Global equities traded higher yesterday and today in Asia, ahead of the US CPIs for June, which may well affect expectations over the Fed’s future course of action. Accelerating underlying inflation may bring hike bets forward, but market participants may get a clearer view on the Fed’s plans by Fed Chief Powell himself, who testifies before Congress on Wednesday and Thursday. Tonight, the spotlight is likely to fall on the RBNZ monetary policy decision. Given that, last week, a closely watched business confidence index jumped to its highest in four years, we see the case for a relatively optimistic language.

Will Rising US Inflation Increase Bets Over An Earlier Fed Tightening?

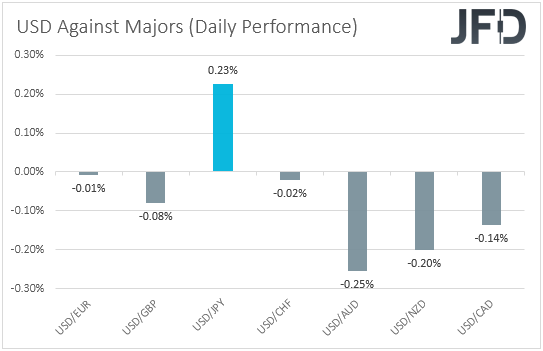

The US dollar traded mostly lower on Monday and during the Asian session Tuesday. It gained only against JPY, while it lost the most ground versus AUD, NZD, and CAD in that order.

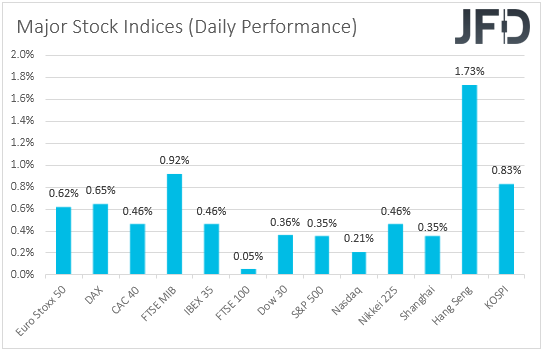

The weakening of the US dollar and the safe-haven yen, combined with the strengthening of the risk-linked Aussie, Kiwi and Loonie, suggests that markets may have traded in a risk-on fashion yesterday and today in Asia. Indeed, turning our gaze to the equity world, we see that major EU and US indices were a sea of green, with the German DAX, as well as Wall Street’s S&P 500 and NASDAQ, hitting fresh record highs. The optimism rolled over into the Asian session today as well, with Hong Kong’s Hang Seng gaining the most.

Although worries about the pace of the economic recovery remain elevated due to the fast spreading of the Covid Delta variant, evident by the slump in travel stocks, equities remained supported, perhaps due to investors increasing their risk exposure on defensive sectors. What’s more, concerns over a slowing global recovery could be translated into expectations that some major central banks may have to delay tightening plans in case the spreading of the coronavirus worsens. Paradoxically, this may have been a supportive factor for some equities, as it means lower borrowing costs for companies for longer, as well as higher discounted present values.

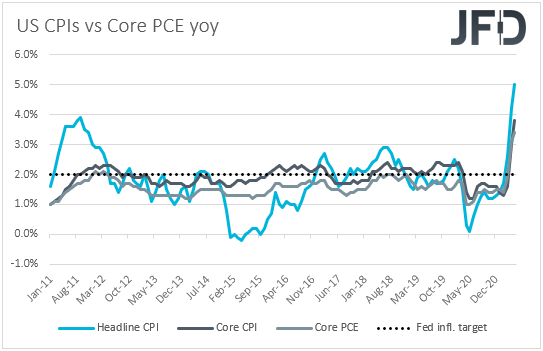

Today, market participants may lock their gaze on the US CPIs for June as they try to estimate when Fed officials are likely to push the rate-hike button. The headline rate is forecast to have ticked down to +4.9% yoy from +5.0%, while the core one is anticipated to have inched up to +4.0% yoy from +3.8%.

