Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

We first rang alarm bells on this company when it went public in April 2015. Since then, profits have declined and the market has grown more competitive, yet the stock has tripled.

Now, the firm’s lack of resources (relative to competitors) and low profitability make the expectations baked into the stock price look overly optimistic. These issues, and more, make Godaddy Inc (NYSE:GDDY) (: $61/share) this week’s Danger Zone pick.

Revenue Growth and Accounting Earnings Mislead Investors

We leverage our Robo-Analyst technology to analyze the footnotes and MD&A in company filings to get an accurate look at a company’s true profitability. Through this work, we find that GoDaddy’s GAAP net income was artificially increased in 2017 due to hidden (and non-hidden) non-operating income.

We made 10 adjustments to GoDaddy’s 2017 income statement, with a total value of $279 million. One of the larger adjustments was the removal of $32 million (23% of GAAP net income) in non-operating income related to the gain on sale of PlusServer. We also removed $123 million (90% of GAAP net income) in tax receivable agreement liability adjustments included on the income statement.

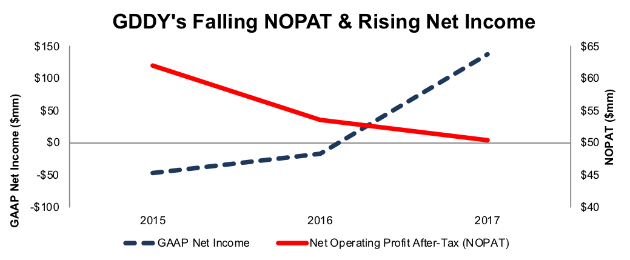

After taking into account all adjustments, we removed $86 million in non-operating income from GAAP net income. These adjustments revealed that despite GAAP net income increasing from -$17 million in 2016 to $136 million in 2017, after-tax profit (NOPAT) fell from $54 million to $50 million over the same time.

This disconnect in GAAP net income and the true recurring profits of the business is not new either. Since 2015, GDDY’s net income has grown from -$47 million to $136 million while NOPAT has fallen 10% compounded annually, per Figure 1.

Figure 1: GDDY’s Misleading GAAP Net Income

Sources: New Constructs, LLC and company filings

The decline in NOPAT stems from NOPAT margins falling from 4% in 2015 to 2% in 2017. At the same time, average invested capital turns, a measure of balance sheet efficiency, have fallen slightly from 0.70 in 2015 to 0.68 in 2017. Falling margins and inefficient capital use have dropped GDDY’s return on invested capital (ROIC) down from 3% in 2015 to 2% in 2017.

Lack of Comparability in Shifting Non-GAAP Metrics

We’ve long warned investors about companies using non-GAAP metrics to obscure actual profits. GoDaddy’s use of non-GAAP takes this misleading practice one step further and limits comparability to previous years by changing the non-GAAP metric on which they tell investors to focus. At the end of 2016, GoDaddy stopped reporting adjusted EBITDA, which removed significant expenses, such as equity-based compensation, from its calculation. In its place, the firm began reporting “unlevered free cash flow”, which is supposed to “evaluate the business prior to the impact of its capital structure and after-tax distributions”. Unlevered free cash flow adds back cash paid for interest and cash paid for acquisition-related costs.

Both metrics significantly overstate the profitability of the business. Adjusted EBITDA removes real operating expenses and completely ignores the balance sheet, while “unlevered free cash flow” doesn’t take into account the costs of acquisitions, like GoDaddy’s $1.8 billion acquisition of HEG in 2017. Switching between the metrics exaggerates their flaws by making it difficult to compare profitability between periods.

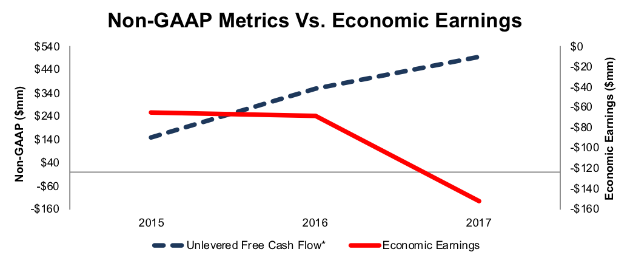

In either case, Figure 2 shows that non-GAAP metrics provide a misleading picture of GDDY’s profitability. From 2015-2016, adjusted EBITDA increased from $147 million to $263 million. When calculating adjusted EBITDA, GoDaddy removed $40 million (>100% of net income) and $57 million (>100% of net income) in equity-based compensation expense in 2015 and 2016 respectively. Meanwhile, economic earnings, the true cash flows of the business, fell from -$65 million to -$68 million.

