forty-three percent of respondents were attracted to "fully guaranteed" investments, 42% found an annual return of 110% for an investment appealing and nearly half liked the prospect of a daily rate of return of over 2%."

Helmets Off!

…to the Colorado football players, staff, and students who helped out those displaced by the terrible flooding. (The game against Fresno will be made up later).

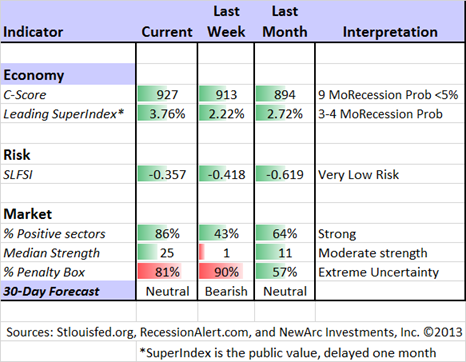

The Indicator Snapshot

It is important to keep the current news in perspective. I am always searching for the best indicators for our weekly snapshot. I make changes when the evidence warrants. At the moment, my weekly snapshot includes these important summary indicators:

- For financial risk, theSt. Louis Financial Stress Index.

- An updated analysis of recession probability from key sources.

- For market trends, the key measures from our "Felix" ETF model.

The SLFSI reports with a one-week lag. This means that the reported values do not include last week's market action. The SLFSI has recently edged a bit higher, reflecting increased market volatility. It remains at historically low levels, well out of the trigger range of my pre-determined risk alarm. This is an excellent tool for managing risk objectively, and it has suggested the need for more caution. Before implementing this indicator our team did extensive research, discovering a "warning range" that deserves respect. We identified a reading of 1.1 or higher as a place to consider reducing positions.

The SLFSI is not a market-timing tool, since it does not attempt to predict how people will interpret events. It uses data, mostly from credit markets, to reach an objective risk assessment. The biggest profits come from going all-in when risk is high on this indicator, but so do the biggest losses.

Recession Odds

I feature the C-Score, a weekly interpretation of the best recession indicator I found, Bob Dieli's "aggregate spread." I have now added a series of videos, where Dr. Dieli explains the rationale for his indicator and how it applied in each recession since the 50's. I have organized this so that you can pick a particular recession and see the discussion for that case. Those who are skeptics about the method should start by reviewing the video for that recession. Anyone who spends some time with this will learn a great deal about the history of recessions from a veteran observer.

I also feature RecessionAlert, which combines a variety of different methods, including the ECRI, in developing a Super Index. They offer a free sample report. Anyone following them over the last year would have had useful and profitable guidance on the economy. RecessionAlert has developed a comprehensive package of economic forecasting and market indicators, well worth your consideration. Dwaine has also developed a market-timing approach which follows ten bear-market signals. His latest installment provides detail and a current look.

Georg Vrba's four-input recession indicator is also benign. "Based on the historic patterns of the unemployment rate indicators prior to recessions one can reasonably conclude that the U.S. economy is not likely to go into recession anytime soon." Georg has other excellent indicators for stocks, bonds, and precious metals at iMarketSignals. For those interested in gold, he has a recent update, asking when there will be a fresh buy signal.

Unfortunately, and despite the inaccuracy of their forecast, the mainstream media features the ECRI. Doug Short has excellent continuing coverage of the ECRI recession prediction, now over 18 months old. Doug updates all of the official indicators used by the NBER and also has a helpful list of articles about recession forecasting. His latest comment points out that the public data series has not been helpful or consistent with the announced ECRI posture. Doug also continues to refresh the best chart update of the major indicators used by the NBER in recession dating.

The average investor has lost track of this long ago, and that is unfortunate. The original ECRI claim and the supporting public data was expensive for many. The reason that I track this weekly, emphasizing the best methods, is that understanding recessions is important for corporate earnings and for stock prices. This attention to actual risk measures has paid off handsomely for anyone our investors, and for anyone reading each week.

Readers might also want to review my Recession Resource Page, which explains many of the concepts people get wrong.

Our "Felix" model is the basis for our "official" vote in the weekly Ticker Sense Blogger Sentiment Poll. We have a long public record for these positions. Last week Felix turned bearish. I wrote, "Felix might switch to a neutral posture if the overall market holds its ground." With the reduced chance of military action against Syria, the market celebrated the reduction in uncertainty. The key change from last week is that the inverse ETFs have dropped dramatically in the ratings. They are now significantly lower than their positive counterparts.

