Asian markets opened the new year in negative territory, as the MCSI index moved lower and emerging markets and high yielding currencies (particularly the South Korean won) weakened against the US Dollar. The market as a whole is lacking optimism about the potential prospects for the European debt crisis and this is leading the Euro Stoxx 50 futures to point to a lower open (down about 0.4 percent). Trading volumes remain thin and this will continue today with both Japan and the US observing holidays.

Most of the news headlines today are focusing in the face that most of the broad stocks and commodities indices posted their worst yearly performance since the 2008 financial crisis. Additional headlines were made by the South Korea and Singapore central banks which made negative comments about export growth and GDP revisions for 2011. Macro data today will come with Eurozone manufacturing data and this is expected to show declines for the fifth month in a row. Many of the European officials are still on holiday so they aren’t available to make positive comments and attempt to prop up the Euro and regional equities.

Yesterday, the Chinese manufacturing PMI showed a rise from 49 in November to 50.3 in December, which was higher than analyst expectations and we will see a similar report from the Eurozone today. A negative surprise will bring some buyers back into the US Dollar, which gained 1.5 percent last year as measured by the Dollar Index. In terms of US treasuries, gains of nearly 9.8 percent were seen for the year, which is also the biggest gain since the 2008 financial crisis.

For the most part volatilities are expected to remain light this week, but we could easily see this change on Thursday and Friday as some key macro data out of the US will be released. First, we will see the ISM report (expected to continue in its uptrend) and this will be followed by Construction Spending and then finally the Non Farm Payrolls figures on Friday. The NFP is expected to show a rise of 150,000 jobs for the month (after a gain of 120,000 previously). This report has the potential to move markets more than usual because of the low volume conditions that are currently in place and as most of the investment community slowly returns back to the trading floors.

EUR/USD CHART" title="EUR/USD CHART" width="672" height="318" />

EUR/USD CHART" title="EUR/USD CHART" width="672" height="318" />

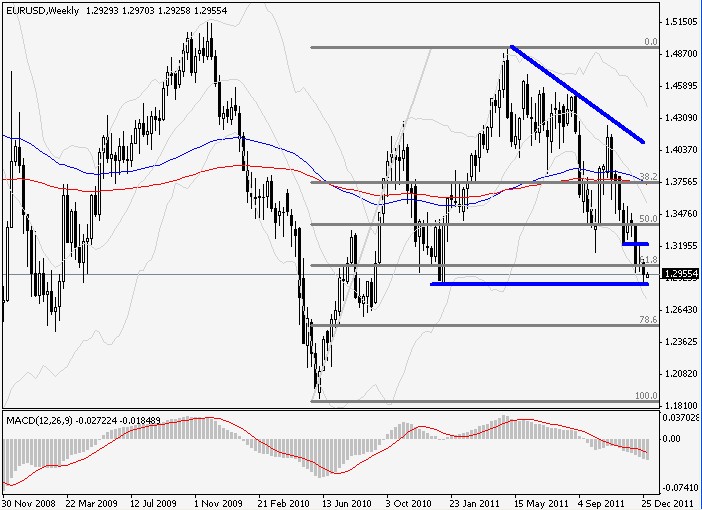

The EUR/USD continues to trade heavy and since we are dealing with longer term support levels, we will pull out to the weekly charts to get a sense of what is happening.We are seeing a slight bounce off of 1.2860 but follow through has been limited and the MACD indicator is venturing into negative territory, with plenty of room to extend. Short term, the first resistance comes in at 1.30 and this is the first sell zone.

The FTSE is still caught in its symmetrical triangle, after bouncing off of significant short term Fibonacci support at 5280. The bounce is encouraging and suggestive of additional upside breaks, so only a move back through 5280 will remove the bullish bias. First resistance comes in at 5560.

Most of the news headlines today are focusing in the face that most of the broad stocks and commodities indices posted their worst yearly performance since the 2008 financial crisis. Additional headlines were made by the South Korea and Singapore central banks which made negative comments about export growth and GDP revisions for 2011. Macro data today will come with Eurozone manufacturing data and this is expected to show declines for the fifth month in a row. Many of the European officials are still on holiday so they aren’t available to make positive comments and attempt to prop up the Euro and regional equities.

Yesterday, the Chinese manufacturing PMI showed a rise from 49 in November to 50.3 in December, which was higher than analyst expectations and we will see a similar report from the Eurozone today. A negative surprise will bring some buyers back into the US Dollar, which gained 1.5 percent last year as measured by the Dollar Index. In terms of US treasuries, gains of nearly 9.8 percent were seen for the year, which is also the biggest gain since the 2008 financial crisis.

For the most part volatilities are expected to remain light this week, but we could easily see this change on Thursday and Friday as some key macro data out of the US will be released. First, we will see the ISM report (expected to continue in its uptrend) and this will be followed by Construction Spending and then finally the Non Farm Payrolls figures on Friday. The NFP is expected to show a rise of 150,000 jobs for the month (after a gain of 120,000 previously). This report has the potential to move markets more than usual because of the low volume conditions that are currently in place and as most of the investment community slowly returns back to the trading floors.

EUR/USD CHART" title="EUR/USD CHART" width="672" height="318" />The EUR/USD continues to trade heavy and since we are dealing with longer term support levels, we will pull out to the weekly charts to get a sense of what is happening.We are seeing a slight bounce off of 1.2860 but follow through has been limited and the MACD indicator is venturing into negative territory, with plenty of room to extend. Short term, the first resistance comes in at 1.30 and this is the first sell zone.

The FTSE is still caught in its symmetrical triangle, after bouncing off of significant short term Fibonacci support at 5280. The bounce is encouraging and suggestive of additional upside breaks, so only a move back through 5280 will remove the bullish bias. First resistance comes in at 5560.