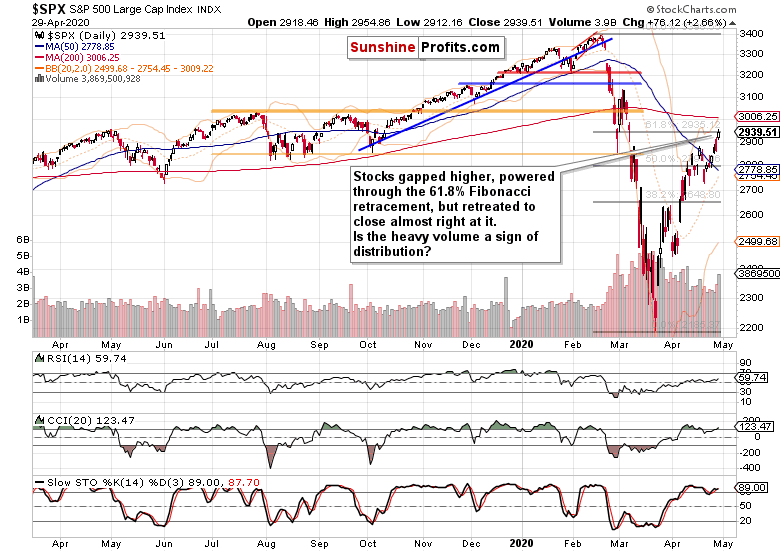

Already at yesterday’s open, stocks have erased Tuesday’s downswing – and as the day progressed, more gains came in. The S&P 500 finished at our initial upside target, at the 61.8% Fibonacci retracement. As the Fed press conference got underway, stocks attempted to break above this key resistance, but sold off in the final 15 minutes of the trading session. What comes most likely next?

Let’s check yesterday’s developments on the daily chart (charts courtesy of (http://stockcharts.com ).

S&P 500 in the Short-Run

Yesterday’s candle shows the battle between the bulls and bears. The candle’s shape is bullish by itself, because the upper knot isn’t exactly dwarfing the white body. Therefore, the higher volume of yesterday’s upswing can be chalked down to meeting a serious technical obstacle rather than experiencing heavy selling into strength.

Please note that earlier in April, we’ve seen higher volume too, and stocks still made it above the key resistance (the 50% Fibonacci retracement) back then. The daily chart examination right now leans in favor of upcoming consolidation that will be followed by renewed upswing taking on the upper border of the early March bearish gap.

Let’s explore the clues that favor exactly this outcome.

The Credit Markets’ Point of View

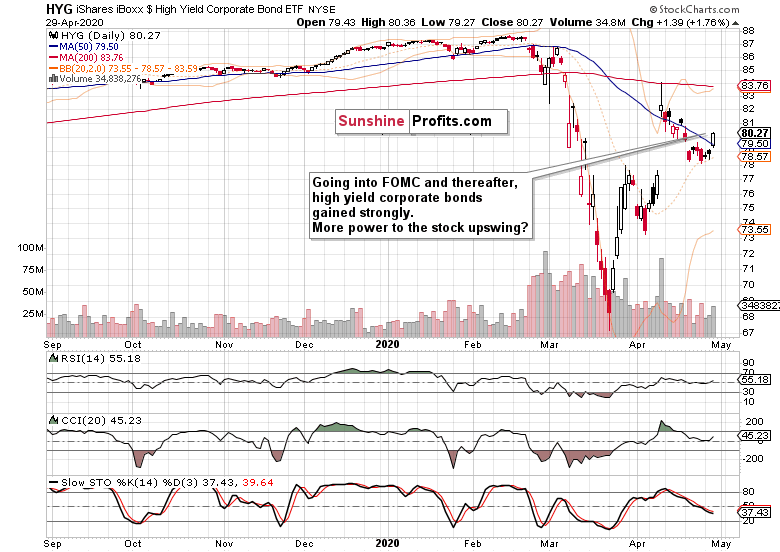

We’ll open this section with the high yield corporate bonds HYG ETF (NYSE:HYG) ETF) analysis.

It’s not just yesterday’s strong showing of corporate junk bonds, their ratio to short-term Treasuries (SHY ETF) performed similarly well. Primed for more gains, they are not alone in this position.

The investment grade corporate bonds to longer-dated Treasuries ratio (LQD:IEI) also moved to the upside yesterday, and appears ready to break higher out of its bullish flag. This is true despite both LQD ETF lagging behind the HYG ETF yesterday, and the weaker showing of municipals (HYD ETF).

Key S&P 500 Sectors in Focus

Technology continues to lead higher, erasing Tuesday’s setback in one go. Whether you look at Alphabet stocks Alphabet Class A (NASDAQ:GOOGL) or Class C (NASDAQ:GOOG), it’s predictably been a star

performer of yesterday’s session. Microsoft (NASDAQ:MSFT) and Facebook (NASDAQ:FB) results also show that big tech can make it through the storm. How strong will Amazon (NASDAQ:AMZN) earnings be when it reports today after the market close? In our opinion, the stock will push higher, confirming our bullish bias for the tech sector.

