Market sentiment remained largely supported due to the easing “stay at home” measures. In the currency world, the Aussie was among the main gainers following Australia’s better-than-expected CPIs. As for today, the spotlight is likely to turn to the FOMC decision and the 1st estimate of the US GDP for Q1.

RISK APPETITE REMAINS SUPPORTED, AUD GAINS AFTER CPIS

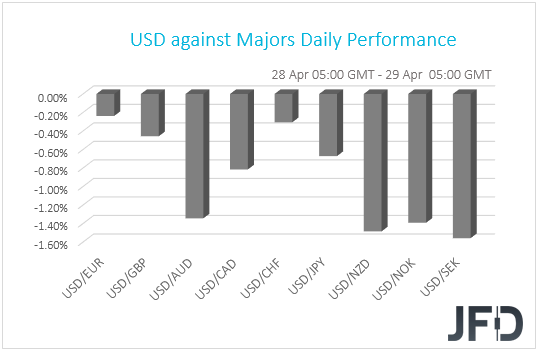

The dollar traded lower against all the other G10 currencies on Tuesday and during the Asian morning Wednesday. It lost the most ground against SEK, NZD, NOK and AUD in that order, while it underperformed the least versus JPY, GBP, CHF and EUR.

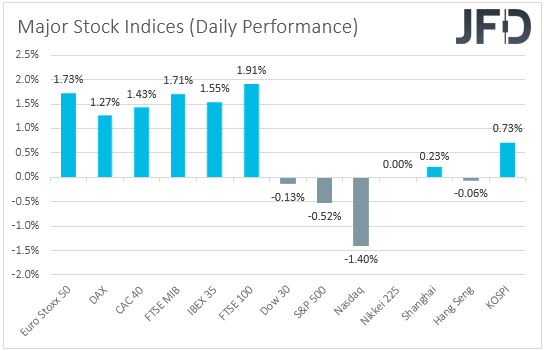

The weakening of the dollar and the strengthening of the commodity-linked currencies suggest that risk appetite may have remained supported for another day. Indeed, major EU indices were a sea of green, aided by a rally in banking shares following a 40% jump in UBS’s Q1 earnings and a 4.2% in Spain’s Santander (MC:SAN). It seems that expectations have fallen so much due to the uncertainty surrounding the coronavirus, that anything less bad than anticipated is seen as a positive. The optimism due to several economies starting to loosen restrictive measures may have also helped. Wall Street indices traded in the red, pulled by slides in technology stocks. That said, it seems that flows were diverted into economically sensitive value stocks, as they have the potential to benefit more by the easing of lockdown measures. Risk appetite rebounded again during the Asian session today. Although Hong Kong’s Hang Seng closed virtually unchanged, China’s Shanghai Composite and South Korea’s KOSPI gained 0.23% and 0.73% respectively. Japanese markets were closed.

Now (NYSE:DNOW), back to the currencies, SEK was the main gainer among the G10s, coming under strong buying interest after the Riksbank decided to continue its purchases of government and mortgage bonds up to the end of September 2020 and to leave the repo rate unchanged at 0%. Although officials noted that they cannot rule out the possibility of interest rates being cut at a later date, they added that it was not deemed justified at this point to try to increase demand by a cut, when the economic downturn is due to impose restrictions. The market reaction suggests that there may have been expectations for more stimulus today, but remember, yesterday we noted that this may not be the case, as following only a small downtick in the core CPIF rate, officials may prefer to stand pat and wait to see whether the already adopted measures are having the desired effects.

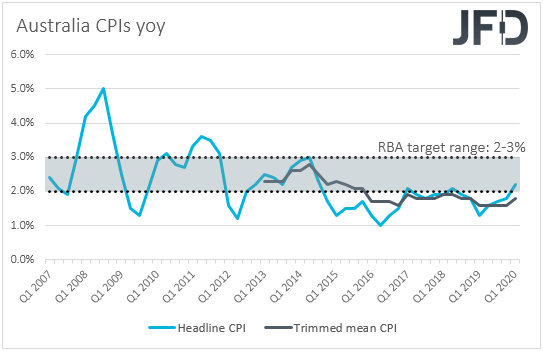

The Aussie was also among the main gainers, perhaps gaining extra ground after Australia’s better than expected CPIs for Q1. The headline rate moved to +2.2% yoy from +1.8%, above the lower end of the RBA’s target range, while the trimmed mean and weighted mean CPIs accelerated more than anticipated, to +1.8% and +1.7%, from +1.6% and +1.3% respectively.

