Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Equity markets traded in a risk-on fashion, yesterday, supported by Janet Yellen remarks over the weekend and by the falling coronavirus cases. The market sees the approval of the US stimulus package as a most likely thing, which could keep the positive sentiment for a while more.

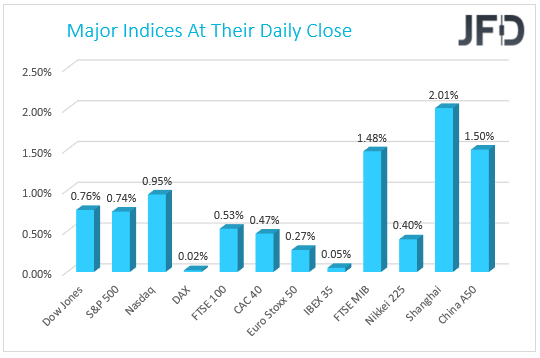

Yesterday, the equity markets rallied, with some major indices hitting fresh all-time highs. In the US, NASDAQ, Dow and the S&P 500, all hit record highs, while in Europe, DAX also went for a new historic high. However, the German index eventually declined and closed virtually unchanged for the day. The best performing index in Europe was the Italian FTSE MIB, gaining almost one-and-a-half percent. UK’s FTSE 100 also showed a good result, ending the session with around half of a percent gain. The upmove in the UK’s index might have been partially fuelled by the slightly weaker pound.