The Ticker Sense poll asks for a one-month forecast. Felix has a three-week horizon, which is pretty close. We run the model daily, and adjust our outlook as needed.

Felix's ratings improved dramatically over the last week, and the penalty box percentage decreased. A high rating means that most ETFs are in the penalty box, so we have less confidence in the overall ratings. That measure remains elevated. Felix is close to bullish territory.

[For more on the penalty box see this article. For more on the system ratings, you can write to etf at newarc dot com for our free report package or to be added to the (free) weekly ETF email list. You can also write personally to me with questions or comments, and I'll do my best to answer.]

The Week Ahead

This week brings little data and scheduled news, an artifact of the calendar and the holidays.

The "A List" includes the following:

- The FOMC decision (W). Followed by the Bernanke press conference.

- Initial jobless claims (Th). Employment is the focal point in evaluating the economy, and this is the most responsive indicator.

- Building permits and housing starts (W). Permits are the best leading indicator, but the market emphasizes housing starts. These are crucial factors in the current rebound since construction activity is implied.

- Industrial production (M). Closely watched component of GDP.

- Existing home sales (Th). An indicator of the housing market, and economic health, but not as important as new homes.

- CPI (T). Inflation is still not a major concern, but eventually it will be important. Meanwhile, we watch closely.

- Leading indicators (Th). Still a favorite for some economic observers, despite some controversy about the index.

I am not very interested in the Philly Fed, although it sometimes moves the market if it makes a major move. I am even less interested in the Empire State index. There will be more speeches and news about Syria, but it will remain in the background unless there is another chemical weapons incident.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a "one size fits all" approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix went wrong last week. World events sparked a dramatic change in sentiment and market direction. Felix correctly identified a dangerous situation, and our trading accounts were poised to profit from a market decline. This type of trading is an appropriate choice for some investors, often as a complement to their regular long holdings in stocks.

When such a prediction goes wrong, most people forget that risk was avoided or hedged. When the fire does not happen, why did we have insurance?

This is why I emphasize each week the short-term nature of the trading program.

Felix frequently identifies concepts recommended by the leading experts. Jim Grant was on CNBC Friday afternoon, recommending that you buy assorted Russian energy stocks on the London exchange. He noted the risks and extolled the valuation, responding to Maria's questions. For those who do not have an account that readily works for London, you could follow our ETF updates. We show an easy way to accomplish the same thing. I posted as follows on WSAS:

"If anyone is interested in Russian energy, the Market Vectors Russia ETF (RSX) has all of the names Grant mentioned in pretty high concentration. I trade it occasionally via Felix, and it is highly correlated with oil. It is top-ranked Felix ETF at the moment, but in the penalty box."

We do not yet own RSX, but we might buy it soon. During the week we sold our holdings in the inverse ETFs, accepting a modest loss on our 2/3 position. Trading accounts are now completely out of the market, but there are several attractive sectors. My guess is that Felix will have fresh buys for us in a couple of days.

Insight for Investors

One of the most frequent questions for me is why I separate the time frames in these posts. I frequently suggest that investors use periods of selling to add to positions. At the same time, traders might be taking short positions. Those following the enhanced yield approach should be adding new covered call positions on dips, and selling calls against existing stock positions on rallies.

It is all about the time frame!

The challenge for investors is to distinguish between the major trends and the short-term uncertainty. The main themes are not related to headlines news, even though sentiment may drive market fluctuations. Do not be seduced by the idea that you can time the market, calling every 10% correction. Many claim this ability, but few have a documented record to prove it. Most who claim past success are using a back-tested model. (See here)

Take last week as an example. Few traders can be sufficiently agile to make major position adjustments. Even if they try, the news – always difficult to interpret – can throw a curve ball. It is much better to discover a winning method and stick with it.

Here are the most important current themes.

- Beware of yield plays. For several months, I have accurately emphasized the danger of yield-based investments – yesterday's source of safety. The popular name for this is "The Great Rotation." It is still in the early innings, since bond fund investors are only getting the bad news from their statements. Even the best bond managers (like Gross and Gundlach) cannot win when interest rates are rising. The exodus from their funds is continuing. Most investors are emphasizing cash, real estate, and gold. .333 is good in the major leagues, but not for your investments!

