Risk appetite softened on Tuesday and during the Asian session Wednesday, perhaps due to coronavirus infections accelerating again, and/or due to the softer-than-expected US retail sales for October. In the FX world, the pound was among the main G10 gainers, being bought on expectations that a trade deal with the EU could be reached as soon as next week.

EQUITIES PULL BACK AFTER VACCINE RALLY, GBP GAINS ON DEAL OPTIMISM

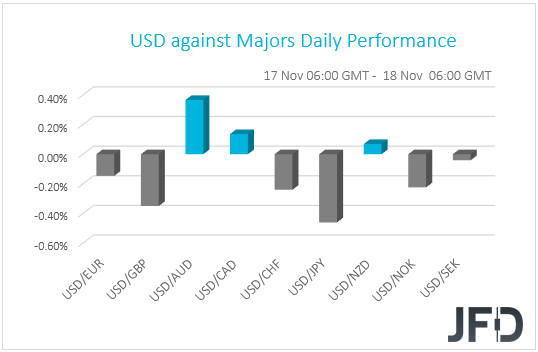

The US dollar traded lower against the majority of the other G10 currencies on Tuesday and during the Asian session Wednesday. It gained only versus AUD, CAD, and NZD in that order, while it underperformed the most against JPY, GBP and CHF.

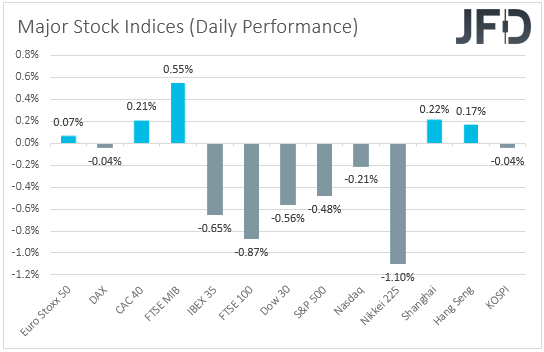

Although the greenback was mostly lower, the strengthening of the yen and franc, and the weakening of the commodity-linked Aussie, Loonie, and Kiwi, suggest that markets turned risk-off at some point yesterday. Looking at the performance in the equity world, we see that EU stock indices were mixed yesterday, while the US ones finished in the red, losing on average 0.42% each. As for today, in Asia, even though China’s Shanghai Composite is up 0.22%, Japan’s Nikkei 225 tumbled 1.10%.

Following the latest rally on promising vaccine trials, investors decided to abandon risk-linked assets, perhaps due to coronavirus infections accelerating again yesterday, and/or due to the softer-than-expected US retail sales for October, which highlighted the lack of new fiscal aid in the US.

In any case, we will maintain a positive view with regards to the broader market appetite, and we will treat yesterday’s retreat as a corrective pullback. After the vaccine-driven rally, a small corrective setback due to some profit-taking appears more than normal to us. Yes, the covid-era is not behind us yet, and thus, more months of restrictions and economic slowdown are ahead until any vaccine is ready for distribution. However, as we noted several times in the last few days, we are now closer in finding the cure, and anything suggesting more progress may continue to support sentiment.

Now back to the currencies, the British pound was the second winner in line, coming under strong buying interest following the news that UK’s Brexit chief negotiator David Frost told Prime

Minister Johnson to expect a trade deal with the EU “early next week”. This followed news last week that Dominic Cummings was set to leave the government, something that according to market chatter increases the chances for an accord as Cummings was seen as a hardline Brexiteer.

Remember that recently we’ve been highlighting that the British currency is likely to stay mostly linked to developments surrounding the Brexit landscape and all this adds credence to our view. Therefore, we will stick to our guns that anything pointing towards an accord may prove supportive for the pound, while the opposite may be true if news suggests that the two sides are finding it difficult to reach common ground. In case we get more optimistic headlines regarding a deal, and conditional upon risk-on returning into the markets, the pound is likely to perform better against the safe havens, the likes of the US dollar, the Japanese yen, and the Swiss franc.

