Risk appetite improved on Monday and during the Asian morning Tuesday as investors may have continued placing bets on the prospect of a global economic recovery, despite some fresh tensions between the US and China. Today, we already had an RBA decision, but it was proven a non-event, with the Aussie staying linked to the improvement in the broader market sentiment. Later in the day, investors may also pay some attention to a new round of Brexit talks, the last ahead of the June 18th and 19th EU summit.

INVESTORS KEEP PUSHING RISKY ASSETS NORTH

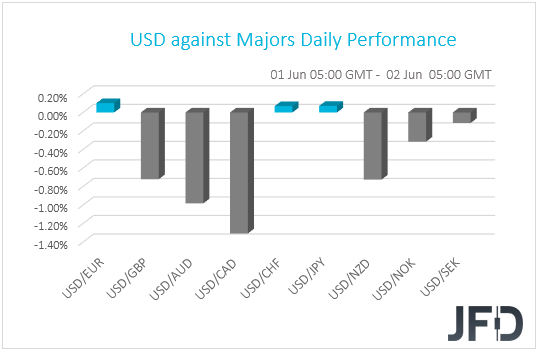

The US dollar continued trading south against most of the other G10 currencies on Monday and during the Asian morning Tuesday. It underperformed the most versus CAD, AUD, and NZD in that order, while it eked out minor gains only against EUR, CHF, and JPY.

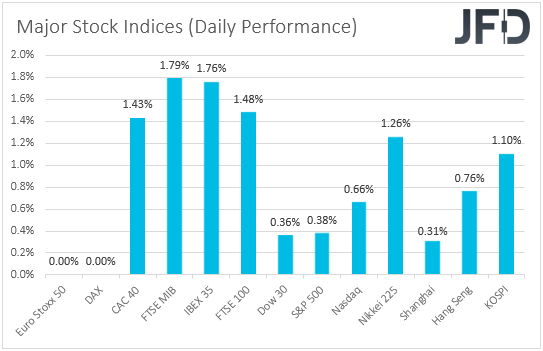

The strengthening of the commodity-linked currencies and the weakening of the safe havens suggest that investors’ appetite remained supported for another day. Indeed, turning our gaze to the equity world, we see that major EU and US indices traded in the green, with the positive morale rolling into the Asian session today.

It seems that investors continued placing bets on the prospect of a global economic recovery as governments around the globe continue to ease their lockdown measures adopted due to the fast-spreading coronavirus. Market participants may have also taken relief after US President Trump announced on Friday that he would end special treatment for Hong Kong, avoiding bold action against China, like the imposition of sanctions and/or fresh tariffs. This may have allowed market participants to maintain hopes that the “Phase One” trade deal between the world’s two largest economies will stay in place and that at some point in the future, the two nations could eventually finalize an accord.

That said, that was tempered somewhat by reports that China has told state-owned firms to stop farm purchases from the US, notably soybeans. Anyhow, China hasn’t been buying US soybeans this year and thus, risk appetite recovered again. Another negative was that US President Trump will send US troops into the streets to control violence triggered by the death of George Floyd in police custody. This may have raised concerns over a national economic recovery, as well as fears of a second wave of coronavirus infections. That said, markets shrugged off this news as well.

As for our view, it has not changed. As we already noted, it seems that investors are more focused on the prospect of a global economic recovery and barring any fresh and more serious tensions between the US and China, they may continue to increase their risk exposures. As we noted several times in the past, among currency pairs, one of the best gauges of the broader market sentiment may be AUD/JPY. As a risk-linked currency, the Aussie may continue to attract flows as investors divert their capital out of safe havens like the yen. In short, we expect AUD/JPY to continue trading north in the near term. We believe that for that to change, the US and China may have to scale back the progress made so far in their trade relationship and/or to start another round of tit-for-tat tariffs.