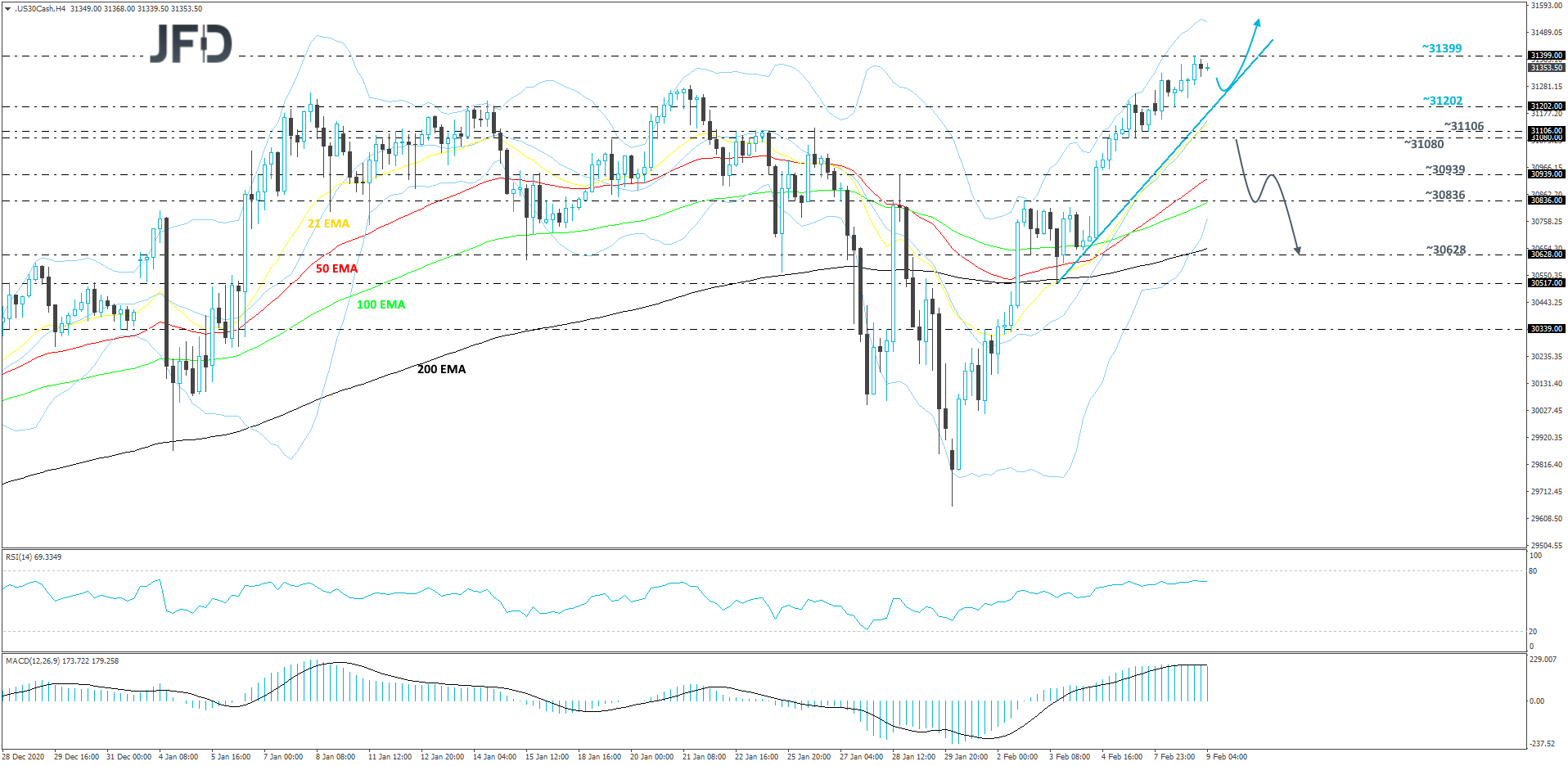

The DJIA index hit a new all-time high, yesterday, as risk-on environment prevailed. The cash index pushed further north, hitting the area near the 31399 level. The price remains on a steep upmove, while trading above a short-term tentative upside support line taken from the low of Feb. 3. Even if we see a retracement back down and the index stays above that upside line, we will remain positive, at least for now.

A small decline could bring the price back to the 31285 hurdle, marked by the highest point of January, or to the aforementioned upside line, which might provide support again. If so, DJIA could move back up, as more buyers might jump in. We will then aim for the current all-time high, at 31399, a break of which would place the price into the uncharted territory.

Alternatively, if the index breaks the aforementioned upside line and then falls below the 31080 hurdle, marked by an intraday swing low of Feb. 5, that may open the door for further declines. The bulls could get spooked from the field temporarily and the price may slide to the 30939 zone, or to the 30836 area, marked by the high of Feb. 2. If the selling continues, the next possible target might be at 30628, marked by an intraday swing low of Feb. 2.

