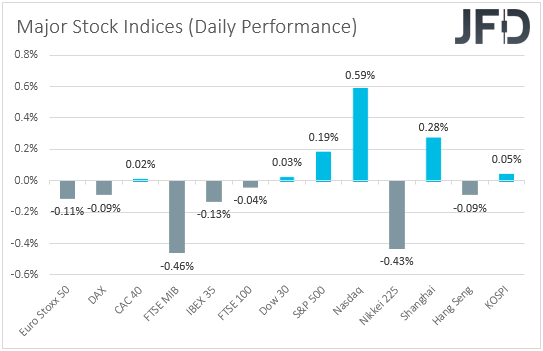

Most EU indices closed slightly in the red yesterday, and although Wall Street gained, risk appetite softened slightly again during the Asian session today. With no clear market drivers yesterday, it seems that market participants stayed relatively indecisive ahead of tomorrow’s release of the core PCE index, which is the Fed’s favorite inflation metric.

Equities Trade Mixed Ahead Of Friday's PCE Inflation Release

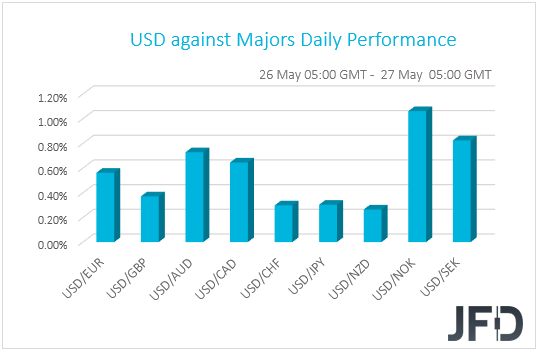

The US dollar rebounded and traded higher against all the other G10 currencies on Wednesday and during the Asian session Thursday. It gained the most versus NOK, SEK, AUD, CAD, and EUR in that order, while it eked out the least gains against NZD, JPY, and CHF.

The strengthening of the US dollar and the weakening of the commodity-linked Aussie and Loonie suggest that market participants switched to risk-off mode at some point yesterday. Although the strengthening of the Kiwi points otherwise, that was not due to developments surrounding the broader market sentiment, rather than the RBNZ’s optimism that the OCR may rise in the second half of 2022. Shifting attention to the equity world, we see that most major EU indices closed slightly lower, and while Wall Street ended higher, risk appetite softened slightly again during the Asian session today.

Once again, there was not a clear driver for the broader market sentiment. We stick to our guns that markets participants stayed relatively indecisive ahead of tomorrow’s release of the core PCE index, which is the Fed’s favorite inflation metric. Investors may have also been confused following remarks by Fed Board Governor Randal Quarles yesterday.

Following dovish comments by other officials, Quarles said that it will be important to begin discussing plans for adjusting QE at the upcoming meetings, but he also stressed the need to reman patient and that the time to discuss rate hikes is “far into the future”.

Quarles’s view is not as dovish as Fed Chair Powell’s and some other officials’ opinion, who believe that it’s still too early to even start discussing policy withdrawal, and that’s why many market participants may have been reluctant to confidently add to their risk exposure. Our focus now is what policymakers will have to say after tomorrow’s PCE data, the core yoy rate of which is expected to surge to +2.9% from +1.8%.

If several of them stick to their guns that the surge in inflation is likely to prove to be temporary and that it’s not the time to consider normalization yet, equities and other risk-linked assets are likely to rebound and continue trending north. However, the opposite may be true if more Fed policymakers start referring to a potential reduction of their QE purchases. For now, we prefer to step to the sidelines and wait for the picture to become clearer.

