Inflation vs recession

It’s been a troublesome year for equity markets. An overload of government spending during the pandemic coupled with supply disruptions and a global energy crisis joined forces to generate the greatest inflation shock in decades, forcing central banks to raise interest rates at a stunning pace.

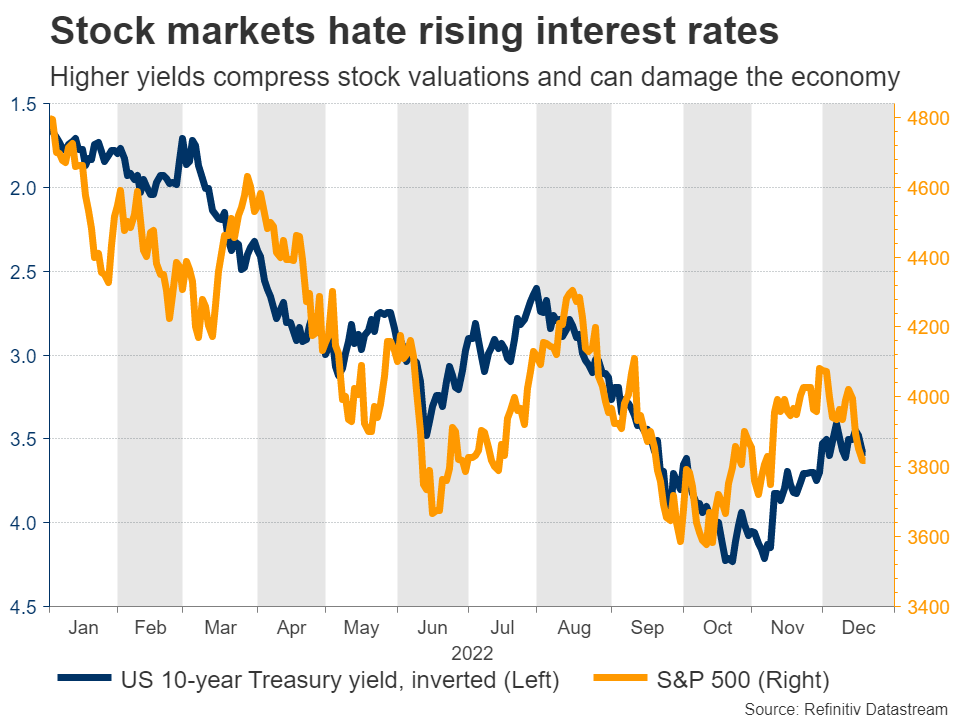

Higher interest rates are toxic for riskier assets like stocks, because they can compress valuation multiples and also inflict damage on the economy itself, dealing a blow to corporate earnings power. Some of the valuation adjustment has already played out, with the S&P 500 earnings multiple falling sharply this year.

However, the earnings impact hasn’t, and it could be the story of next year. By raising interest rates so fast and draining liquidity out of the system, the Federal Reserve is trying to engineer a slowdown in the economy, on the hope that this will reduce demand enough to crush inflation. In doing so, there’s a clear risk it causes a recession.

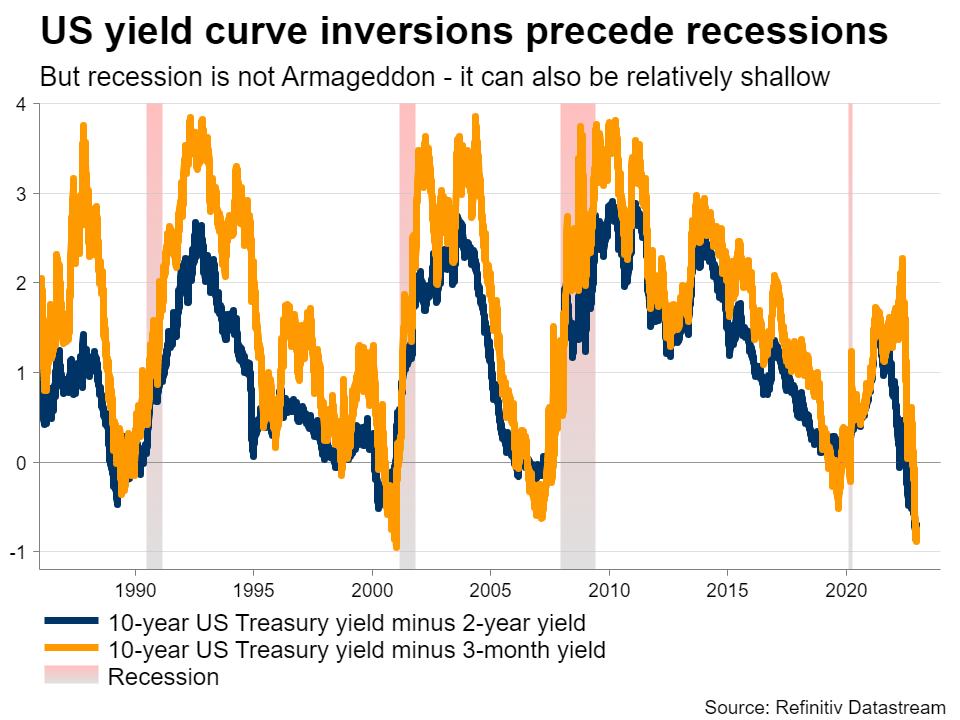

In fact, many classic recessionary indicators are already flashing red. New business orders are on the decline, the housing market has started to crack, consumer morale is low, and retailers are swimming in excess inventory they cannot unload. Meanwhile, the inversion of the US yield curve keeps getting more extreme, which is usually a sign of trouble ahead.