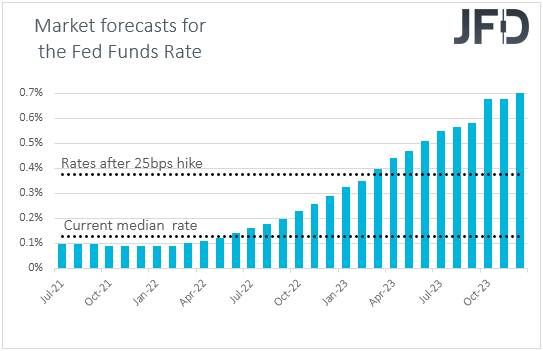

At its latest meeting, the FOMC kept its policy unchanged, but signaled that interest rates are likely to start rising in 2023. Since then, we’ve heard the individual views of several policymakers, with some of them supporting that interest rates should even start rising during 2022, and others arguing against withdrawing monetary policy support too soon. The divided Fed was also reflected in the minutes of the gathering, with various participants feeling that the conditions for reducing their asset purchases would be “met somewhat earlier than they had anticipated”, while others saw a less clear signal from incoming data and suggested a “patient” approach to any policy change. Overall though, they generally agreed that it is important to be well positioned to reduce the pace of asset purchases in case there is faster-than-anticipated progress towards the Committee’s goals.

In our view, a rising core CPI rate could add more credence to the view that the surge in inflation may eventually not be due to transitory factors and could increase expectations that the Fed may indeed start normalizing its monetary policy sooner than previously thought. According to the Fed Funds futures, market participants expect the first rate-hike to be delivered in March 2023, but a rising core CPI rate may bring that timing forth and thereby support the US dollar.

At the same time, equities are likely to correct lower, but we believe that the main focus for equity investors is likely to be second-quarter earnings, with big banks reporting this week. Today, we will get results from JPMorgan Chase (NYSE:JPM), Goldman Sachs (NYSE:GS), and Bank of America (NYSE:BAC).

Expectations are for a growth of 65.8% for companies in the S&P 500, up from a previous forecast of 54% at the start of the period. Solid earnings are likely to encourage more equity buying, and thus, we don’t expect a major pullback in stock indices in case data show that underlying inflation continued to accelerate in the US.

We believe that expectations around the Fed’s future course of action may be reflected more in the FX sphere. Even if so, the market’s response may still be relatively cautious as on Wednesday and Thursday, Fed Chief Jerome Powell will testify before Congress, and thus, investors and traders may get clearer hints with regards to the Fed’s plans directly from him.