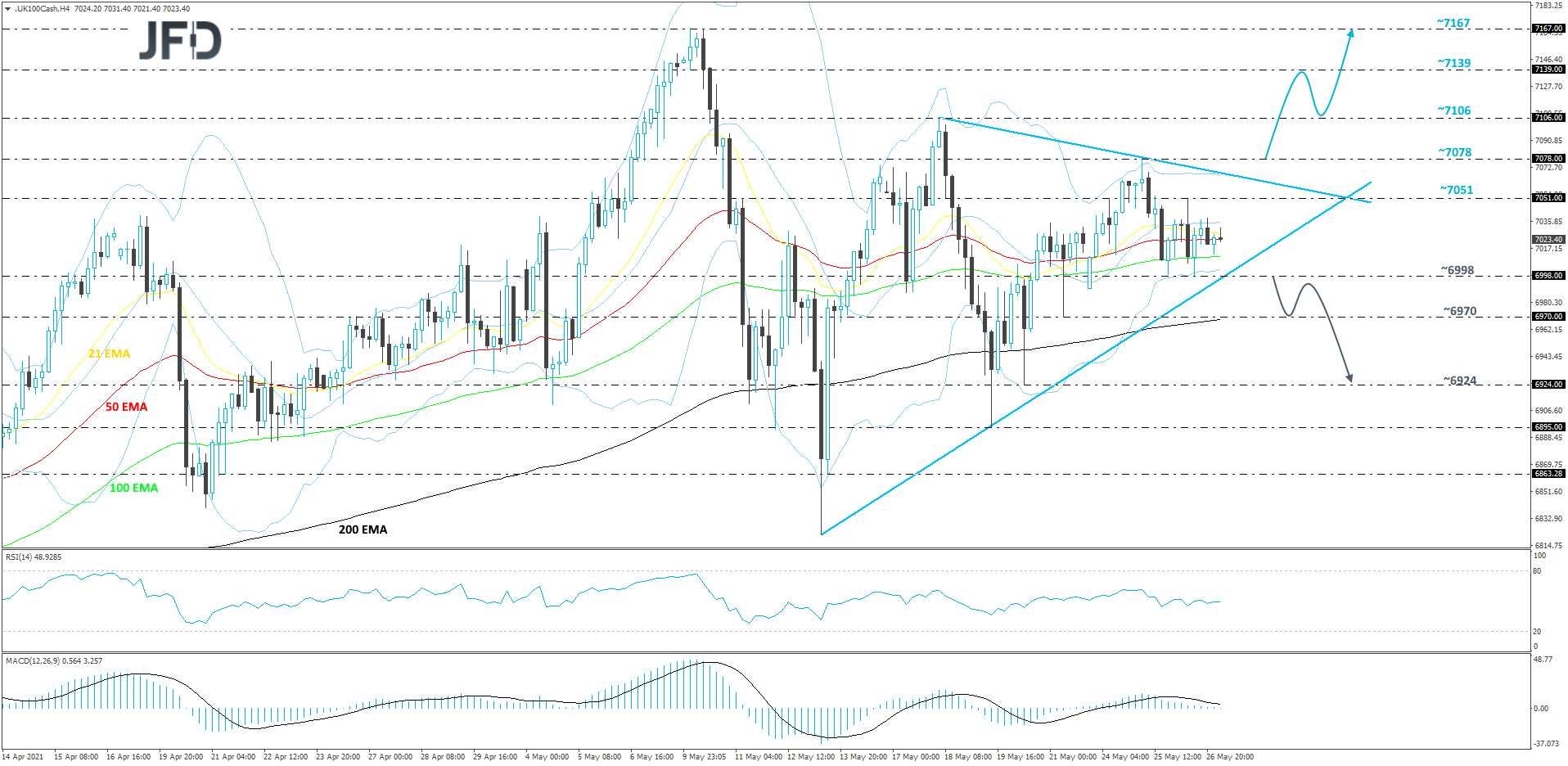

FTSE 100 Technical Outlook

Looking at the FTSE 100 cash index on our 4-hour chart, we can see that it is currently stuck between two of its short-term tentative lines, an upside one taken from the low of May 13 and a downside one drawn from the high of May 18. In order to consider the next short-term directional move, a break through one of those lines is needed.

If the price is able to rise above the aforementioned downside line and also above the 7078 barrier, marked by the current highest point of this week, such a move may attract more buyers into the game. The index could drift to the high of May 18, at 7106, or to the 7139 hurdle, which is an intraday swing low of May 10. If the buying doesn’t end there, FTSE 100 could be pushed to the 7167 level, marked near the highest point of May.

Alternatively, if the previously-discussed upside line breaks and the price falls below yesterday’s low, at 6998, this may attract more bears into the field, resulting in further declines for the index. FTSE 100 could then travel to the 6970 obstacle, a break of which might clear the way for a move to the 6924 level, marked by the low of May 20.

