Global equities traded well in the green on Monday as both infected cases and deaths due to the coronavirus slowed down on Sunday. In the FX world, the risk-linked currencies Aussie and Kiwi were among the main gainers, with the former getting an extra boost from the less-dovish-than-expected RBA, while the safe havens dollar, yen and franc traded on the back foot.

RISK ASSETS GAIN, SAFE HAVENS SLIDE ON VIRUS SLOWDOWN

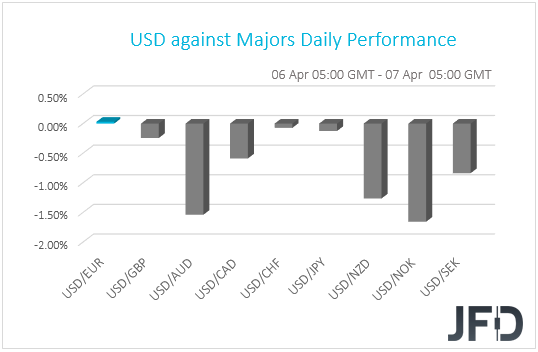

The dollar traded lower against the majority of the other G10 currencies on Monday and during the Asian morning Tuesday. It lost the most ground versus NOK, AUD and NZD in that order, while it underperformed the least against GBP and JPY. The greenback was found virtually unchanged against CHF and EUR.

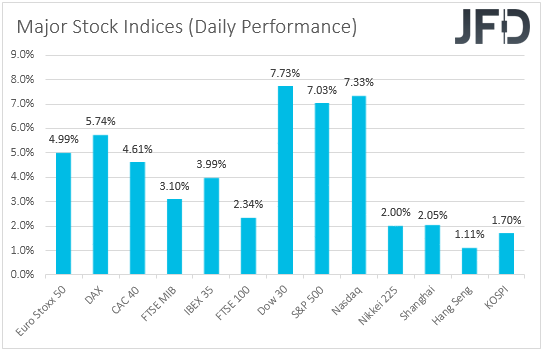

The strengthening of the risk-linked currencies Aussie and Kiwi, combined with the weakness of the dollar, the yen and the franc, suggests that market participants traded in a risk-on manner yesterday. Indeed, major EU indices closed in green territory, with risk appetite accelerating during the US session. All three main Wall Street indices gained at least 7%. The positive investor morale rolled over into the Asian session today but eased somewhat. At the time of writing, Japan’s Nikkei and China’s Shanghai Composite are up 2.00% and 2.05%.

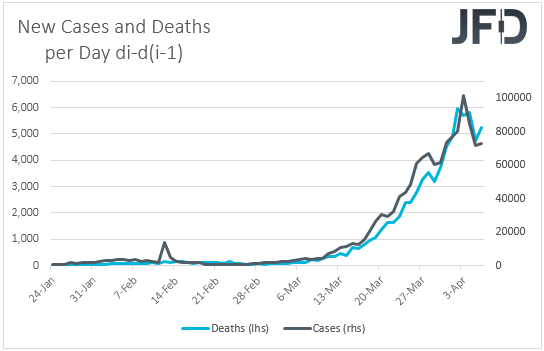

The catalyst behind the strong start of the week in equity markets may have been the slowdown in both infected cases and deaths from the fast spreading coronavirus. On Sunday, both new cases and deaths declined, with Italy, the nation with the highest death toll globally, reporting its lowest daily number of deaths in more than two weeks, while in Spain, the number of deaths slowed for the fourth consecutive day. With regards to the US, daily deaths in New York, the state hit the most, dropped as well, sparking hopes that the pandemic may have started leveling off. That said, Monday’s numbers were slightly higher than Sunday’s, resulting in some caution. That may have been the reason why Asian bourses today gained less than their EU and US counterparts did yesterday.

As for our view, it remains to be seen whether more slowdown is on the cards for the days to come. If we continue getting less and less cases day by day, equity markets may set the stage for a decent recovery. That said, another round of record numbers may be enough to turn things upside down again. This would mean that the worst is not behind us yet and that the economic wounds could still deepen and drag longer than previously anticipated. In any case, we believe that it is too early to call for a peak in the spreading of the coronavirus. Even if we have reached the peak, the lockdowns around the globe may be extended for a while more as governments may want to ensure that the virus has indeed been contained. And when we get a free movement permission, many people may be reluctant to get out of their homes. With that in mind, we believe that the global economy may start recovering well after the peak of the pandemic.

