The US dollar traded higher against all the other major currencies yesterday and today in Asia, with equities pulling back after US President Joe Biden picked Jerome Powell to lead the Federal Reserve Bank for a second term, enhancing expectations over a potential rate hike next summer.

As for today, the main items on the agenda may be the preliminary PMIs for November from the Eurozone, the UK, and the US. They will provide a glance as to how those major economies have been dealing with the latest supply shortages, and perhaps impact expectations around their respective monetary policies. Tonight, the RBNZ is anticipated to hike interest rates again, but the big question is by how much.

US Dollar Gains and Equities Pull Back as Biden Picks Powell

The US dollar traded higher against all the other major currencies on Monday and during the Asian session Tuesday. It gained the most versus NZD, JPY, and CAD in that order, while it eked out the least gains versus CHF.

The strengthening of the greenback and the weakening of the risk-linked Kiwi suggest that the financial community may have traded in a risk-off fashion yesterday and today in Asia. However, the weakening of the yen points otherwise.

Thus, in order to clear things up with regards to the broader market sentiment, we prefer to turn our gaze to the equity world. There, major EU indices were mixed, with some of them recovering a portion of last week’s late losses due to announcements for fresh lockdowns around to bloc in order to fight the 4th wave of the pandemic.

The main gainers were telecommunications, gaining following the announcement that US fund KKR is interested in buying Telecom Italia, which suggests that investors bet on the possibility of similar corporate movements elsewhere.

The sentiment was dented more after US President Joe Biden picked Jerome Powell to lead the Federal Reserve Bank for a second term. Given that the other potential candidate was Fed Governor Lael Brainard, who is seen by many as more dovish than Powell on monetary policy, Powell’s nomination reinforced expectations that the Fed could push the hike button in the middle of next year, and perhaps once more by the end of it.

Brainard was appointed as Vice-Chair, and surprisingly, in her aftermath remarks appeared also committed to getting inflation down. Maybe that added extra fuel to the short selling in Wall Street, especially in NASDAQ Composite, which mainly constitutes high-growth tech stocks.

Let’s not forget that expectations over higher interest rates also mean lower present values for such companies. Anyhow, a dove as a Vice-Chair could still raise questions as to whether they could push the hike button as soon as next summer, but her comments imply that there may be more members supporting such an action than initially thought.

Ahead of Biden’s announcement, the Fed funds futures were pointing to the first post-pandemic hike to be delivered in July. Now, they point to June.

In our view, all this means that the US dollar could continue sailing north, but what about equities? Yes, we could see some more declines, on expectations of faster rate hikes, but, in our view, investors may have already digested the idea of higher rates soon to some extent.

We believe that they are more focused on indications and proves as to how the US economy has been performing, and as long as everything points to resilience, they may stay willing to buy again. Thus, for now, we will class yesterday’s retreat, or any short-term extensions of it, as a corrective move.

NASDAQ 100 – Technical Outlook

The NASDAQ 100 cash index fell sharply yesterday, after hitting a fresh record high, at around 16760. That said, the index is still trading above the 16300 zone, and the upside support line drawn from the low of Oct. 13. We would like to see a dip below that crossroads before we abandon the bullish case. For now, we would still examine the case of a potential rebound from that line.

If the bulls are strong enough to take charge from near that support area, we could see them pushing the action back, towards the 16760 zone. If they don’t stop there this time around, a break higher would take the index into uncharted territory and perhaps aim for the psychological round figure of 17000. If that zone is broken as well, then we would expect to see advances towards the 17300 territory.

In order to consider a bearish reversal, we would like to see a dip below the aforementioned upside line, but also a subsequent slide below 16090. This could invite more bears into the game, who, in their turn, could push the battle down the low of Nov. 10, at around 15900, or the low of Nov. 1, at around 15780.

If neither level is able to halt the slide, we may see the fall extending towards the 15600 area, marked by the low of Oct. 29, or even to the 15310 territory, which provided support between Oct. 21 and 25.

Flash PMIs To Provide an Updated Picture of Major Economies

As for today, the main items on the agenda may be the preliminary PMIs for November from the Eurozone, the UK, and the US. Getting the ball rolling with the Eurozone, both the manufacturing and services indices are expected to have continued sliding, resulting in the 4th consecutive slide to the composite index.

This will add to concerns that the latest supply shortages and bottlenecks have left their marks on the Euro-area economy and combined with the latest lockdown measures around the bloc, could add more credence to the recent remarks by ECB President Lagarde that tightening monetary policy now to rein in inflation could choke off the euro zone's recovery.

Thus, with all that in mind, we believe that sliding PMIs could prompt EUR traders to push further back their bets over a potential rate hike by the ECB next year, and thereby keep the euro under selling pressure.