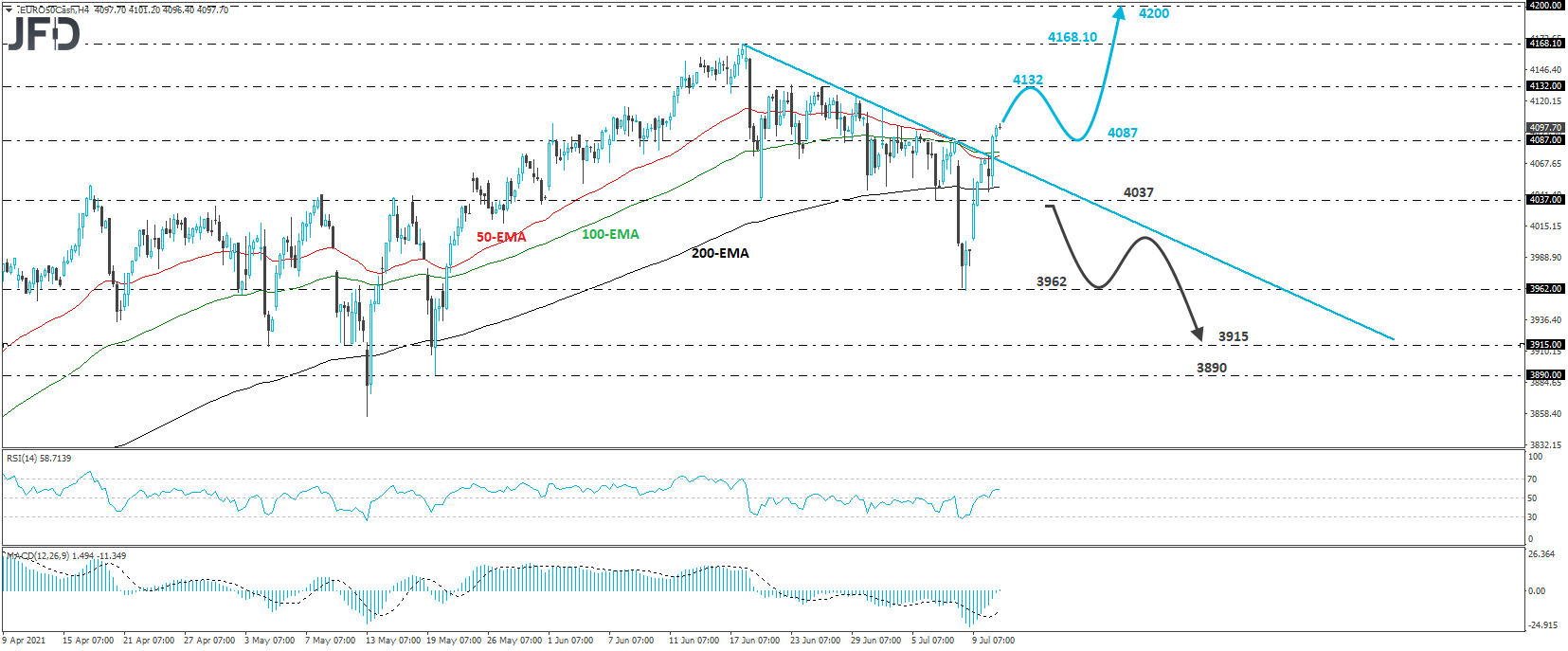

EURO STOXX 50 Technical Outlook

The Euro STOXX 50 cash index traded higher yesterday, breaking above the downside resistance line drawn from the high of June 17. What’s more, the rally took the index above last Wednesday’s high of 4087, thereby confirming a forthcoming higher high. In our view, yesterday’s jump has turned the technical picture back to positive, which means that further advances are likely.

Investors may decide to push the index higher, with the first obstacle on their way north perhaps being the 4132 zone, which provided decent resistance between June 22 and 25. If that area is not able to halt the advance this time around, market participants could target the all-time high of the index, at 4168.10, hit on June 17. A break higher would take the price into uncharted territory, and thus, we will mark as our next resistance the round-figure territory of 4200.

On the downside, we would like to see a retreat back below 4037 before we abandon the bullish case and star examining whether another round of selling could be possible. This would confirm the index’s return below the downside line drawn from the high of June 17, and may initially allow declines towards the 3962 support zone, defined by the low of July 8. Another break, below 3962, would confirm a forthcoming lower low and perhaps target the low of May 4, at around 3915.

RBNZ Likely To Sound More Optimistic

Tonight, during the Asian morning Wednesday, the spotlight is likely fall on the RBNZ, which decides on monetary policy. Although no policy action is expected, the tone of the accompanying statement may play a major role in shaping expectations over the Bank’s policy plans. Last week, market participants brought forth their bets over when this Bank will push the hike button, with 60% of New Zealand’s financial-sector firms expecting interest rates to rise over the coming year. This happened after a closely watched business confidence index jumped to its highest in four years.

With all that in mind, investors may dig into the statement for clues and hints on how optimistic policymakers are, and when they may be thinking to start raising rates. Although inflation remains below the midpoint of the Bank’s 1-3% target range, New Zealand has so far avoided a major outbreak of Covid’s Delta mutation, which may allow officials to be more optimistic than previously. This could support the Kiwi at the time of the announcement, but bearing in mind that FX traders’ sentiment may also be affected by expectations surrounding a potential Fed tightening, we don’t believe an upbeat RBNZ could prove the catalyst for a major bullish trend reversal in NZD/USD. It could just result in another small corrective bounce.

NZD/USD Technical Outlook

NZD/USD traded higher yesterday, but hit resistance near 0.7010 during the Asian session today, and it pulled back somewhat. Overall, since May 27, most of the price action has stayed below a downside resistance line, as well as below all three of our moving averages on the 4-hour chart. In our view, this paints a somewhat negative picture, and thus, we would see decent chances for the pair to drift lower.

However, in order to get confident on that front, we would like to see a clear dip below 0.6923, a hurdle that stopped the pair from moving lower on June 18 and July 9. Such a move would confirm a forthcoming lower low and perhaps encourage the bears to drive the battle towards the 0.6878 area, which provided support back on Nov. 17, 18, and 19. If they are not willing to stop there this time around, the next area to consider may be the low of Nov. 13, at 0.6810.

On the upside, a recovery above 0.7010 will also take the rate above the aforementioned downside line and may initially target the high of July 7, at 0.7062. A break above that barrier may extend the advance towards the 0.7105 zone, defined as a resistance by the high of the day before, but the move that would turn the picture to a more positive one is a break above that level. This will confirm a forthcoming higher high on the daily chart and could initially allow a test near the 0.7155 hurdle, which stopped the rate from moving higher between June 14 and 16.

As For The Rest Of Today's Events

During the early EU session, we already got Germany’s final CPIs for June, which just confirmed their preliminary estimates. Later in the day, after the US CPIs, the API report on crude oil inventories is coming out, but as it is always the case, no forecast is available.

As for the speakers, we do have one on today’s agenda and this is Atlanta Fed President Raphael Bostic.