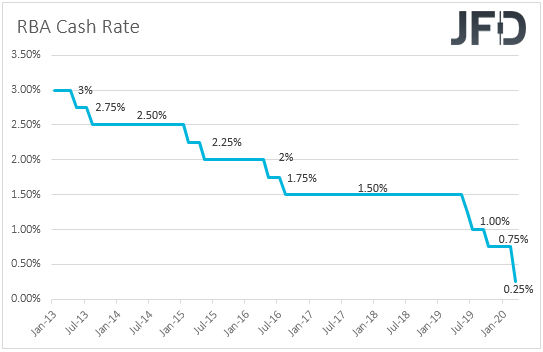

Besides headlines surrounding the virus saga, during the Asian session today, we also had an RBA monetary policy decision. Australian policymakers left monetary policy unchanged and offered some details with regards to their QE program. They noted that they will do what is necessary to achieve a 3-year yield target of 0.25%, with the target expected to remain in place until progress is being made towards the goals for full employment and inflation. However, they added that if conditions continue to improve, it is likely that smaller and less frequent purchases of government bonds will be required.

After saying that interest rates have reached their effective lower bound at their previous meeting, the aforementioned points suggest that there is very little chance of expanding their QE program. On the contrary, they could soon scale it back if the spreading of the coronavirus continues to level off. Maybe that’s why the Aussie was among the main G10 gainers. Apart from the risk-on trading, it may have received an extra boost from the less-dovish-than expected RBA. The Aussie could continue gaining for a while more if the spreading of the pandemic continues to slow, and may record the most gains against safe-haven currencies, like the yen, which tend to come under selling interest during periods of optimism.

Alongside the safe-havens, the pound was also on the back foot, losing ground after UK Prime Minister Boris Jonson was moved to intensive care due to worsening coronavirus symptoms. The PM was hospitalized on Sunday night due to persistent symptoms for more than ten days.