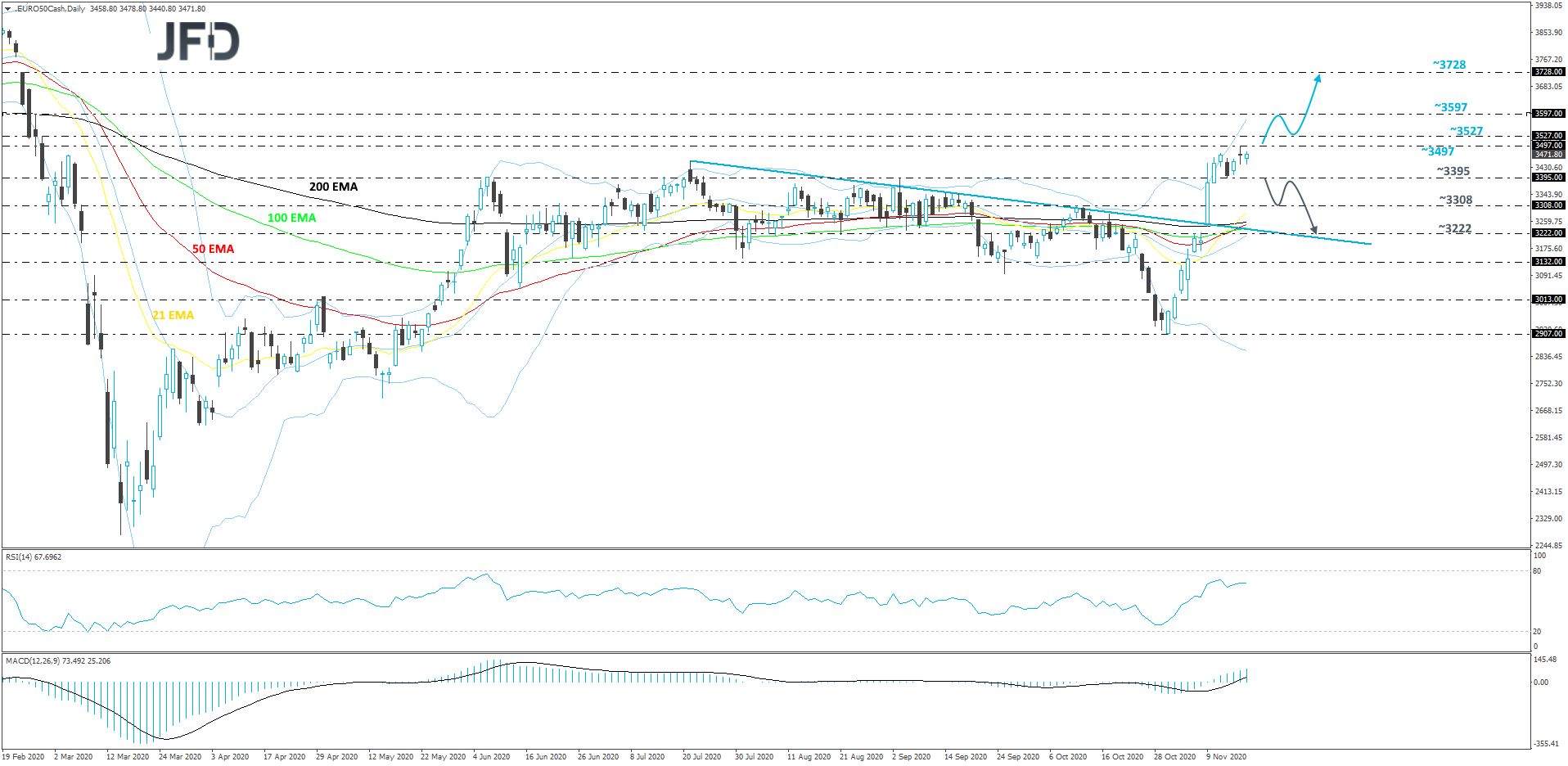

EURO STOXX 50 – TECHNICAL OUTLOOK

After a good run to the upside during the whole course of last week, this week is a more modest one for Euro Stoxx 50, as it is seen to be in some consolidation, at the moment. Some might view it as a possible bullish flag with a slight tilt to the upside. Although all this looks quite positive, we would still prefer to wait for a push above the current high of this week first, which is at 3497.

