Today, market participants may be sitting on the edge of their seats in anticipation of the US retail sales for October, where substantial numbers could add to speculation that the Fed could indeed start raising interest rates as soon as the tapering process is over. Tomorrow, during the early European morning, we get the UK CPIs, with further acceleration having the potential to fuel bets over a December hike by the Bank of England (BoE).

US Retail Sales Today and UK CPIs Early Tomorrow on the Agenda

The US dollar traded higher against all but one of the other major currencies on Monday and during the Asian morning Tuesday. It lost some ground only versus CAD, while the main losers were EUR and CHF.

The rebound in the US dollar used to be a sign of risk aversion. However, lately, signs of an improving US economy have pushed the currency up due to expectations of faster rate hikes. Still, they have also helped equities, as investors may have already digested the idea of higher rates soon in the US.

That said, this time around, although European indices marched higher, Wall Street closed virtually unchanged. Perhaps this was because investors took the sidelines ahead of today's retail sales. Now, in Asia today, the picture was mixed. Nikkei finished virtually flat, while China’s Shanghai Composite and South Korea’s KOSPI slid. Only Hong Kong's Hang Seng gained decently.

As we already noted, today, the highlight on the agenda may be the US retail sales for October. We also get the industrial and manufacturing production rates for the same month. Headline sales are forecast to accelerate to +1.1% MoM from +0.7%, while the core rate is expected to have held steady at +0.8% MoM. Industrial and manufacturing productions are expected to rebound 0.7% MoM and 0.8% MoM, after sliding 1.3% and 0.7% respectively.

In our view, the forecasts point to decent data, which following last week's acceleration in the US CPIs could increase bets over a hike by the Fed as soon as the tapering process is over. Remember that Fed Chair Powell said that they would stay "patient" on interest rates at the latest gathering, but he ruled out the likelihood of action just after tapering is over.

According to the Fed funds futures, investors are already pricing in a 25bps hike to be delivered in July next year, and another round of robust US data could add more credence to their view. This is likely to allow more dollar buying. Even if equities are correct somewhat lower, as we already noted, signs of further improvement in the US economy could allow for a rebound very soon.

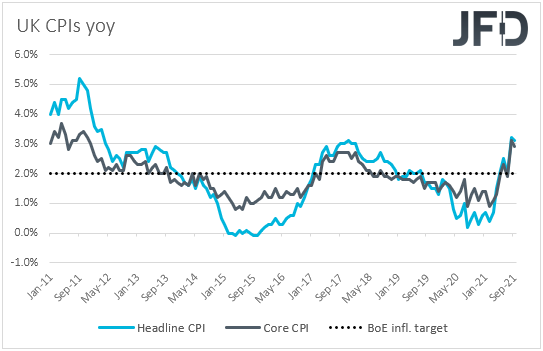

Now, flying from the US to the UK, tomorrow, during the early European session, we have the UK CPIs for October. Yes, we do get the UK employment report for September today. Still, we believe that GBP traders will pay more attention to the October CPIs as they try to understand how the Bank of England (BoE) will handle inflation and when the proper time for a hike will be.

Expectations are for the headline rate to jump to +3.9% YoY from +3.1%, while the core one is expected to rise to +3.1% YoY from +2.9%.

At its latest meeting, the BoE decided not to hike and instead said that this could happen in the "coming months," despite market participants assigning an 80% chance for such a move ahead of the meeting. Last Monday, the pound rebounded strongly, following remarks by BoE Governor Andrew Bailey. He said they are on a path towards raising interest rates, which may have sparked expectations over a December move.

However, on Thursday, the preliminary UK GDP for Q3 disappointed, slowing by more than expected. This may have forced market participants to push back their hike expectations, perhaps somewhere in the first months of next year. After all, February is also in the "coming months" spectrum.

Having said all that, though, strong acceleration in consumer prices will add more credence to Governor's Baily remarks and may revive speculation for a December hike, something that could prove positive for the pound.

The euro was the main loser among the majors, and this may have been due to remarks by European Central Bank (ECB President Christine Lagarde, who pushed back against interest rate hikes once again, saying that tightening monetary policy now to rein in inflation could choke off the euro zone's recovery.

Remember that she tried to push against hikes at the press conference following the latest ECB decision, but her attempt was unsuccessful. It seems that her persistence eventually got some participants having second thoughts, and that's why we saw the euro sliding.

With the ECB staying adamant that it is not the time to start raising rates and the Federal Reserve keeping the door open for higher rates as soon as next summer, we believe that this monetary policy divergence will keep the EUR/USD currency pair under selling interest.

EUR/USD – Technical Outlook

EUR/USD fell sharply yesterday, after it hit resistance at 1.1465, with the fall finding support at 1.1357. Overall, the pair remains well below the downside resistance line taken from the high of May 25, which paints a very negative picture, combined with the latest steep fall.

Even if the rate rebounds to recover some of its latest losses, we would see decent chances for the bears to retake charge from near the 1.1432 zone and aim for another test at 1.1357. If they manage to break lower this time around, we could see them pushing the action down towards the 1.1250 barrier, marked as a support by the low of Jul. 10.

On the upside, we would like to see a move back above the critical barrier of 1.1524 before we examine the case of a more significant upside correction. This could encourage some advances towards the 1.1575 zone, the break of which could pave the way towards the crossroads of the 1.1615 level and the aforementioned downside line taken from the high of May 25.

GBP/CHF – Technical Outlook

GBP/CHF traded higher on Monday to touch the upper bound of a sideways range that's been in place since Nov. 4. The upper bound is at 1.2423, while the lower one is at 1.2280. We can also say that the sideways activity looks like a double bottom formation, but we will start examining a bullish reversal upon a break above 1.2423. For now, we will stay neutral.

If we do see a break above 1.2423, this could signal the completion of the double bottom and encourage the bulls to push the action towards the 1.2487 hurdle, marked by the high of Nov. 4. If they are unwilling to stop there, we could see them marching towards the 1.2545 barrier, marked by the high of Nov. 1, or the peak of Oct. 29, at 1.2583.

On the downside, the picture could turn negative again, only if we see a dip below 1.2280. This would take the rate into territories last tested in February. The following support could be seen at 1.2207, marked by the inside swing high of Jan. 27, the break of which could allow extensions towards the low of Jan. 29, at 1.2147.

Elsewhere

During the Asian morning, we already got the minutes of the latest Reserve Bank of Australia (RBA) monetary policy meeting, which just confirmed that there would be no rate hikes until wage and inflation criteria are met. What's more, in a speech soon after the minutes were out, Governor Lowe said that underlying inflation at the mid-point of the RBA's range (2.5%) would not warrant a rate rise.

He added that underlying inflation needs to stay well within the 2-3% range and make them confident it will stay there. In our view, this enhances the narrative communicated at the latest meeting. That is, interest rates are unlikely to be touched next year.

Later in the day, and ahead of the US retail sales, we get the 2nd estimate of Eurozone's GDP for Q3, which is expected to confirm its preliminary print of 2.2%, as well as the bloc's employment change for the quarter, for which no forecast is available though. We already mentioned that we got the employment report for September from the UK, but we believe GBP traders will refrain from engaging in large positions ahead of tomorrow's CPIs.

As for the speakers, we will get to hear from ECB President Christine Lagarde again, as well as from Philadelphia Fed President Patrick Harker, San Francisco Fed President Mary Daly, Atlanta Fed President Raphael Bostic, and Richmond Fed President Thomas Barkin. It would be interesting to hear the Fed officials' views on when interest rates could start rising, especially if retail sales come in on the strong side.