When they last met, Australian policymakers left monetary policy unchanged and offered some details with regards to their QE program. They noted that they will do what is necessary to achieve a 3-year yield target of 0.25%, with the target expected to remain in place until progress is being made towards the goals for full employment and inflation. However, they added that if conditions continue to improve, it is likely that smaller and less frequent purchases of government bonds will be required.

After saying that interest rates have reached their effective lower bound at their prior meeting, the aforementioned points suggest that there is very little chance of expanding their QE program. On the contrary, they could soon scale it back if the spreading of the coronavirus continues to level off, and accelerating inflation is likely to make their work easier.

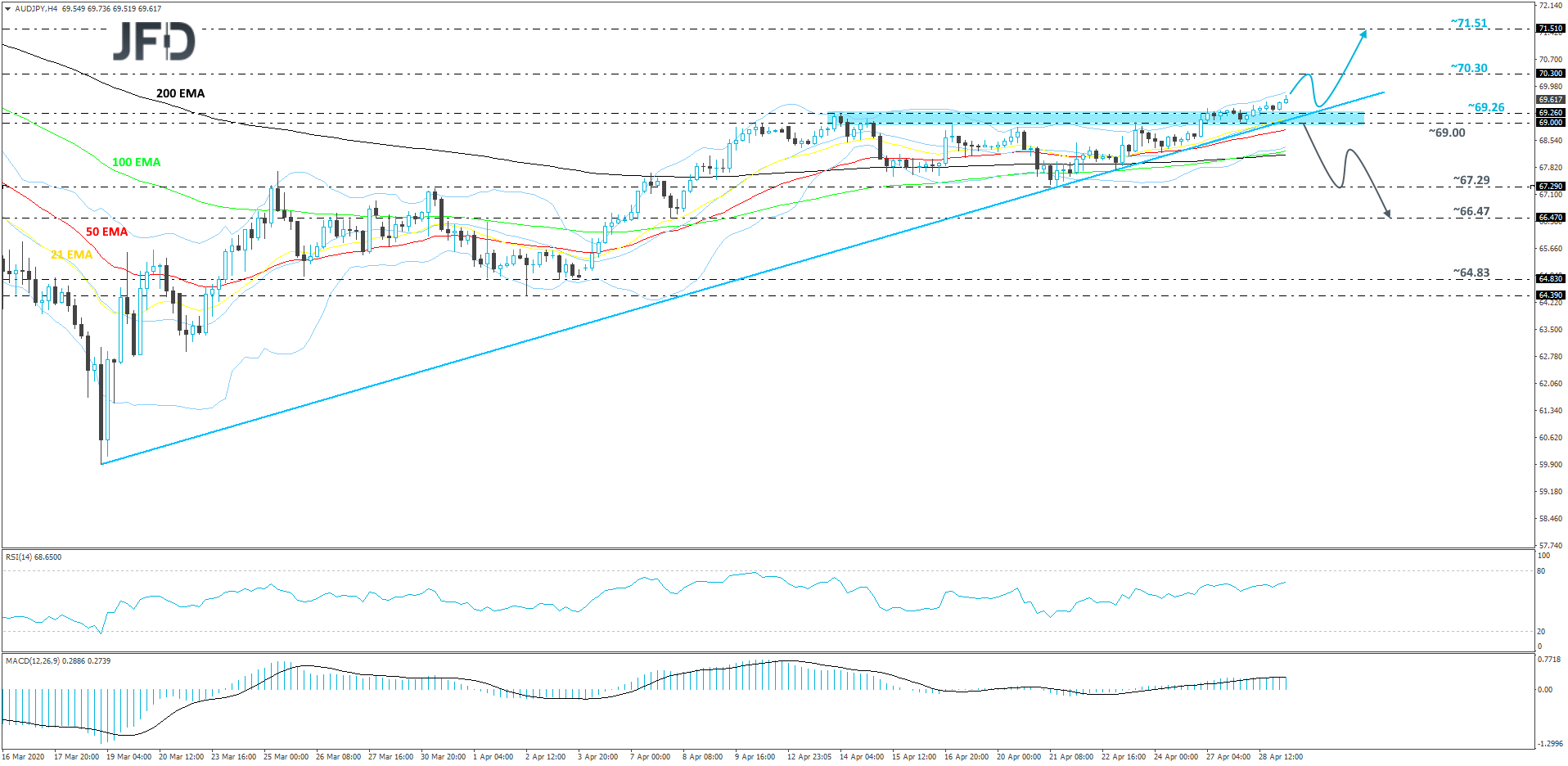

AUD/JPY – TECHNICAL OUTLOOK

AUD/JPY continues to gradually drift higher, while balancing above a short-term tentative upside support line drawn from the low of March 19th. This week, the pair managed to overcome its key resistance barrier, at 69.26, which was the previous highest point of April. As long as AUD/JPY stays above that upside line, we will remain on the positive side.

A further push north could bring the pair closer to the 70.30 barrier, which marks the low of March 3rd and an intraday swing high of March 6th. AUD/JPY could stall there for a bit, or even retrace back down slightly. That said, if the rate remains above the aforementioned upside line, the bulls may take charge again and lift the pair higher. If this time the 70.30 obstacle surrenders, the next potential resistance level to consider could be near the 71.51 area, marked by the high of March 3rd.

On the other hand, if the previously-mentioned upside line breaks and the rate falls below the 69.00 hurdle, which is the high of April 23rd and the low of yesterday, that may spook the bulls from the field temporarily and allow more bears to join in. However, we will still remain slightly cautious with the downside. For us to get slightly more comfortable with deeper extensions to the downside, AUD/JPY would have to drop below the 67.29 zone, which is the low of April 21st. The next possible support area to consider could be the low of April 8th, at 66.47.