Figure 2: GDDY’s Non-GAAP Metrics Paint False Picture of Firm

* Prior to 2016, GDDY reported Adjusted EBITDA, which was replaced by Unlevered Free Cash Flow in 2016

Sources: New Constructs, LLC and company filings

From 2016-2017, unlevered free cash flow rose from $357 million to $496 million, while free cash flow fell from $161 million to -$1.5 billion and economic earnings fell from -$68 million to -$152 million.

Compensation Plan Rewards Execs Despite Shareholder Value Destruction

GoDaddy’s executive compensation misaligns executives’ interests with shareholders’ interests. The misalignment helps drive the profit decline shown in Figures 1 and 2.

GoDaddy’s executives earn annual cash bonuses based on the achievement of corporate and individual performance goals. The corporate performance goals include bookings, adjusted EBITDA, unlevered free cash flow, and total customers. Equity awards are given in either time-based options or performance-based stock units, which are also tied to bookings and adjusted EBITDA.

As noted above, these non-GAAP metrics do little to measure the true profitability of the firm. Instead, they include numerous adjustments that allow executives to earn bonus awards while destroying shareholder value. We’ve demonstrated through numerous case studies that ROIC, not non-GAAP net income or similar metrics, is the primary driver of shareholder value creation. A recent white paper published by Ernst & Young also validates the importance of ROIC and the superiority of our data analytics. Without major changes to this compensation plan (e.g. emphasizing ROIC), investors should expect further value destruction.

GoDaddy’s Brand Name Can’t Outlast Superior Competition

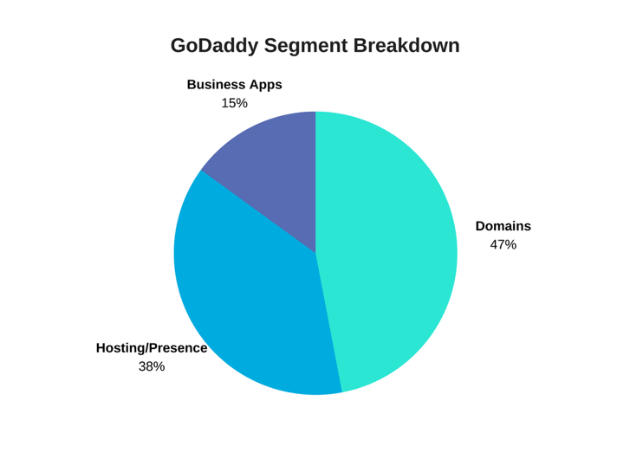

GoDaddy may be best known for its flashy Super Bowl ads from years ago, but the company operates in three main segments: domains, hosting & presence, and business applications. See Figure 3.

Figure 3: Domains Still Make Up Largest Portion of Revenue

Sources: New Constructs, LLC and company filings

GoDaddy may have had an advantage at one point due to its superior brand recognition, but its advantage has disappeared. Customers today are just as familiar, if not more so, with many of its competitors.

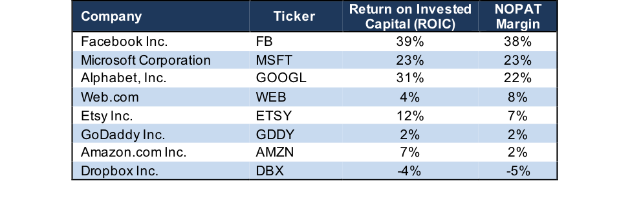

Per Figure 4, GoDaddy’s margins and ROIC, rank well below its largest competition (as noted in its 10-K) and only outrank previous Danger Zone Pick Dropbox (DBX). More alarming, GoDaddy’s margins have declined despite diversifying its business away from the commoditized domain registration business.

Figure 4: GoDaddy’s NOPAT Margin Ranks Near the Bottom

Sources: New Constructs, LLC and company filings

GoDaddy Losing Ground in Commoditized Domain Registration

The domains segment allows customers to register and purchase domain names. This segment is largely commoditized, as the price registrars pay for domains is set by VeriSign (NASDAQ:VRSN), which holds a contract to distribute domain names from the Internet Corporation for Assigned Names and Numbers (ICANN). This contract runs through 2024 and sets a standard price on the cost of domains. With set costs, this segment provides little room for margin expansion despite being GoDaddy’s largest revenue source.

Domain registration competitors include Web.com (NASDAQ:WEB), namecheap.com, DreamHost, United Internet, Donuts, Google (NASDAQ:GOOGL) – which recently entered the domain registration market – and more.