Therefore, while the US economy is still doing fine today, the forward-looking measures suggest “recession” will likely replace “inflation” as the scare word of 2023.

Dissecting valuations and liquidity

The core problem for the US market is that valuations are still too optimistic, not reflecting the risk of a decline in earnings, which the leading indicators are warning about. Hence, the stock market is essentially pricing in a soft economic landing and a rapid decline in inflation.

That’s going to be difficult to pull off. We only have three instances over the last century where the US economy dodged a recession after interest rates rose so sharply, and only one of those is similar to today - the 1994 experience. It can happen, but historically speaking, it’s rare.

The economic weakness in Europe and China because of their respective energy and property crises is further adding credence to such concerns. Companies in the S&P 500 receive around 40% of their revenue from overseas, increasing to almost 60% for the tech sector, so the global landscape is really important.

It’s tough to be optimistic when the S&P 500 is trading at a forward earnings multiple of 17.5x, on earnings that are vulnerable to negative revisions. Such multiples were normal over the last decade when low interest rates artificially boosted valuations, but seem unreasonable today. Most bear markets conclude with a multiple of 14x or below, so there’s scope for valuations to compress further.

Liquidity is another issue. The Fed is draining liquidity out of the market through its quantitative tightening program, and the last time we tried this back in 2018, it ended with a stock market crash. But in recent months, this process was nullified by the US Treasury, which decreased its cash buffer, essentially releasing liquidity back into the system.

This enabled the relief rally in US markets since October, yet it’s a temporary effect that will likely fade in 2023 as the government rebuilds or at least stabilizes its cash levels. With the European Central Bank also announcing plans to begin quantitative tightening next year, the global liquidity impulse is about to deteriorate further.

Increasing odds of recession in Europe

The Euro area and the UK are more likely than the US to dip into a recession as the lethal combination of high inflation and monetary tightening might continue to curtail consumers’ disposable incomes, while Europe’s energy supply throughout the winter remains uncertain.

In contrast to the US, inflationary pressures in Europe stem mostly from the supply side, making monetary policy interventions less effective. In the adverse scenario of an escalation in Ukraine or a tough winter in Europe, governments could impose power rationing, which might deepen any economic downturn.

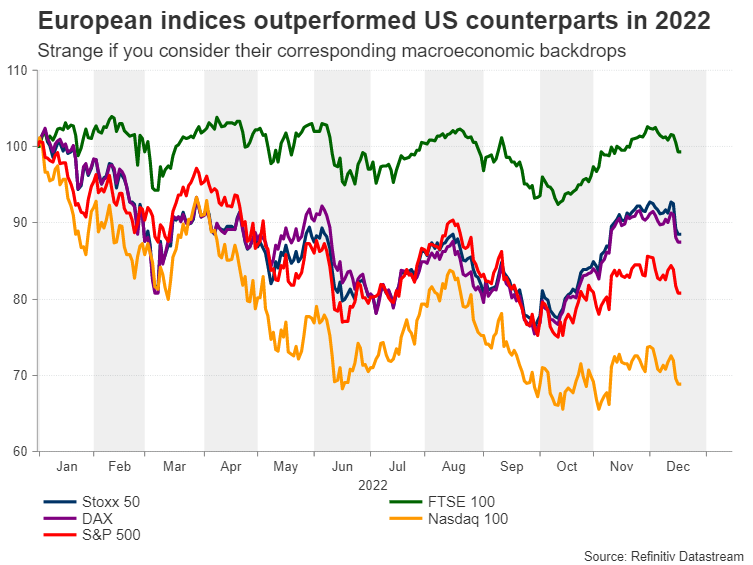

Despite deteriorating macroeconomic conditions and greater uncertainty, major European indices have outperformed their US counterparts in 2022 and have posted a moderate recovery in the fourth quarter. However, this year-end rally could set the stage for a significant pullback next year as growth in Europe will likely remain suppressed by increasingly restrictive interest rates, because inflation remains far too high.

European valuations are cheaper

The current stock market landscape has some similarities with the global financial crisis. In 2008, equity valuations bottomed in November before rallying without any clear catalyst until February 2009 when the negative earnings revisions shuttered investor sentiment and dragged stocks to new lows.

This time around, European indices could hit a trough when forward earnings estimates are downgraded to reflect a recessionary environment, which could be more severe than what their US competitors will face.