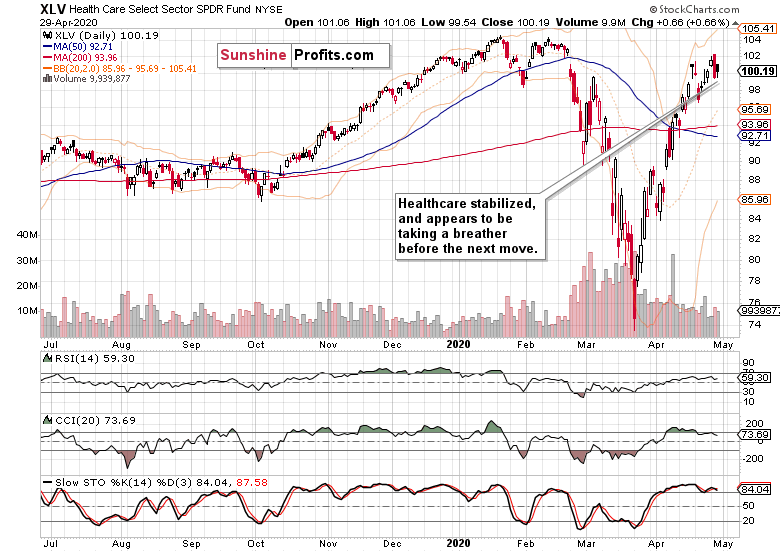

Healthcare (NYSE:HTA) recovered part of the lost ground, and appears to be in need of more time to consolidate before continuing higher. The volume of last two sessions is definitely more consistent with consolidation in the sector than with distribution. But where would the engine of upcoming S&P 500 gains be? Energy (NYSE:XLE), Materials (NYSE:XLB) and Industrial (NYSE:XLI) have led the charge yesterday, too.

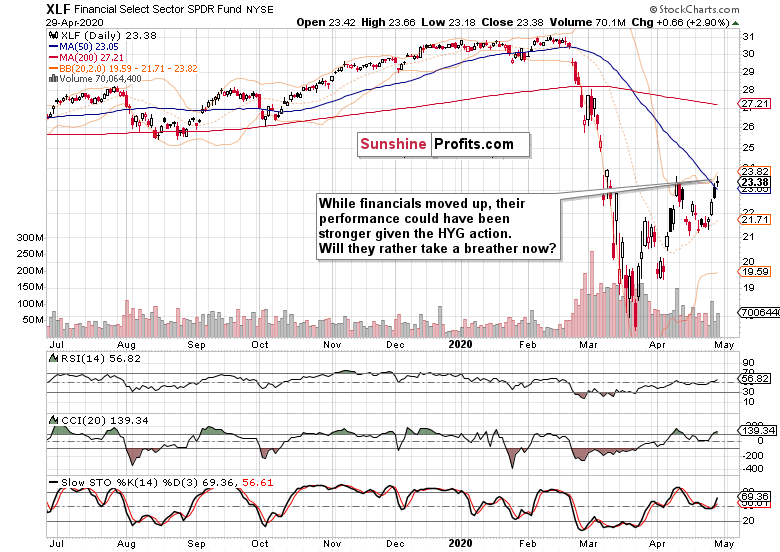

Consumer discretionaries (NYSE:XLY) ETF have also smartly dealt with Tuesday’s setback, similarly to financials (NYSE:XLF) ETF.

Given the strong performance in the credit markets, financials a bit surprisingly paused yesterday. It appears likely that similarly to healthcare, this sector needs to digest recent gains before the next move. And chances are, that the move would be higher when it arrives.

The Fundamental S&P 500 Outlook

Yesterday’s Fed meeting is over, and the not-so-subtle Fed hints that we won’t run out of money are there. So far, so good – the implicit Jerome Powell put is in. Despite today’s premarket downswing (futures trade at around 2910 currently) stocks don’t appear ready to test the resolve in what might very well turn out to be a bear trap.

Yes, weekly unemployment claims are just in, at almost 3.85 million – disappointing expectations. The economy reopening is a long process (state-by-state different) and isn’t likely to bring a V-shaped consumer rebound on a lasting basis. But stocks are forward-looking, ready to bridge the view of more than one quarter ahead.

We’ll monitor the anatomy of both the up and down days for signs that this upleg is over. Right now, that still doesn’t appear to be the case.

Summary

Summing up, S&P 500 challenged the 61.8% Fibonacci retracement yesterday, and today’s premarket trading shows that it won’t be that easily overcome. But the index still remains primed for further gains, and the credit markets keep on providing tailwinds. Powered by positive earnings reports, the tech sector looks far from having topped. While healthcare and financials are likely to consolidate, the stealth bull market trio (energy, materials and industrials) continues to perform. And so do consumer discretionaries. As the bulls’ resolve get tested and stocks digest recent gains, the balance of risks still remains skewed to the upside and our long position justified.