We look through potential reasons for the April bounce in fixed income. A stubborn Fed and gloomy Eurozone outlook provide the best, if unsatisfactory, explanations. Upcoming US inflation data and supply offer the most likely drivers for a return to the higher rates trend.

The April bounce is more technical than fundamental

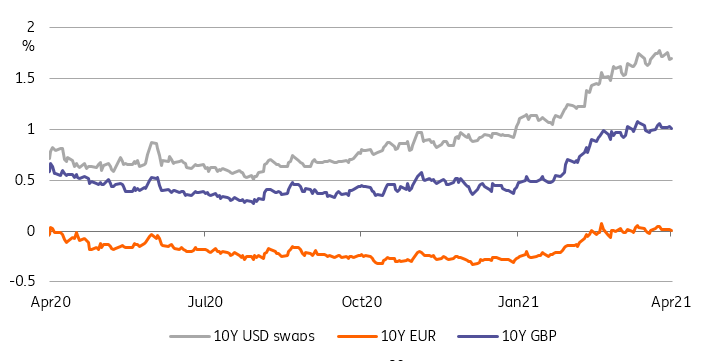

April has proved a good month for fixed income so far, and rates markets have been no exception, be it USD or EUR.

We are tempted to dismiss the rebound in government bonds, and the drop in rates, as technical in nature. Still, since they run counter to our macro view, they warrant further investigation. This should also give us an indication of how rates markets might trade into next week.

In short, we see no reason in data to question our economics team’s bullish outlook on the US economy. If anything, job creation in March surprised to the upside and sentiment indicators confirmed the strength of the upcoming upswing. The same cannot be said in the Eurozone but we feel that survey-based data have at least eased the gloom caused by a third Covid-19 wave. Incidentally, the discrepancy in economic environments is the key reason why we see USD and EUR rates diverge further in Q2, to 190 basis point in 10-year swaps.

The trend towards higher rates has stalled in April

Source: Refinitiv, ING

More credible central banks? Perhaps the ECB

Given the above, we find it difficult to explain why the market would all of a sudden believe the Federal Reserve's forward guidance.

To be sure, the March FOMC minutes were very much on message, but we detect a growing disconnect between their projected rates path and the strength of the recovery. Perhaps the key here is that the Fed can be wrong longer than investors can remain solvent, so extending Fed hike pricing this early before data will prove them right or wrong might seem a bit of a stretch. For what it’s worth, we don't think that Fed Fund rates two-year forwards above 30bp look stretched when one takes into account the term premia necessary to reflect exceptionally wide confidence bands this far ahead.

In Europe, it is also tempting to attribute some of the fixed income strength to a greater degree of ECB credibility. After all, its decision to ramp up purchases for three months combined with the Covid-19 gloom could account for EUR rates’ failure to follow their USD peers higher, but the latest ECB minutes did not suggest a firm conviction that the central bank needs to suppress rates at all costs.

As far as we can tell, technical factors might also be at play here, as elevated government bond redemptions in April should bring higher ECB reinvestments, on top of the faster net purchases announced in March.

Today’s events and market view: the April bounce to the test

We find none of the above explanations satisfactory on their own, although the central bank credibility argument holds most water in our view.

Going forward, the fixed income rebound will be put to the test fairly quickly. First up, the US producer price index is expected to jump to 3.8% in February (release is today), and CPI to 2.5% in March (release next Tuesday). Both are headline figures, and both year-on-year are likely to be heavily distorted by last year’s slump, both the month-on-month prints look similarly strong if consensus is anything to go by.

USD rates markets will also have to contend with long-dated US Treasury supply next week. If the recent bounce has been on the back of strong buying flow, then these should pose no particular challenge. Still, the rebound has been strongest in the belly of the curve, so we are unsure how much support this could lend to the long end. We find it prudent to stick to our bearish USD rates view into next week, but it could affect the long-end more due to supply.

Central bank speakers today include ECB VP Luis de Guindos and Dallas Fed president Robert Kaplan. Fed President Jerome Powell repeated his dovish mantra yesterday, judging that the spike in inflation mentioned above will be temporary and that much progress remains necessary on the job market.

Original Post

Content Disclaimer: The information in the publication is not an investment recommendation and it is not an investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.

This publication has been prepared by ING solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. Read more