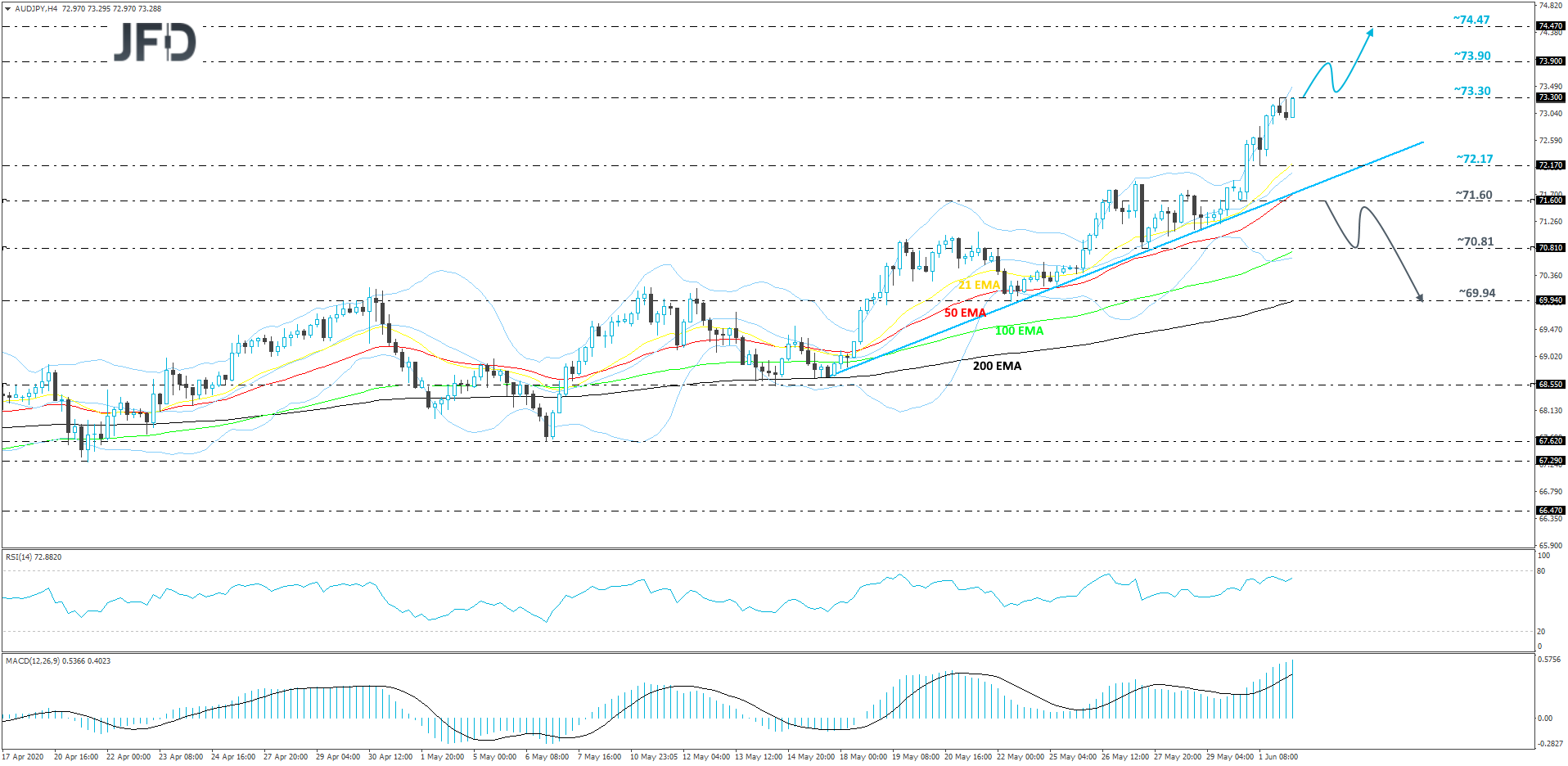

AUD/JPY – TECHNICAL OUTLOOK

AUD/JPY is still comfortably moving higher, while balancing above a short-term upside support line taken from the low of May 15th. This morning, the pair is already testing the high of yesterday, at 73.30, which suggests that the bulls are still willing to drive AUD/JPY higher. We will remain positive and aim for higher areas, as long as the pair stays above the aforementioned upside line.

A strong push above yesterday’s high, at 73.30, would confirm a forthcoming higher high and may set the stage for further advances. AUD/JPY could then drift to the 73.90 hurdle, which is the high of February 24th, a break of which may help the bulls to lift the rate to the highest point of February, at 74.47.

On the downside, if the previously-discussed upside line breaks and the rate falls below the 71.60 zone, which is near yesterday’s low, that may signal a change in the short-term trend. AUD/JPY might then fall under the influence of even more bears, who could send the rate further down. This is when the pair may test the 70.81 obstacle, a break of which might set the stage for a push towards the 69.94 level, marked by the low of May 22nd.

