Most EU and US stock indices gained yesterday, but today, during the Asian session, sentiment took a 180-degree spin after US President Donald Trump was tested positive for the coronavirus.

As for today, the main event is likely to be the US employment report for September. In the currency world, the pound was the main loser among the G10s, coming under selling interest following negative headlines with regards to the EU-UK relationship.

EU And US Shares Gain, But Asian Slide As Trump Tested Positive For COVID

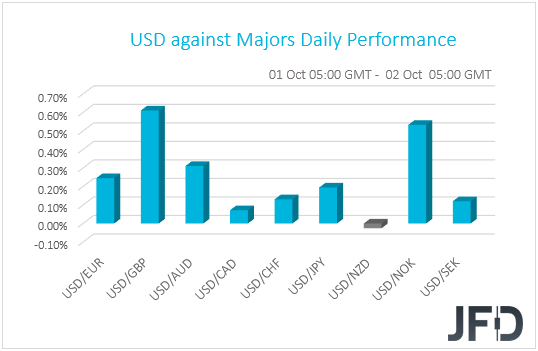

The US dollar traded higher against all but one of the other G10 currencies on Thursday and during the Asian morning Friday. It gained the most versus GBP, NOK, and AUD, while it was found virtually unchanged against NZD.

The strengthening of the greenback suggests that financial markets traded in a risk-off fashion, but the fact that the Kiwi was also strong suggests otherwise. Thus, in order to clear things up, we prefer to turn our gaze to the equity world.

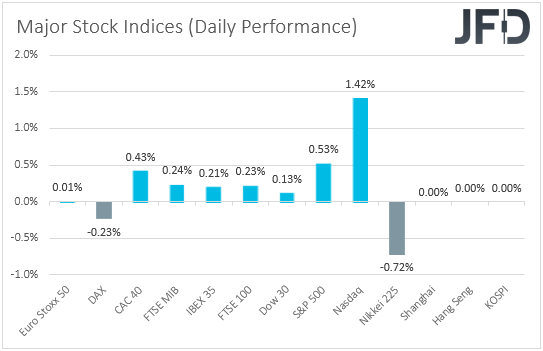

There, most EU and US indices closed in positive territory, with NASDAQ gaining the most (1.42%), driven again by market leaders such as Amazon (NASDAQ:AMZN), Microsoft (NASDAQ:MSFT) and Apple (NASDAQ:AAPL).

The exception was DAX, which slid 0.23%, weighed down by a 13.1% slump in Bayer (OTC:BAYRY), after the firm signaled that adjusted profit may decline in 2021 and that it is likely to write down the value of agriculture assets by nearly EUR 10bn.

Sentiment was softer during the Asian session today, with Japan’s Nikkei 225 falling 0.72% following headlines that US President Donald Trump was tested positive for the coronavirus. China’s, Hong Kong’s, and South Korea’s markets remained closed.

Despite most indices trading again in the green, we repeat that we are reluctant to trust a long-lasting recovery. Covid infections continue to rise at a fast pace, with yesterday’s new global cases nearing their record, which adds to concerns over more lockdown measures around the world.

Madrid is the first capital to go back into lockdown, while British health minister introduced more coronavirus restrictions across a wider area of England. On top of COVID, another source of concern may be the US election, scheduled to take place on Nov. 3. As we get closer to the election day, investors may start getting more nervus.

US Employment Report Takes Center Stage

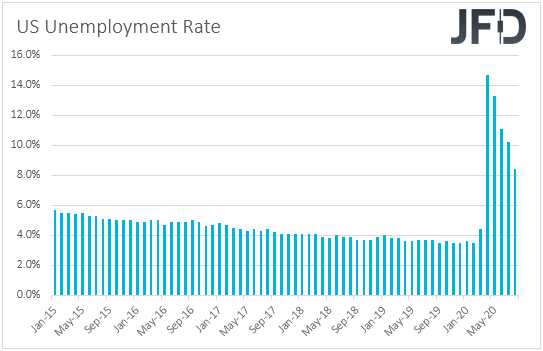

Having said all that though, now, market attention is likely to fall on the US employment report for September, due out later today. NFPs are forecast to have increased by 850k, less than August’s 1.371mn, but still a solid number which is consistent with further improvement in the labor market.