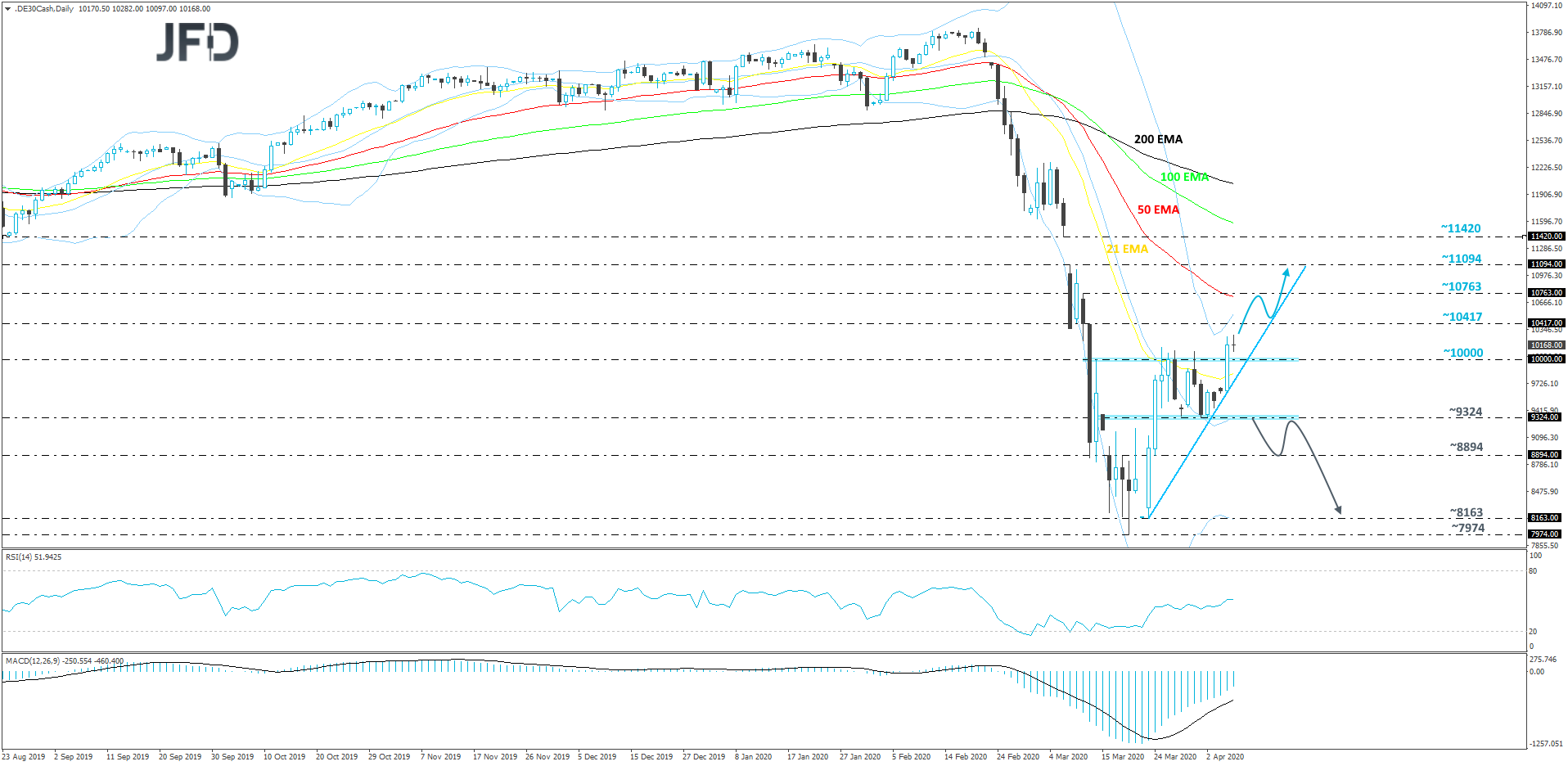

DAX – TECHNICAL OUTLOOK

We can see that DAX had recently violated and closed a daily candle above its key resistance barrier, at 10000. The index is now also trading above a newly-established short-term tentative upside support line drawn from the low of March 23rd. Given that there is a bit of positivity in the market, there is a possibility for the price to go for a larger correction to the upside, hence why we will take a cautiously-bullish stance for now.

Because DAX already closed a daily candle above the psychological 10000 barrier, we can now get a bit more comfortable with the examination of slightly higher areas. The bulls may push the price to the 10417 obstacle, a break of which could send the German index to the 10763 zone, marked by the high of March 11th. Initially, DAX could receive a hold-up there, or even correct a bit lower. That said, if it remains above the aforementioned upside line, and if the bulls are still feeling more comfortable, they might easily lift the price above the 10763 area and aim for the 11094 level, which is the high of March 9th.

On the downside, if the price breaks the previously-discussed upside line and then slides below the 9324 obstacle, which acted as a good support area from March 25th, this might spook the bulls from the field temporarily. DAX could slide to the 8894 area, which is the low of March 24th. The German index might rebound from there slightly, however if it struggles to move back above the 9324 barrier, this could result in another round of selling, potentially overcoming the 8894 zone and aiming for the 8163 level, marked by the low of March 23rd.