FOMC AND US GDP DATA ENTER THE LIMELIGHT

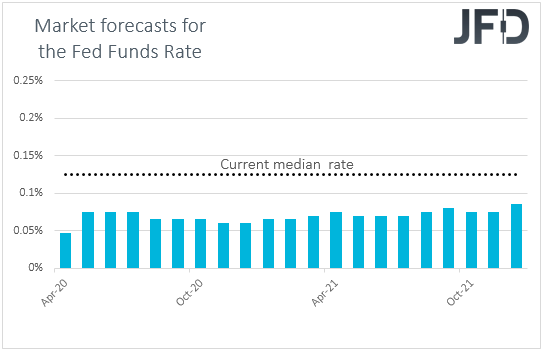

As for today, the spotlight is likely to turn to the FOMC decision, as well as to the 1st estimate of the US GDP for Q1. This would be the first ordinary meeting since January, after which the Committee decided to proceed with a number of simulative measures, including cutting rates to the 0-0.25% range and unlimited amounts of QE purchases, to support the US economy from the coronavirus damages.

On March 26th, Fed Chair Powell highlighted that the Fed is not going to run out of ammunition in its attempt to stimulate the economy, but since then they announced programs considered as a “never seen before” intervention into the US economy. The Committee announced that it will purchase corporate bonds, backstop direct loans to companies and that it will initiate a program to provide credit to small and medium-sized businesses. They also announced that they will purchase unlimited amounts of Treasuries and agency mortgage-backed securities in order to allow proper functioning of the US debt market. With the Fed never been in favor of the “negative rates” regime, all these measures make us believe that, now, there is little easing ammunition in the chamber and thus, policymakers may prefer to stand pat for now and wait for a while to see whether the already adopted measures are having the desired effect on the economy.

However, market participants may be sitting on the edge of their seats in anticipations of clues as to how long interest rates could stay near zero, and whether the Fed is willing to do more in the not-too-distant future in order to fight the virus. That said, with the situation easing somewhat lately, we don’t expect them to appear too much concerned. However, we don’t expect them to serve too much optimism either as the element of uncertainty remains. No one can guarantee that the virus will not start spreading fast again after the restrictions start to ease. Thus, they are unlikely to proceed with any language pointing to when interest rates may start being lifted, while they could still signal readiness to do more, but only if the situation worsens again.