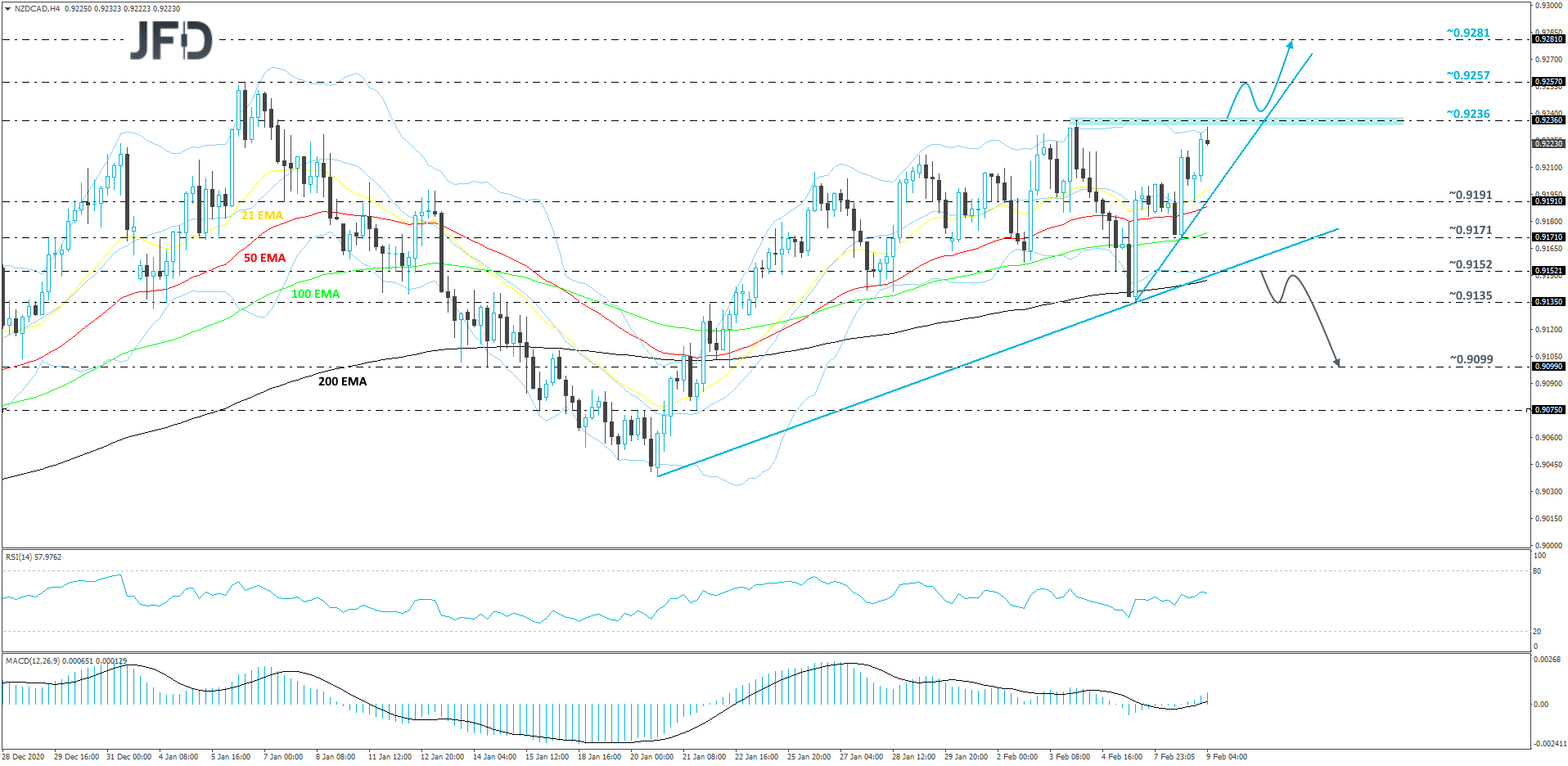

NZD/CAD continues to move higher, while trading above a couple of short-term tentative upside lines. One is drawn from the low of Jan. 20 and the other one (a slightly steeper one) is taken from the low of Feb. 5. Although the pair is showing signs that it may continue it,s journey north, in order to get comfortable with that idea, we would prefer to wait for a break above the current highest point of February, at 0.9236. Hence our somewhat bullish approach, for now.

A push above the 0.9236 barrier would confirm a forthcoming higher high, potentially inviting more buyers into the game. The pair could then rise to the 0.9257 obstacle, a break of which might clear the path for a move to the 0.9281 level. That level marks the highest point of March 2019.

In order to shift our attention to some lower areas, we would prefer to wait for a break of the aforementioned upside line, drawn from the low of Jan. 20. In addition to that, a rate-drop below the 0.9152 zone, marked by an intraday swing low of Feb. 5, could strengthen the bearish case, potentially opening the door to further declines. NZD/CAD may then travel to the current lowest point of February, at 0.9135, which might stall the slide temporarily. However, if the bears are still felling comfortable, they might push the rate further south, aiming for the 0.9099 level, marked by the low of Jan. 22.

Tuesday is a relatively quiet day in regards to economic indicators. The only worthwhile data set, which we will keep an eye on will be the Energy Information Administration’s (EIA) short-term energy outlook. Every month, EIA delivers its forecast on consumption, supply and prices in relation to oil-related products. Also, from the US, we will get the JOLTs job openings number for the month of December. Currently, the expectation is for the number to decline from 6.527M to 6.400M. If the actual number comes out lower than the forecast, this could be bad for the US dollar. However, we believe that USD may ignore the figure and instead, stay more vulnerable to the broader market sentiment.

The bad news is that the contraction in the money supply appears to be over. That’s not bad news per se (see below), but it’s bad in that the anti-inflationary work...

Tesla's (NASDAQ:TSLA) Q1 results didn’t look good at all. The revenue dropped 9% - the first revenue drop in four years - and net income plunged by 55% compared to the same...

The average 12-month trailing yield for the major asset classes has ticked up so far this year, based on a set of proxy ETFs through yesterday’s close (Apr. 23)...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.