A strong move above the aforementioned 3497 barrier, would confirm a forthcoming higher high and may clear the way to the some higher areas. That’s when the index might travel to the 3527 obstacle, a break of which could clear the way to the 3597 zone, marked by the lowest point of December of 2019 and the high of February 26th. The index may get halted there temporarily, or even correct slightly lower. However, if Euro Stoxx 50 remains somewhere above the 3497 hurdle, we might see another attempt by the buyers to lift the index. If they succeed in doing that and then are able to overcome the 3597 area, the next potential target could be at 3728, marked by the high of February 24th.

Alternatively, if the price drops below the low of November 12th, at 3395, that could clear the way for a larger correction lower. The index may then drift to the 3308 obstacle, a break of which might set the stage for a move to the 3222 level, which is marked near the highs of October 23rd and November 5th.

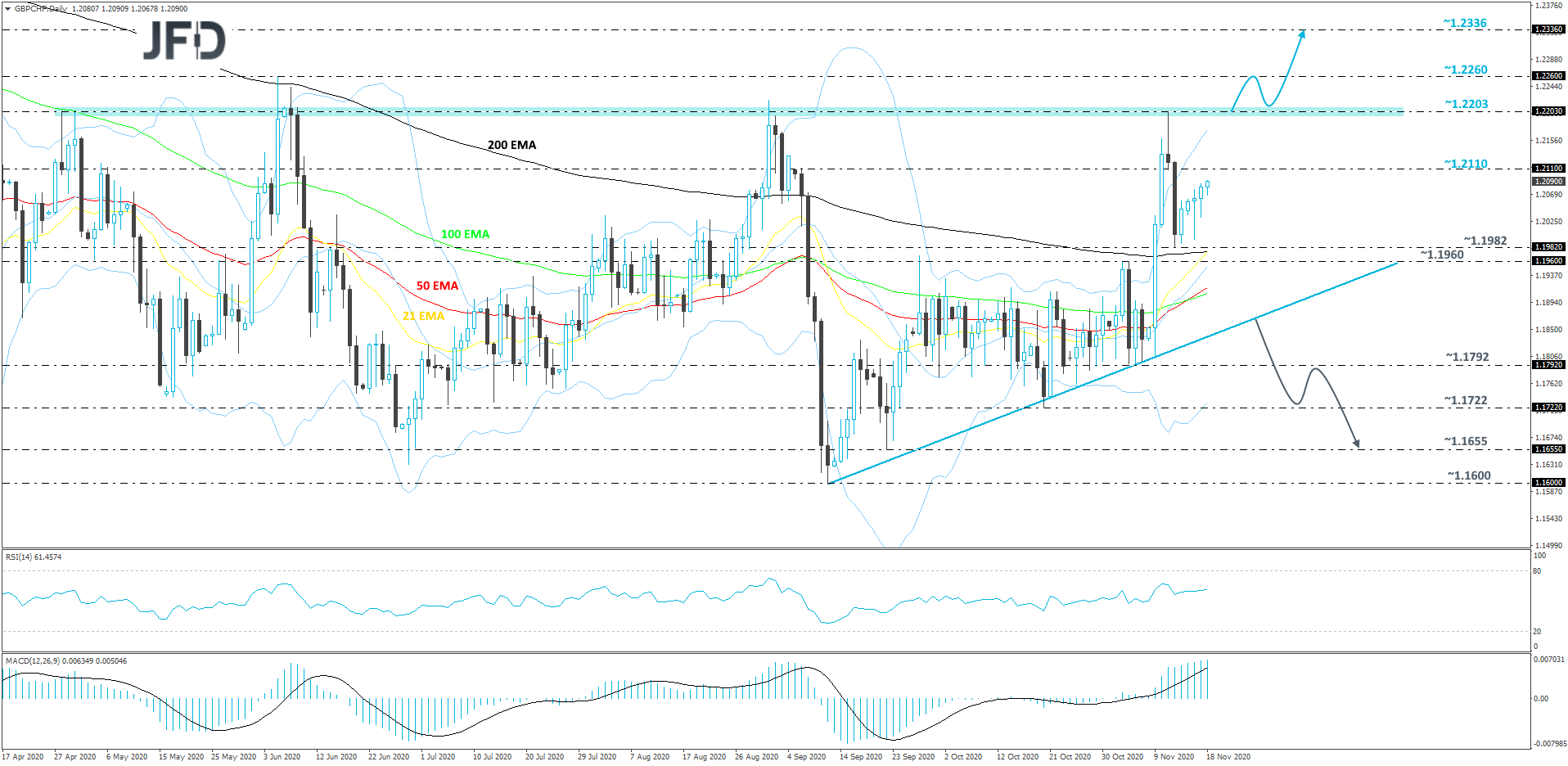

GBP/CHF – TECHNICAL OUTLOOK

For now, GBP/CHF continues to balance above a short-term upside support line drawn from the low of September 11th. Last week, the pair found key resistance near the 1.2203 barrier and then corrected a bit lower, but remained above the 200-day EMA. This week, the rate is showing strength and is trying to move back up again. That said, in order to get comfortable with larger extensions to the upside, we would prefer to wait for a push above last week’s high first, which is at 1.2203. Hence our cautiously-bullish approach for now.

A move above the aforementioned 1.2203 barrier would confirm a forthcoming higher high, potentially inviting more buyers into the game. GBP/CHF may then drift to the 1.2260 obstacle, which if broken might open the door for a test of the 1.2336 level. That level marks the high of March 5th.

On the other hand, in order to start looking at much lower areas, we would need to wait for a break of the previously mentioned upside line first. This move might spook the remaining bulls from the field and allow more bears to join in, especially if the rate falls below the 1.1792 zone, marked near the lows of November 4th and 5th. Then GBP/CHF could travel to the 1.1722 area, which