The unemployment rate is expected to have declined more, to 8.2% from 8.4%, while average hourly earnings are forecast to have accelerated somewhat, to +4.8% yoy from +4.7%.

At its most recent meeting, the FOMC kept its policy unchanged, but changed its inflation language noting that they “will aim to achieve inflation moderately above 2% for some time so that inflation averages 2% over time”.

With regards, to the new economic projections, officials revised up their GDP and inflation forecasts, and downgraded the unemployment rate ones, while the new dot plot suggested that interest rates are likely to stay at present levels at least through 2023.

That said, looking at the details, we see that one member was in favor of a hike in 2022, and four saw rates higher in 2023. Combined with the inflation forecast of 2023, which is at 2%, this shows that some members may not be willing to tolerate inflation above target for long as pointed in the decision statement.

Thus, a decent employment report, although it would be a sign that the economic recovery continues, may raise speculation that interest rates in the US may rise somewhat faster than previously anticipated.

Something like that may prove positive for the US dollar, but negative for equities. Equity investors may prefer extra-loose monetary policy for longer, as this means cheap loans for companies.

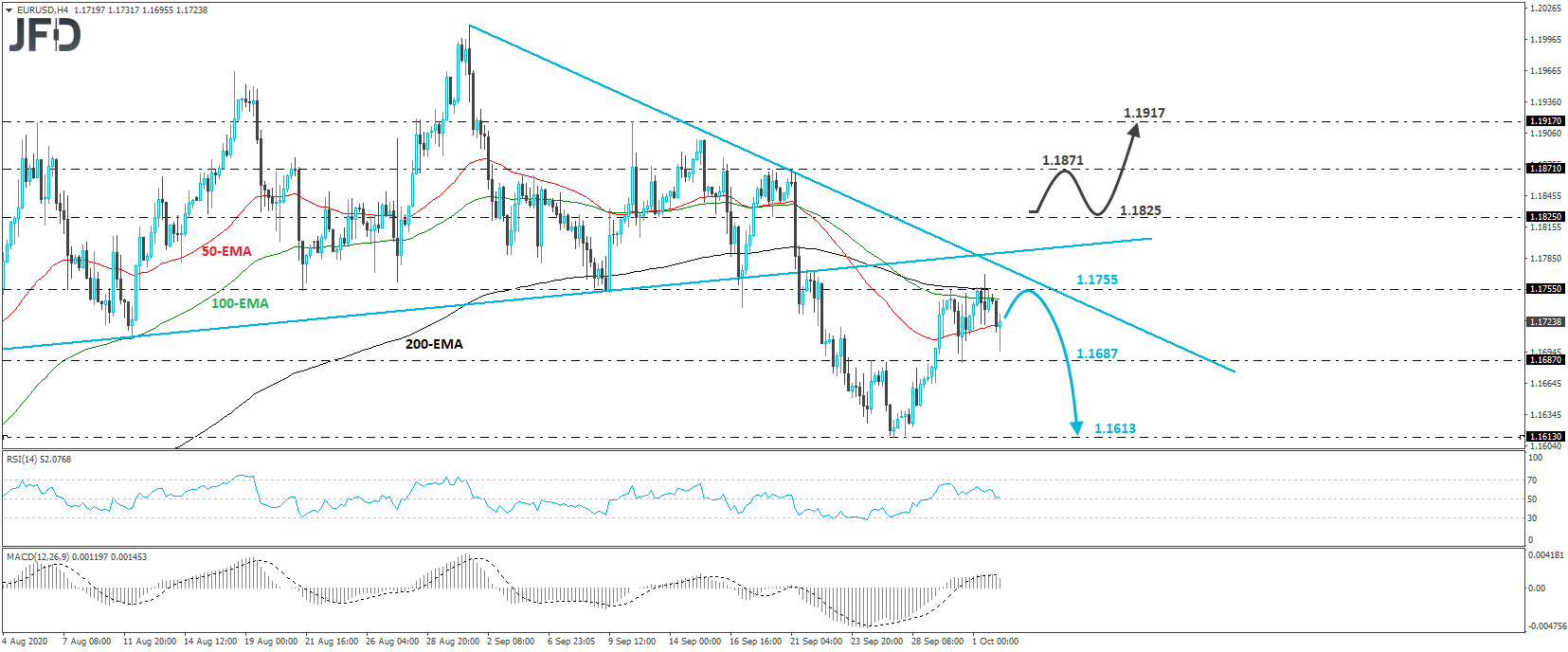

EUR/USD Technical Outlook

EUR/USD traded lower yesterday, after hitting resistance near the 1.1755 territory. Overall, the rate remains below the downside resistance line drawn from the high of Sept. 1, as well as below the prior upside one taken from the low of Aug. 3. All these technical signs keep the short-term outlook negative in our view.

Today, the rate started to rebound somewhat, but even if this continues, we see decent chances for the bears to take charge again near the 1.1755 zone, or near the aforementioned downside line. If this is the case, we may see another test near the 1.1687 barrier, marked by Wednesday’s low, the break of which may pave the way towards the low of September 25th, at around 1.1613.

On the upside, we would like to see a strong break above 1.1825 before we start examining whether the bulls have gained the upper hand. Such a move would take the rate above both the pre-discussed diagonal lines and may encourage advances towards the highs of September 18th and 21st, at 1.1871. Another break, above 1.1871, could carry more bullish implications, perhaps targeting the peak of Sept. 10, at 1.1917.

Sterling The Main G10 Loser On Fresh Brexit Woes

Flying from the US to the UK, the British pound was the main loser among the G10 currencies, coming under strong selling interest following headlines that the EU and the UK failed to close their differences-gap in the latest round of trade talks, and that the EU began legal proceedings over the UK’s plan to override key elements of the withdrawal agreement.

Remember that, on Monday, headlines hit the wires that a final trade accord was possible in this round of talks, with one EU official noting last week that the deal is 90% there. This helped the pound to sail north, but yesterday’s news have diminished any hopes with regards to a trade deal before the upcoming EU summit, something which brings back to the table the prospect of a no-deal Brexit at the end of the year, when the transition period expires.