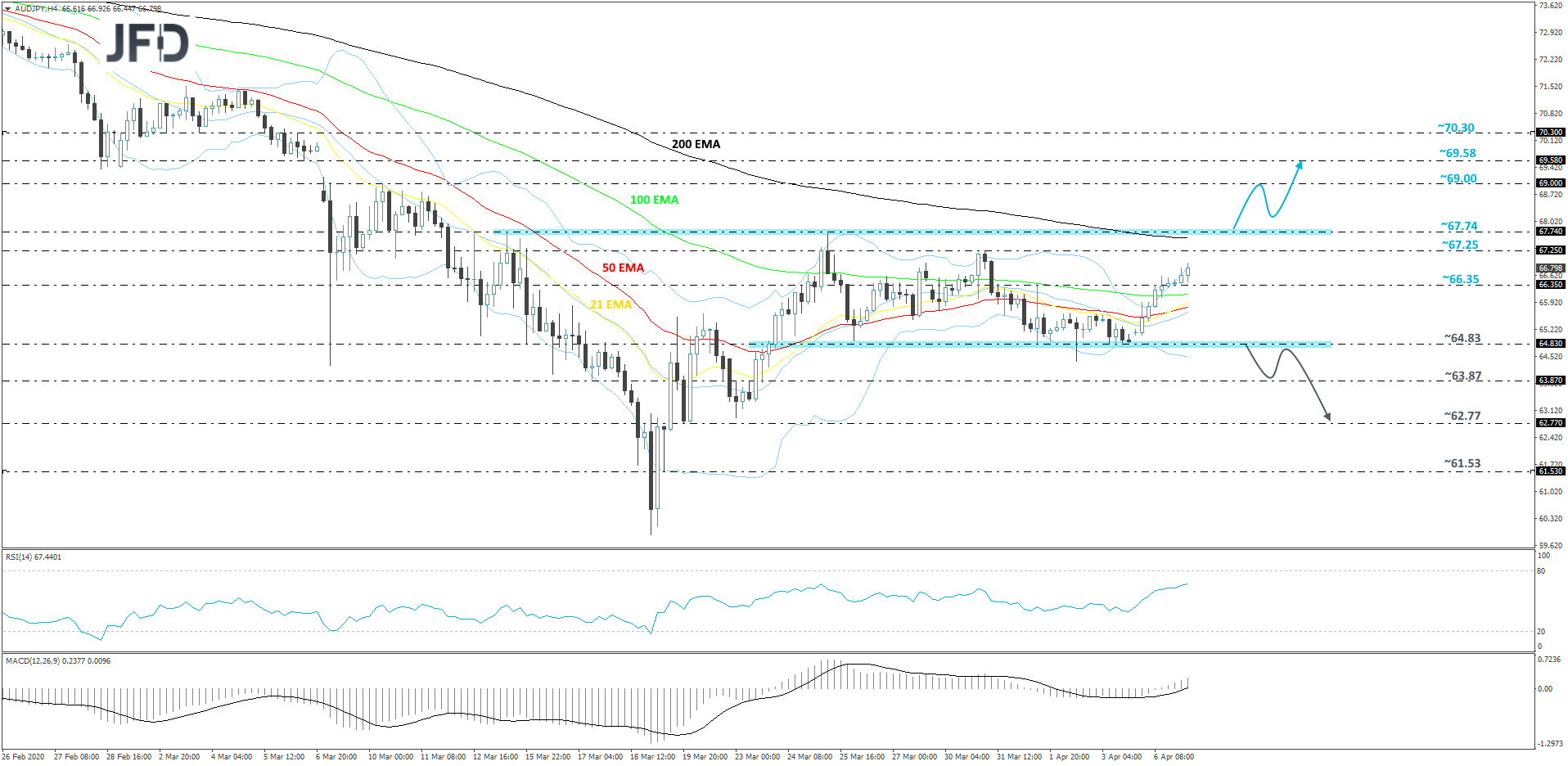

AUD/JPY – TECHNICAL OUTLOOK

AUD/JPY continues to move within a range, roughly between the 64.83 and 67.74 levels. Yesterday, the pair moved away from the lower side of that range and is now trying to make its way towards the upper bound. For now, we will take a neutral stance and wait for a break through one of the sides of that range, in order to consider a further directional move.

A break above the upper side of the range, at 67.74, would confirm a forthcoming higher high and also it would place the rate above the 200 EMA on the 4-hour chart. More buyers may see this as a good opportunity to step in and drive AUD/JPY further north. That’s when we will aim for the 69.00 hurdle, marked by the high of March 10th. The rate may stall there temporarily, however if the bulls are still feeling more comfortable, a break of that hurdle could send the pair to the 69.58 level, which is the low of March 6th.

In order to examine lower areas, we would first have to wait for a break of the lower side of the range, at 64.83. This way AUD/JPY could slide to the 63.87 obstacle, a break of which might put the 62.77 support level on the radar. That level marks an intraday swing low of March 19th.

AS FOR THE REST OF TODAY’S EVENTS

The US JOLTs job openings for February are coming out and they are expected to have declined somewhat, to 6.600mn from 6.963mn. Following the skyrocketing of the initial jobless claims for the week ended on March 27th to a new record of 6.65mn, investors may treat February’s job openings as outdated and wait for the March number, as during March the virus damages had been much more severe. From Canada, we get the Ivey PMI for March, which is expected to have declined to 41.0 from 54.1.

With regards to the energy market, we get the API (American Petroleum Institute) weekly report on crude oil inventories, but as it is always the case, no forecast is available.

Tonight, during the Asian session Wednesday, Japan’s current account balance for February is coming out, with the nation’s trade surplus expected to have increased to JPY 3.062 trillion from JPY 0.612 trillion.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Markets Trade In “Risk On” Fashion As Virus Spread Slows

Published 04/07/2020, 03:36 AM

Updated 07/09/2023, 06:31 AM

Markets Trade In “Risk On” Fashion As Virus Spread Slows

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.