Even worse, what was once GoDaddy’s namesake business is losing ground. From 2014-2016, GoDaddy’s market share in domain registration fell from 21% to 19%. It jumped back to 22% in 2017, but largely due to GoDaddy’s acquisition of Host Europe Group, which added 1.6 million customers. With dwindling capital (more on this below) GoDaddy cannot rely on acquisitions to boost market share.

Hosting and Site Creation Are Not Strengths Either

The hosting & presence segment offers website hosting services as well as tools to build websites and online stores. GoDaddy provides these services in an effort to diversify its revenue sources while also providing additional value to its customers.

Website hosting and creation competitors include Amazon Web Services (NASDAQ:AMZN), Automattic (owner of WordPress), Shopify (NYSE:SHOP), Squarespace, Weebly, Wix (NASDAQ:WIX), and more. Unfortunately for GoDaddy, its site creation lags many of its competitors, in both market share and function. According to Datanyze, which calculates market share for web technologies, Wix is the leader in website building with a 23% market share. Squarespace comes in second with 17%, while Weebly has 15% and GoDaddy has just 9% of the market.

Additionally, numerous reviews note that GoDaddy’s site builder, which does not offer a free version, lacks standard features often provided by free competitors. Product integration (domain and site building) can be a positive add-on, but only if you’re offering clients the best available services and tools.

Business Applications Market Dominated by Tech Giants

Lastly, the business applications segment includes email accounts, email marketing tools, and IP-based telephone services.

Business application competitors include tech giants such as Microsoft (NASDAQ:MSFT) and Google (via Gmail), and Dropbox (NASDAQ:DBX). Social platforms and third-party e-commerce sites such as Facebook (NASDAQ:FB) or Etsy (NASDAQ:ETSY) also present competition as they provide sales and marketing capabilities outside of creating a traditional website.

We don’t think it is likely that this business segment will generate much, if any, profit growth given the stiff competition and relatively weak offerings of GoDaddy.

Bull Case Ignores A Commoditized Product, Years with No Profits, Rising Costs, & Less Flexibility

Despite being founded in 1997, GoDaddy’s first reported accounting profits occurred in 2017. As we noted earlier, this reported profit was artificially achieved with significant unusual income. Because of the lack of real profits, investors have chosen to focus on revenue growth and customer growth, while ignoring real issues in the business. As the industry slows, rising costs and lack of resources in a highly competitive (and commoditized) industry threaten any bull case.

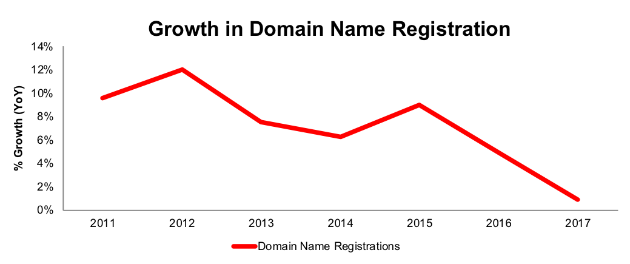

According to Verisign’s Domain Name Industry Brief reports, the growth in domain name registrations is slowing significantly. Per Figure 5, top level domain name registrations grew 1% year-over-year in 2017, down from 10% year-over-year in 2011.

Figure 5: Domain Name Registration Growth is Slowing

Sources: New Constructs, LLC and company filings

Despite the slowing growth of domain registrations, GoDaddy achieved record revenues in 2017 and grew its customer base by 18% (11% came from an acquisition). However, its operating expenses grew even faster. Year-over-year, general & administrative, technology & development, and customer care costs grew 28%, 24%, and 21%, respectively. Cost of revenues and marketing and advertising grew 18% and 11% YoY as well. For reference, revenue grew 21% YoY.

Making matters worse, some of these costs may not be reduced, unless GDDY sacrifices key functions. For instance, customer care expenses represent the cost to advise and service customers. As GoDaddy strives to increase customer count, it must also increase customer care. For a firm already plagued with numerous complaints regarding its customer care, this cost structure could prove a challenge to sustaining customer growth and achieving profitability.

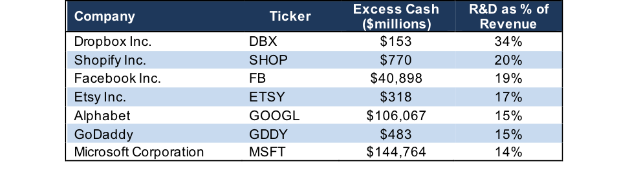

Beyond cost concerns, GoDaddy lacks the capital and the operational flexibility to grow at rates required by its valuation. GoDaddy’s excess cash is dwarfed by its more profitable competitors.

Figure 6: GoDaddy’s Spending and Capital Resources Lag Competition