is the lowest point of October, where the pair might find a temporary hold-up. If so, the rate may rebound somewhat, but if it can’t get back above the aforementioned upside line, another slide could be possible. If this time the bears are able to overcome the lowest point of October, the next potential target might be at 1.1655, marked by the low of September 22nd.

AS FOR TODAY’S EVENTS

During the early EU morning, we already got the UK CPIs for October. Both the headline and core rates rose more than anticipated, but the pound barely reacted, confirming our view that GBP-traders are likely to keep their gaze locked on developments surrounding Brexit, rather than economic data.

From the Eurozone, we get the final CPIs for October, but as it is always the case, they are expected to confirm their preliminary estimates.

We get CPIs for October from Canada as well. The headline rate is expected to have ticked down to +0.4% yoy from +0.5%, while there is no forecast available for neither the core rate nor the trimmed mean one. At its latest meeting, the BoC kept interest rates unchanged and scaled back its QE program, noting that the economic outlook has evolved largely as anticipated in the July Monetary Policy Report. Thus, a downtick in headline inflation is unlikely to raise speculation for officials reversing their decision at the upcoming gathering, namely expanding their QE purchases.

From the US, we have building permits and housing starts for October. Both are expected to have increased somewhat from September.

As for tonight, during the Asian session Thursday, Australia’s employment report for October is scheduled to be released. The unemployment rate is expected to have risen to 7.2% from 6.9%, while the net change in employment is forecast to show that the economy has lost 30.0k jobs, after losing 29.5k in September. Another set of soft Australian data may increase speculation with regards more easing from the RBA, and thereby hurt somewhat the Aussie. However, we expect the risk-linked currency to stay mostly driven by developments surrounding the broader market sentiment. As we already noted, we expect investors’ morale to stay supported and thus, we would treat any potential retreat in the Aussie as just a corrective move.