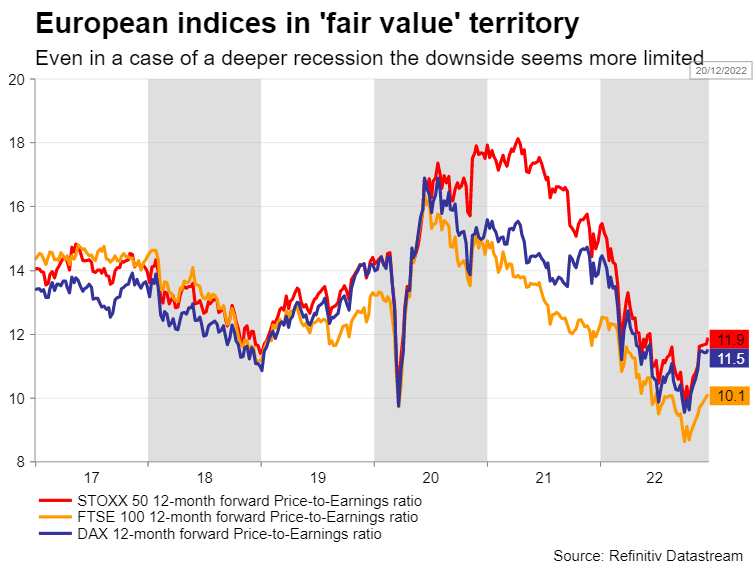

Interestingly, even though US valuations remain significantly higher compared to previous market bottoms, European equity markets are currently trading closer to their ‘fair value’, making their downside potential seem more limited and offering an attractive entry point in case of another selloff.

Tighter financial conditions

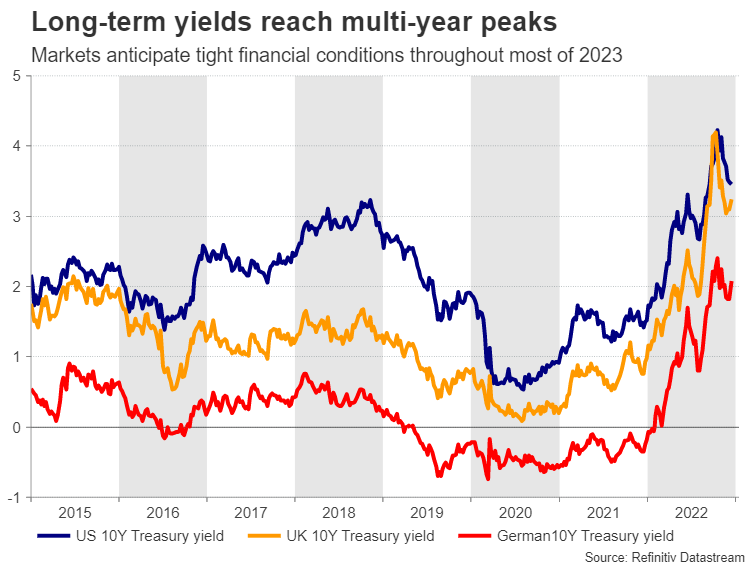

The world’s biggest central banks have stated that their aim is to tighten monetary conditions and keep them restrictive for as long as it takes to restore price stability. The difference between the Fed and the ECB/BoE is that US inflation has already started to cool, leaving the tight labor market as the Fed’s main concern. In Europe, central banks must also cope with the fragile energy situation, which is beyond their control.

Hence, the main risks for European equities are a cold freeze that reawakens the energy crisis and the ECB being overly restrictive, with the quantitative tightening that is set to begin in March posing an additional threat for risky assets.

From a sector perspective, cyclical and growth stocks might take the hardest hit from a combination of high interest rates and substantial earnings downgrades, as a recession will likely impact discretionary sectors more.

Darkest before the dawn

Taking a step back, it’s important to keep things in perspective. The global economy is clearly losing steam and by most metrics, a recession will be difficult to avoid. But the real question for equity markets is the severity of any recession - how long and how deep it will be.

The good news is this one could be relatively brief and shallow, at least in the US. That’s because the weakness is being driven mainly by policy decisions, not some external shock or a failing banking system like in 2008.

If the Fed is essentially engineering an economic slowdown to crush inflation, it can also turn the ship around once the job is done or the pain becomes too much. Hence, even in case of a recession, it might not be a catastrophe for markets.

Since the Great Depression, the average bear market drawdown in the S&P 500 has been around 33%, which would give a ‘target’ near 3,200 in the index. Even if earnings estimates hold up, this region could be reached simply through a valuation compression that brings the forward multiple closer to 14x.

Stock markets can - and usually will - overshoot. Nonetheless, as we approach this region, which is also important from a chart perspective, the risk-to-reward profile would become much more attractive. That’s when investors with long time horizons might look to raise their exposure and take advantage of any bargains.

The bottom line is that every crisis eventually passes. While stocks could resume their selloff as valuations and earnings estimates adjust to tighter liquidity conditions and a softer global economy, getting too bearish can also be a costly mistake.

Historically speaking, stocks bottom a few months before the real economy does, so paradoxically, the best time to enter the market is when the economy is at its worst. Even in the financial world, it is darkest just before dawn.