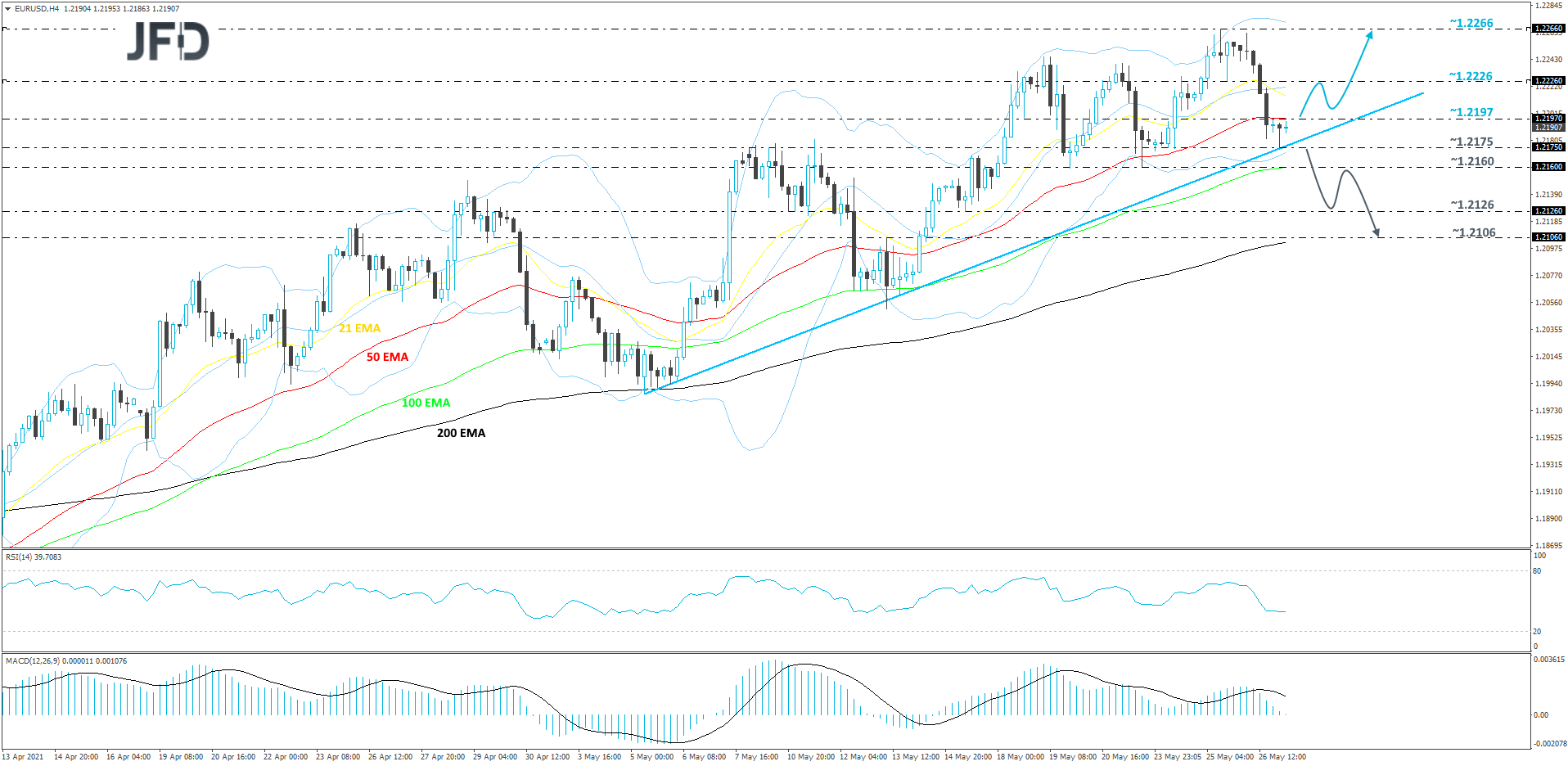

EUR/USD Technical Outlook

Yesterday, EUR/USD made its way lower, falling below the 21 and 50 EMAs on our 4-hour chart. However, the pair managed to stay above its short-term upside support line taken from the low of May 5th. As long as the rate continues to balance above that upside line, we will remain positive with the near-term outlook.

If the aforementioned upside line remains intact and the rate gets pushed back above the 1.2197 hurdle, marked by yesterday’s intraday swing high, this would also place the pair back above the 50 EMA and more buyers may join in. EUR/USD might travel to the 1.2226 obstacle, a break of which could place the 1.2266 level back on the table as the next potential target. That level marks the current highest point of May.

On the other hand, if the pair breaks the previously mentioned upside line and falls below the current low of today, that may temporarily spook the bulls from the field. EUR/USD might drift to the 1.2160 obstacle, a break of which may send the rate to the 1.2126 zone, marked by the low of May 17. The pair could receive a temporary hold-up around there, but if the bears are still feeling quite comfortable, they might push EUR/USD to its next possible support area, at 1.2106, marked by the inside swing high of May 13. Around there the rate may find additional support from the 200 EMA.

As For Today's Events

Today, we get the second estimate of the US GDP for Q1, which is expected reveal a small upside revision, to +6.5% qoq SAAR from +6.4%, as well as the durable goods orders for April. Both headline and core orders are expected to have slowed to +0.7% mom, from +1.0% and +2.3% respectively. Pending home sales for April and the initial jobless claims for last week are also coming out. Pending home sales are forecast to have slowed to +0.8% mom from +1.9%, while initial jobless claims are expected to have declined slightly, to 425k from 444k.

During the Asian session tomorrow, the Tokyo CPIs for May are due to be released, alongside Japan’s employment report for April. No forecast is available for the headline Tokyo CPI rate, while the core one is anticipated to have stayed unchanged at -0.2% yoy. The unemployment rate is expected to have ticked up to 2.7% from 2.6%, while the jobs-to-applications ratio is forecast to have held steady at 1.10.

As for the speakers, we have five on today’s agenda and those are ECB Vice President Luis de Guindos, ECB Governing Council member Jens Weidmann, ECB Executive Board member Isabel Schnabel, ECB Supervisory Board member Pentti Hakkarainen and BoE MPC member Gertjan Vlieghe.