We’ve got a busy calendar today in Europe and North America, with a Riksbank meeting, Bank of Canada meeting and UK BoE minutes up today. Is GBP/USD ready to sell-off yet?

The market tried to regain an even keel yesterday after the remarkable Friday/Monday meltdown that saw commodity currencies on the defensive. Those currencies bounced, but much like gold and oil, the bounce is so far technical in nature and is still very much in the shadow of the huge sell-off, with the open question of whether downside momentum heats up again.

EUR/USD blasted higher through obvious technical resistance on nary a development save for the generally risk-willing atmosphere yesterday. One suspects stale Euro shorts versus commodity currencies are behind some of the Euro buying and stops were likely lined up all over the obviously important 1.3150-75 area (moving averages). As my long-time readers know, I’m skeptical of this rally, but it would be nice to see a technical hook here that would allow the bears to gain some confidence. To get that from here, we need for the pair to droop back through perhaps 1.3100, or an attempt through 1.3200 to see a high-momentum rejection. Until then, the bears will have to bide their time and wait for a sign. If this rally plays out to its full “potential” to the 0.618 retracement area, the top won’t come until we’ve had a look at closer to the 1.3350 area.

Yesterday’s U.S. March housing starts data grabbed headlines with a new post-Lehman high rate of building, but the leading NAHB survey has been declining for three months in a row and the Building Permits Data disappointed and hasn’t really gone anywhere for at least 6 months. Much of the strength in U.S. housing is a product of “the reach for yield” as deep-pocketed investors are snapping up properties for renting. In short: housing may not act as a drag on the U.S. economy, but it’s not going to offer a strong boost any time soon.

Looking Ahead

The Riksbank meeting is on top of us as I write this – there are no real expectations around this meeting, and Swedish data has been generally supportive of late, save for a downright shockingly bad March Services PMI. The RIksbank has a bit of room for cutting with its 1.00% policy rate and I would suspect that SEK will tend to trade pro-cyclically for a while from here (falling if risk appetite is off, etc…). The Riksbank is one of the banks that forecasts what the rate policy will be – a futile task given where they are versus previous projections, but it gives something for the market to react to. In general, I think SEK is near or at the top of its longer term potential strength.

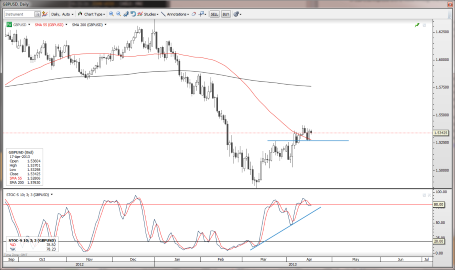

In the UK, we’ve got the BoE minutes up this morning. The market will be looking for signs that the BoE will be more likely to make at least a token further round of asset purchases ahead of the arrival of Carney this summer, but may not get much to go on. The market may be more likely to react strongly to the Retail Sales data tomorrow. I’m looking for a weaker GBP – particularly against the USD, and while the minutes may not provide any spark for heavy selling, I’m not sure that there will be much fuel for GBP upside as the latter has probably mostly been about squeezing shorts, and the weakest hands may be out of the market. Still, we’re in a bit of a technical limbo here and the prospects for a bigger sell-off in GBP/USD improve with a move through the 1.5270/50 area.

GBP/USD

The near term outlook shows that we’re in a range until either the 1.5415 highs or the bottom of the range and the old highs in the 1.5250/70 area give way. Looking eventually for a downside resolution here after we’ve had a good three wave correction, with the admitted risk that the second wave could extend a bit before we sell-off again. GBP/USD" title="GBP/USD" width="455" height="270">

GBP/USD" title="GBP/USD" width="455" height="270">

The Bank of Canada will meet today and the market will hang on its every word. The rally in USD/CAD has perked up again due to the moves in commodity markets, which will likely continue to dominate the outlook from here, but a few more dovish words from the BoC after it downshifted its rhetoric dramatically at the February meeting could see the upside levels above 1.0300 challenged. The longer term question is when/if we ever get out of the seemingly permanent range in USD/CAD below 1.0500/6 and one should note that one-year USD/CAD volatility continues, for obvious reasons to trade at multi-year lows – patient traders might consider long volatility positions.

We’ve got the G-20 up tomorrow and several sources seem to be downplaying expectations that there will be much focus on Japan’s monetary policy. The latest to play this tune was a “senior Canadian official”. But other article suggest that monetary policy will be very much on the agenda, including this basic Reuters preview of the meeting and the official line from the IMF, etc.

In Japan tonight, we have the latest trade data. Interesting to note that Japan’s consumer confidence dipped in March – will it spring back with the April survey due to Kuroda’s Big Move? Anecdotal reports suggest that the Japanese are very cautious in believing the BoJ will succeed.

Stay careful out there – yesterday saw things calming considerably, but the previous volatility could see aftershocks or worse in the days to come.

Economic Data Highlights

- New Zealand Q1 Consumer Prices out at +0.4% QoQ and +0.9% YoY vs. +0.5%/+0.9% expected, respectively and vs. +0.9% YoY in Q4

- Japan Mar. Consumer Confidence out at 44.8 vs. 46.0 expected and 44.2 in Feb.

- Sweden Riksbank Interest Rate Announcement (0730)

- UK BoE Releases Meeting Minutes (0830)

- UK Mar. Jobless Claims Change (0830)

- UK BoE’s Bailey to Speak (0840)

- Euro Zone Feb. Construction Output (0900)

- Sweden Riksbank’s Ingves to hold press conference (0900)

- Canada Mar. Teranet/National Bank Home Price Index (1300)

- US Fed’s Bullard to Speak (1330)

- Canada Bank of Canada Rate Decision (1400)

- Canada BoC Monetary Policy Report (1400)

- US Weekly DoE Crude Oil and Product Inventories (1430)

- Sweden Riksbank’s Jansson to Speak (1500)

- US Fed’s Rosengren to Speak (1600)

- US Fed’s Beige Book (1800)

- Japan Mar. Merchandise Trade Balance (2350)

- New Zealand Apr. ANZ Consumer Confidence (0100)

- Japan BoJ’s Miyao to Speak (0130)

- Japan Mar. Nationwide Department Store Sales (0530)