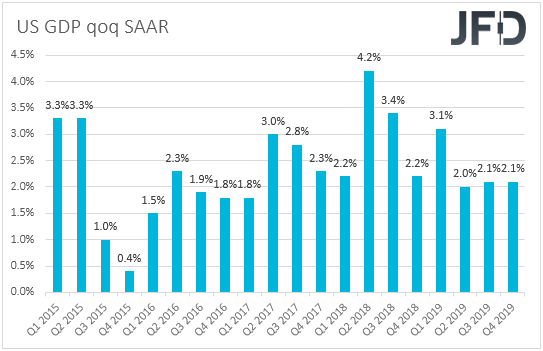

Such an outcome may result in a somewhat higher dollar, but the currency’s faith may also depend on the 1st estimate of the US GDP for Q1, due out ahead of the Fed decision. Expectations are for a 4.0% qoq SAAR contraction, after a 2.1% qoq SAAR expansion in the last three months of 2019. A shrinking US economy would be a surprise to no one, given the fast spreading of the coronavirus in the US during the last month of the quarter. That said, it would be interesting to see how deep the wounds have been. According to the Atlanta GDPNow and the New York Nowcast models, the economy contracted only 0.3% and 0.4% respectively, something that shifts the risks of the official forecast to the upside. A better-than-expected print may give an initial boost to the dollar before the Fed decision.