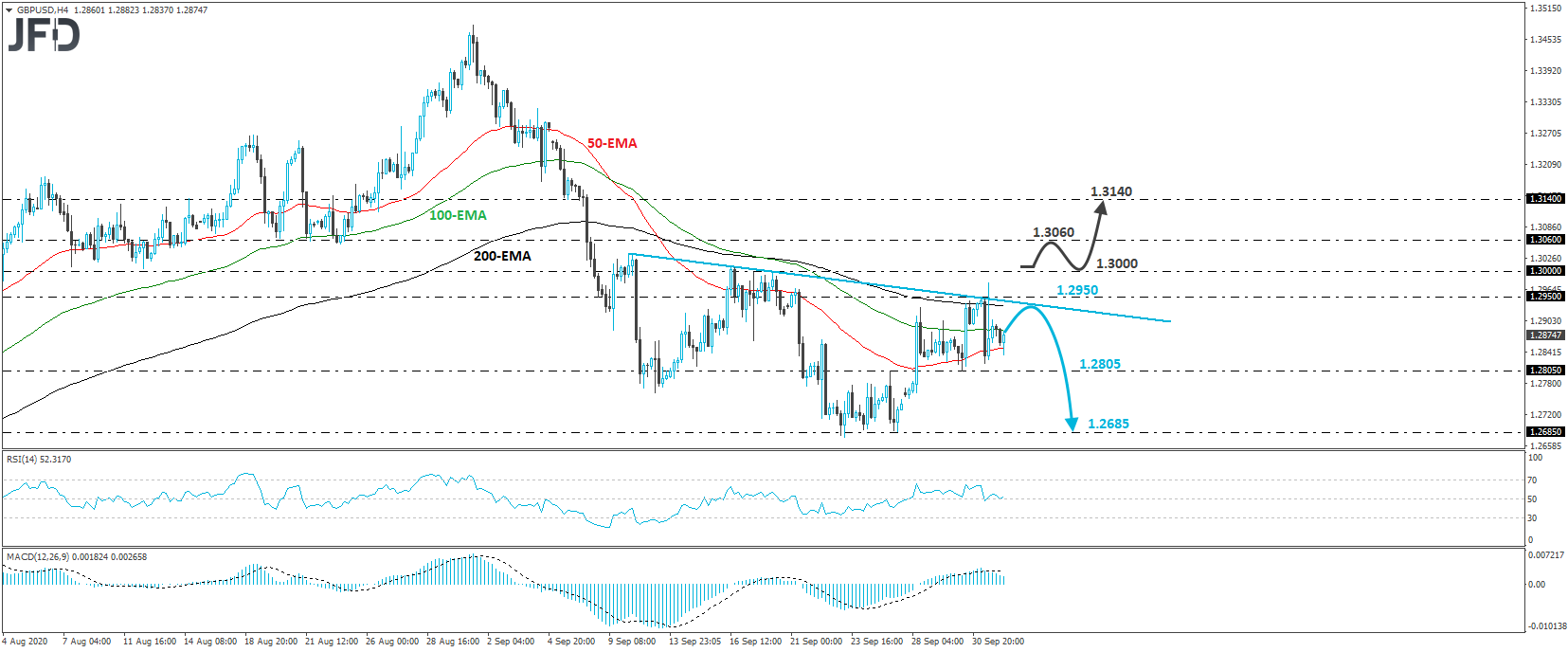

GBP/USD Technical Outlook

GBP/USD edged south yesterday after hitting resistance near the 1.2950 level. That said, the rate found support slightly above 1.2805 and starter to recover thereafter. Although the recovery may continue for a while more, as long as the rate stays below the downside resistance line drawn from the high of September 10th, we would consider the near-term outlook to be cautiously bearish.

If the bears are willing to take charge from near the downside line, we may see them aiming for another test near the 1.2805 barrier, which is Wednesday’s low. If they don’t stop there, we may see them diving towards the 1.2685 territory, which provided strong support between September 23rd and 25th.

Now, in order to start considering the bullish case, we would like to see a strong rebound back above the psychological zone of 1.3000. The rate would already be above the pre-mentioned downside line and the bulls may push the battle up to the 1.3060 zone, which provided support between Aug. 20 and 25. Another break, above 1.3060, may see scope for extensions towards the inside swing low of Sept. 7, at 1.3140.

As For The Rest Of Today's Events

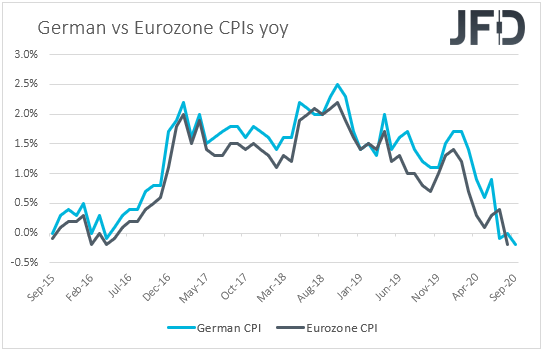

During the European morning, we get the preliminary Eurozone inflation data for September. According to some economic calendars, the data was scheduled for Wednesday, but it was not released.

In any case, the headline rate is forecast to have held steady at -0.2% yoy, while no forecast is available for the core one. That said, the HICP excluding food and energy metric is expected to have accelerated to +1.1% yoy from +0.6%. Bearing in mind that both the German CPI and HICP rates slid by more than anticipated, entering negative waters, we see the risks surrounding the bloc’s headline rate as tilted to the downside.

At the prior ECB meeting, policymakers kept monetary policy untouched, reiterating that they stand ready to adjust all their instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner.

Following the worse-than-expected PMIs for September, with the services sector slipping into contraction, a further decline of the headline CPI into the negative territory may increase speculation for additional stimulus by the ECB.

However, the fact that the core HICP rate is expected to have accelerated means that the weak headline CPI rate may be the result of declines in energy and food, which may allow policymakers to wait for a while more before they decide to push the easing button. They may prefer to wait and see whether the deflationary rate is something temporary or not.

In the US, apart from the official employment data, we also get the factory orders for August and the final UoM consumer sentiment index for September.

As for the speakers, we have two on today’s schedule: ECB Vice President Luis de Guindos and Philadelphia Fed President Patrick Harker.