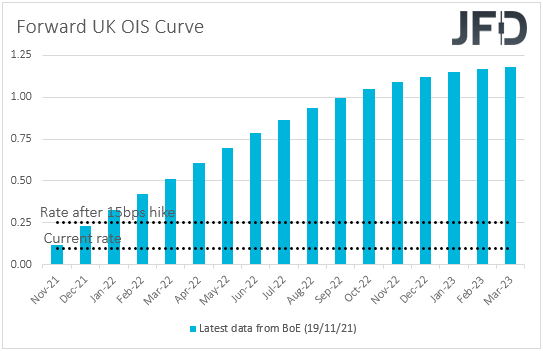

Now, moving to the UK, both the manufacturing and services indices are forecast to have declined here as well, with the composite index expected to fall to 54.1 from 57.8. At its latest meeting, the BoE decided not to hike, despite market participants assigning an 80% chance for such a move ahead of the meeting, and instead said that this could happen in “coming months”.

However, soon thereafter, Governor Andrew Bailey said that they are still on a path towards raising interest rates, remarks which combined with further acceleration in inflation last week, encouraged investors to place bets over a December hike. According to the UK Overnight Index Swaps (OIS) forward yield curve, such a move is nearly fully priced in, but a disappointment in the PMIs may raise fresh questions on the matter, and perhaps result in a pullback in the pound sterling.

Now, flying to the US, in contrast to the Eurozone, there, both the manufacturing and services PMIs are forecast to have increased, underscoring the resilience of the US economy and perhaps adding more validity to the view over a potential rate hike by the Fed in the middle of next year.

EUR/USD – Technical Outlook

EUR/USD continued sliding yesterday, falling below Friday’s low of 1.1250. Overall, the pair continues to trade below the downside resistance line drawn from the high of May 25, but since Nov. 9, it’s been respecting a new steeper line, which paints an even more negative picture.

In our view, the dip below 1.1250 may have opened the path towards the 1.1170 zone, which provided support back on June 19 and 22, 2020. If the bears are willing to dive lower, then we could see them putting the 1.1100 area on their radars. That zone is defined as a support by the low of June 1, 2020.

In order to abandon the bearish case temporarily and start examining a decent correction to the upside, we would like to see a rebound back above 1.1375, the high of Nov. 18. This could wake up some bulls, who could climb towards the 1.1432 barrier, marked by the inside swing low of Nov. 12, or towards the peak of that day, at 1.1465.

Another break, above 1.1465, could see scope for advances towards the 1.1524 area, which acted as a floor for the pair between Oct. 6 and Nov. 5.

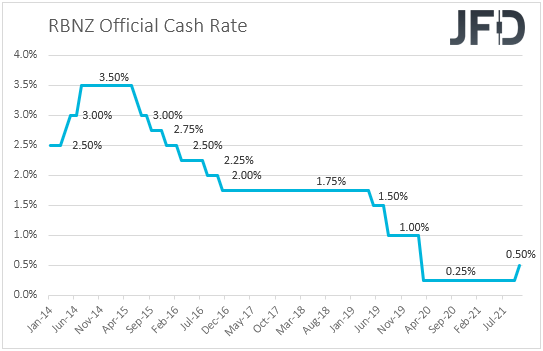

RBNZ Set to Hike Rates, But by How Much?

Tonight, during the early Asian morning, we have a central bank deciding on interest rates and this is the RBNZ. Back in October, the bank raised interest rates by 25 bps as was widely expected, noting that further removal of monetary policy stimulus is expected over time.

With the New Zealand CPI surging to 4.9% in Q3, and the unemployment rate hitting a record low during the same quarter, market participants are almost certain that officials will hit the hike button again this week. The main question though is whether they will add 25 or 50 bps. According to market chatter, there is around a 40% chance for a “double hike”.

In our view, despite the domestic economy performing very well, there are other major economies still facing problems, one of which is China, New Zealand’s biggest trading partner. Thus, we believe that there is no reason for RBNZ policymakers to rush into delivering more than a 25 bps increase.

This could disappoint those expecting more and may result in a pullback in the Kiwi at the time of the announcement. However, conditional upon the bank staying willing to continue normalizing its policy, the retreat may stay limited and short-lived. After all, the RBNZ will be the only major central bank raising interest rates post-pandemic, not once, but twice.

Elsewhere

Besides the PMIs, the only other release worth mentioning is the API report on crude oil inventories for last week, but as it is always the case, no forecast is available.

We also have three speakers on the agenda and those are ECB Vice President Luis de Guindos, BoE MPC member Jonathan Haskel, and BoC Deputy Governor Paul Beaudry.