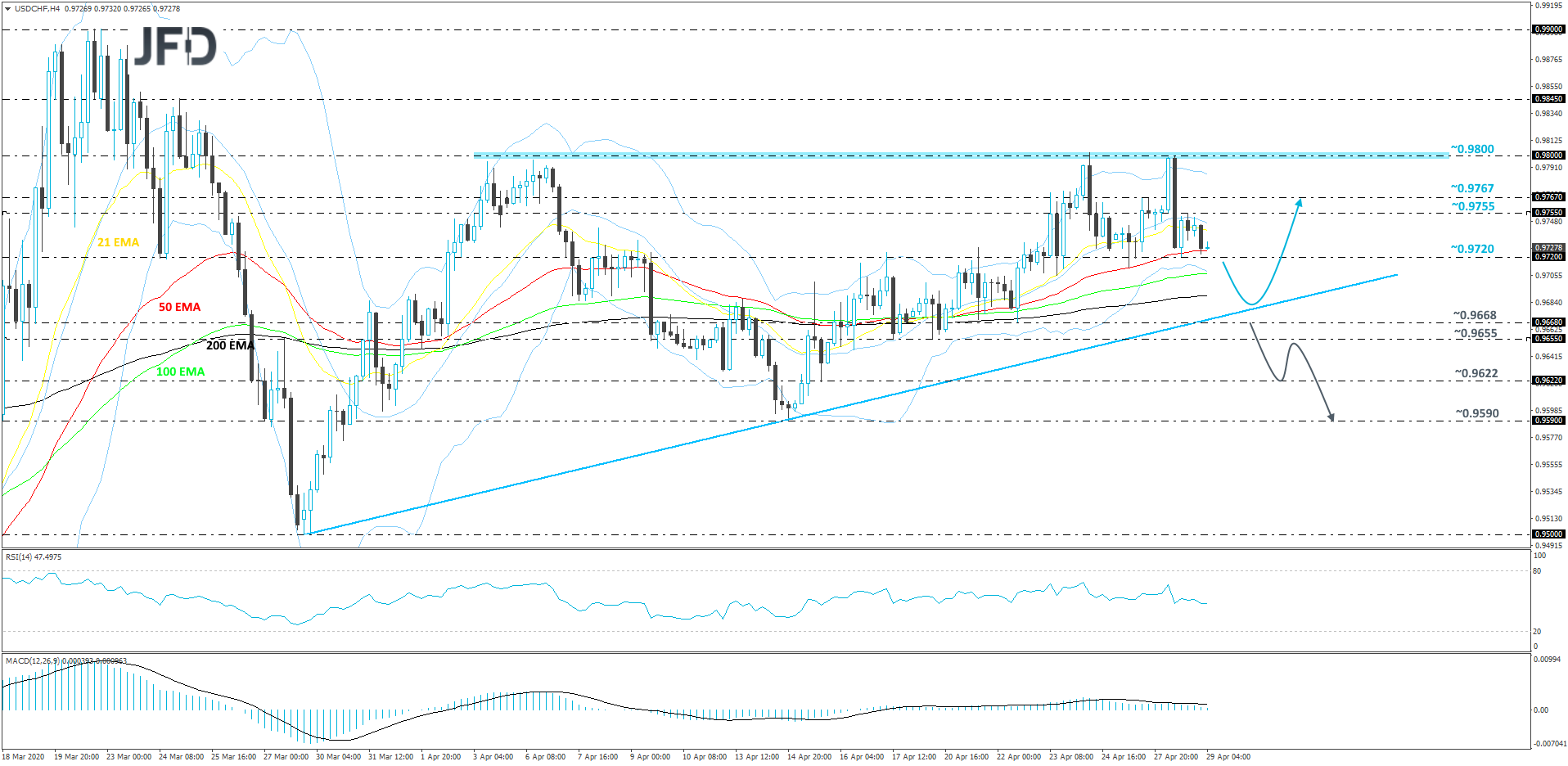

USD/CHF – TECHNICAL OUTLOOK

Once again, USD/CHF got held near the 0.9800 barrier and retraced back down. From around the beginning of April that hurdle continues to provide strong resistance for the pair, which is not allowing the rate to go for a higher high. On the positive side, USD/CHF remains above its short-term tentative upside support line taken from the low of March 29th. Although we may see a bit more downside in the near term, if that upside line stays intact, this could help the rate to rebound, hence why we will take a very cautiously-bullish stance overall.

If the pair slides below the 0.9720 support zone, which is marked near an intraday swing low of April 27th and the low of April 28th, this may clear the path to some lower areas. We will then examine a possible test of the aforementioned upside line, which if stays intact, could provide good support and allow USD/CHF to rebound. If so, the pair could travel back to the 0.9720 hurdle, a break of which might set the stage for a move to the 0.9755 obstacle, marked by an intraday swing high of April 28th. Slightly above it lies another possible resistance level, at 0.9767, which s the high of April 27th.

Alternatively, if the previously discussed upside line breaks and the rate slides below the 0.9668 zone, which is marked near the lows of April 21st and 22nd, this could attract more sellers into the arena. The pair might then drift to the 0.9655 obstacle, a break of which could open the door for a move to the 0.9622 area, marked by an intraday swing low of April 15th. Initially, USD/CHF may stall around there for a bit, but if the bears are still feeling a bit more comfortable, a break of that area might push the rate to the 0.9590 level, marked near the lowest point of April.

AS FOR THE REST OF TODAY’S EVENTS

During the European morning, Germany’s preliminary CPIs for April are coming out. Both the CPI and HICP rates are forecast to have slid notably, to +0.5% yoy and +0.6% yoy from +1.4% and +1.3% respectively. This would raise speculation that the headline rate for the Eurozone as a whole, due out on Thursday, may follow suit.

From the US, apart from the FOMC decision and the GDP data, we also get pending home sales for March and the EIA (Energy Information Administration) weekly report on crude oil inventories. Pending home sales are expected to have slid 10.0% after rising 2.4% in February, while the EIA report is expected to reveal a 10.619mn inventory increase, following a build of 15.022mn.

As for tonight, during the Asian session Thursday, we get Japan’s preliminary industrial production and retail sales, both for March. Industrial production is anticipated to have declined 5.2% mom after sliding 0.3% in February, while retail sales are forecast to have fallen 4.7% after rising 1.6%. China’s official PMIs for April are also coming out, but no forecast is currently available. Following the slowdown and the stabilization of the coronavirus in China since March, we wouldn’t be surprised if the PMIs reveal another month of expansion in both the manufacturing and services sectors.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Investors Lock Gaze On FOMC and U.S. GDP

Published 04/29/2020, 04:00 AM

Updated 07/09/2023, 06:31 AM

Investors Lock Gaze On FOMC and U.S. GDP

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.