RBA STANDS PAT, BREXIT TALKS RESTART

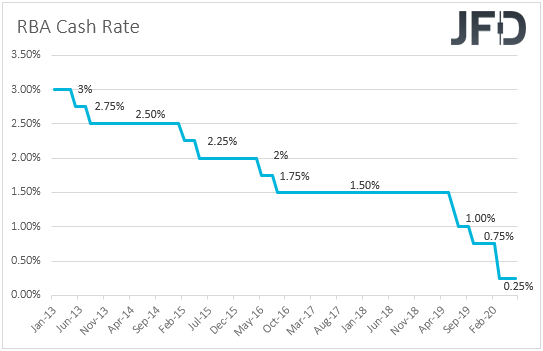

Speaking about the Aussie, during the early morning today, we had an RBA decision. However, there were no fireworks in the aftermath. The Bank kept its benchmark rate and the target of its 3-year government bond yields unchanged at +0.25%, with officials noting that they have purchased government bonds on only one occasion since the previous meeting. They also repeated that they are prepared to scale-up bond purchases again if necessary.

The Aussie barely reacted to the announcement, perhaps as this was the base-case outcome. Remember, yesterday we noted the prospect of better days may have allowed RBA officials to continue reducing their bond purchases. It appears that the main driving force of the Australian currency is the improvement in the broader market sentiment, and as we already noted, we expect this to continue for a while more.

As for today, market participants may pay some attention to the start of another round of Brexit negotiations. This would be the final round ahead of the June 18th and 19th EU summit, by which the UK must decide whether to ask for an extension to the transition period, or not. With PM Johnson insisting over a December 31st deadline, a failure to find common ground is likely to increase fears over a disorderly exit in the end of the year, which combined with the prospect of negative interest rates by the BoE, may keep the pound pressured. That said, we would prefer to exploit any further pound weakness against currencies which we expect to stay strong, like the commodity-linked ones. One of the pairs we would expect to extend its current downtrend is GBP/AUD.

GBP/AUD – TECHNICAL OUTLOOK

GBP/AUD continues its journey south, after the reversal in the beginning of April. The pair is trading below a tentative downside resistance line taken from the highest point of May, which if stays intact could indicate the direction in which the rate might move further. That said, to get a bit more comfortable with further extensions to the downside, we would like to see a drop below yesterday’s low, at 1.8332.

If the pair falls below the above-mentioned hurdle, at 1.8332, that would confirm a forthcoming lower low and more bears could join in and GBP/AUD may slide further south. The pair could easily test the next support area between the 1.8230 and 1.8200 levels, marked by the high of October 9th and by an intraday swing high of October 10th respectively. The rate could stall there initially, or even rebound, however if it continues to trade below the aforementioned downside line, that may be a sign for the sellers to step in again in order to drive the pair down again. If GBP/AUD manages to break the 1.8200 obstacle this time, the next potential support area to consider could be the 1.8075 level, marked by the lowest point of October 2019.

Alternatively, if the previously-discussed downside line breaks and the rate rises above the 1.8549 barrier, marked by yesterday’s high, this could signal a change in the current trend and clear the path for further advances. If so, GBP/AUD may drift to the 1.8659 obstacle, a break of which could set the stage for a test of the 1.8760 hurdle, which is the high of May 19th. The pair might stall there temporarily, however, if the buyers are still feeling comfortable, the next possible resistance zone could be near the 1.8843 level, marked by the low of May 15th and the high of May 17th.

AS FOR THE REST OF TODAY’S EVENTS

The economic calendar for today appears very light with no major economic indicators on the schedule. The only one worth mentioning is the API (American Petroleum Institute) weekly report on crude oil inventories, but as it is always the case, no forecast is available.

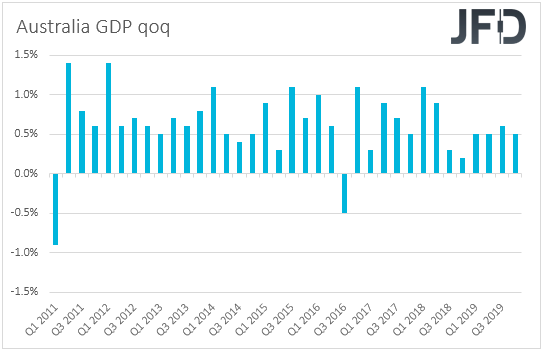

As for tonight, during the Asian morning Wednesday, we get Australia’s GDP for Q1. Expectations are for the economy to have contracted 0.3% qoq after expanding 0.5% in Q4, which will drive the yoy rate down to +1.4% from +2.2%.

Compared to the contraction rates in other major economies, this maybe among the softer ones and would confirm RBA Governor Lowe’s recent remarks that the economic downturn in Australia may not have been as severe as initially thought. In other words, such a print is unlikely to tempt RBA policymakers to start thinking about expanding their stimulus program.

China’s Caixin services PMI for May is also coming out, but no forecast is currently available. That said, bearing in mind the official non-manufacturing index rose to 53.6 from 53.2, we would see decent chances for the Caixin index to have moved in a similar fashion.