It may be a "generational selling opportunity" for bonds. I locked in some positions after the recent big move, but this story is not over. There is a continuing move to cyclical stocks (which I currently favor). - Find a safer source of yield: Take what the market is giving you!

For the conservative investor, you can buy stocks with a reasonable yield, attractive valuation, and a strong balance sheet. You can then sell near-term calls against your position and target returns close to 10%. The risk is far lower than for a general stock portfolio. This strategy has worked well for over two years and continues to do so. (I freely share how we do it and you can try it yourself. Follow here).

Two weeks ago you had chances to set new positions on down days and also to sell calls against existing energy positions on the Syria news. This week we cashed in on the rally from the Intel developers' forum (which we have been discussing at Wall Street All Stars). By holding the stock from the last expiration and waiting to sell calls (I did the OCT 24's for clients). Take what is offered each day. - Avoid the paralysis from fear! Many are rewarded for making sure that you are "scared witless" (TM OldProf euphemism). If you are addicted to gold and allegedly safe yield stocks, you need a checkup. Gold works in times of hyperinflation or deflation/crisis. When neither happens, the ball is going between these Golden Goalposts. I have a good transition plan for those with a fixation and fear and gold.

- Become an Insightful Investor! My current series about the eight traits of the insightful investor will help to point the way. The most recent installment shows a chart that has been expensive for many. The chart has gotten about a zillion page views. My reply is known only to a group equivalent to the population of a small town. Astute investors take advantage of disparities like this!

And finally, we have collected some of our recent recommendations in a new investor resource page -- a starting point for the long-term investor. (Comments and suggestions welcome. I am trying to be helpful and I love feedback).

Final Thought

I suggest several key conclusions from recent data. Each is important, and collectively they provide a good foundation for long-term investors.

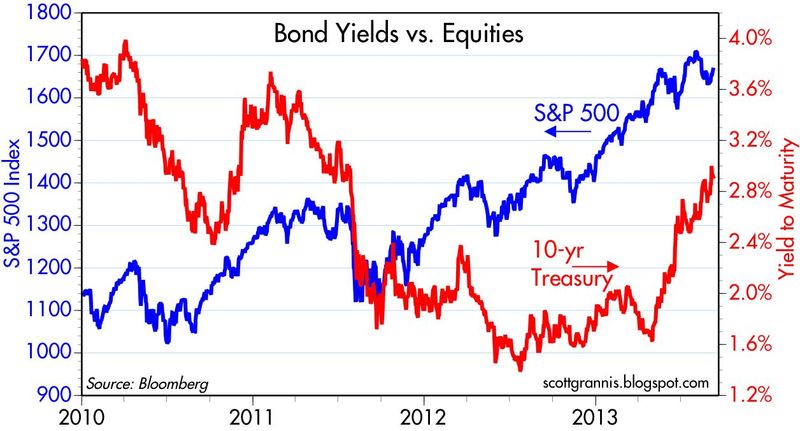

- Many failed pundits excuse themselves by pointing to the Fed. (See The Fed as a Fig Leaf). In fact, the Fed policy has had a positive but small impact. Stocks have done well in spite of an increase in interest rates. Scott Grannis sees the rise in yields as reflective of the economy – a failure of QE. His chart shows that dramatic "non-correlation."

- The Fed will probably announce a policy change. This reflects a shift in the center of FOMC opinion – more confidence in the economy, more concern about unpredictable side-effects, and more emphasis on a shift to forward guidance.

- The Fed policy will remain stimulative for about two more years. Despite this, expect another round of the debate about whether easing up on the gas pedal is the same as hitting the brake.

- The "taper equals tightening" camp is wrong on the facts, but enjoys a large audience.

- Some claim that the first Fed move is immediately projected to the final result, because markets anticipate.

- I recommend attention to the actual facts. Those who have been wrong for the last several years will be wrong again.

- There will be some negative market reaction. Not everyone expects a change, and some do not agree that it is mostly anticipated. This means there will be sellers. I expect this to be relatively modest and short-lived, given the multi-month build up.

- The Bernanke press conference will be important. I have not been a fan of the press conferences. They seem helpful, but it has not been a good venue for explanations by this particular Fed Chair. The press conference could lead to some stock market weakness, which I expect to be temporary.

It always helps to start the week with a plan. An old military maxim says that "no plan survives the first shot." It still helps you to prepare and to react quickly.