Inflation is not coming. It is already here! Gold should benefit, given that it could be higher and more lasting than the pundits believe.

“Knock, knock, knockin’ on heaven’s door,” so sing Bob Dylan and Guns N’ Roses. Now, inflation is knocking on the golden door. According to the BLS, the U.S. CPI inflation rate recorded a monthly jump of 0.6% in March, while soaring 2.6% on an annual basis. And the core inflation has also accelerated. So, inflation has significantly surpassed the Fed’s target of 2%, as one can see in the chart below.

And remember that this is what the official data shows, which rather underestimates the true inflation. This is because of several issues, including hedonic quality adjustments, shifts in the composition of the consumer baskets and methodological changes. It is enough to say that the rate of inflation calculated by the John Williams’ Shadow Government Statistics that uses methodology from the 1980s is over 10% right now.

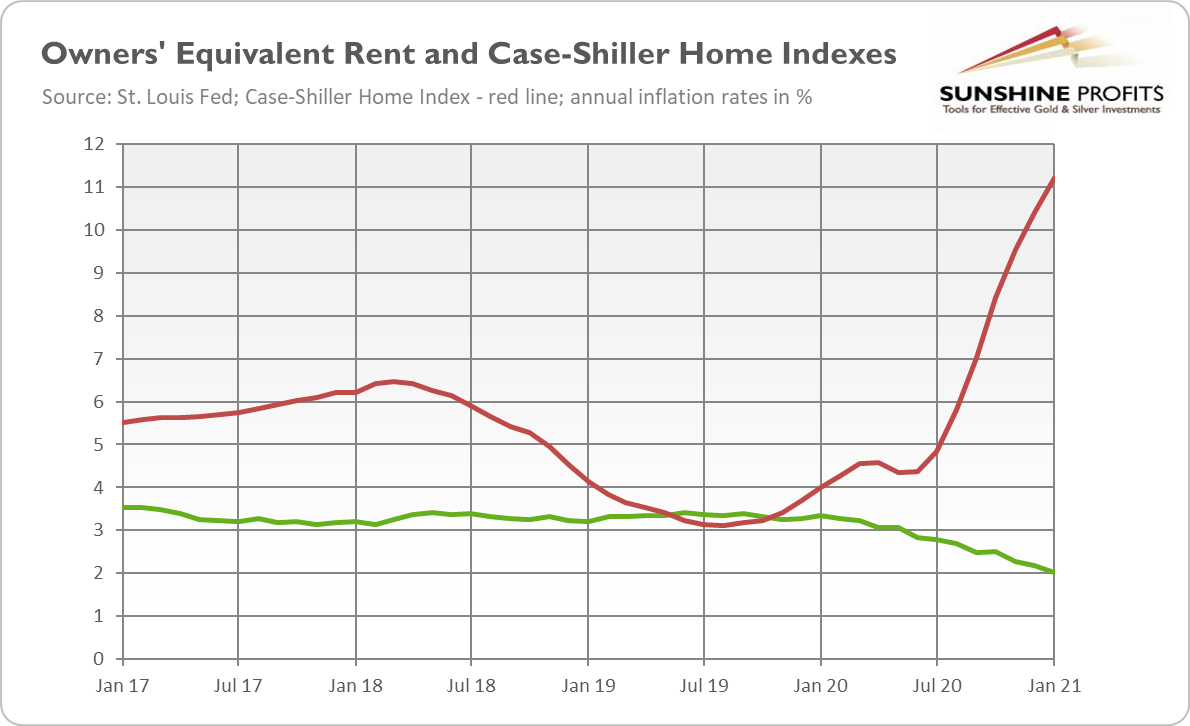

There are some controversies about this alternate data, but I would like to focus on something else. The CPI doesn’t include houses (or other assets) into the consumer baskets, as they are treated as investments. The index only takes rents into account. But homeowners don’t pay rents, so for them, the cost of shelter, which accounts for about one-fourth of the overall CPI, is the implicit rent that owner-occupants would have to pay if they were renting their homes. And this component rose just 2% in March, while the Case-Shiller Home Price Index, which measures the actual house prices, soared more than 11% in January (the latest available data). According to Wolf Street, if we had replaced the owners’ equivalent rent of primary residence with the Case-Shiller Index, the CPI would have jumped 5.1 instead of 2.6%. The chart below shows the difference between these two measures.

Hence, inflation has come, and even the official data – which can underestimate the level of inflation that ordinary people deal with in their daily lives – confirms this. If you’ve been buying food lately, you know what I mean. Now, the question is whether this inflation will be temporary or more lasting.

Powell, his colleagues and the pundits claim that higher inflation will only be a temporary phenomenon caused by the base effect. The story goes like this: the CPI plunged in March 2020, which created a lower base for today’s annual inflation rate. There is, of course, a grain of truth here. But let’s take a look at the chart below. It shows the CPI, with both March 2020 (red line) and February 2020 (green line) as a base. As you can see, in the latter case the index jumped 2.3%. Yes, lower, but not significantly lower than 2.6% when compared to March 2020. So, the Fed shouldn’t blame the base effects for accelerating inflation (and funny thing: have you heard the pundits talking about the base effect when they were talking about vigorous GDP recovery?).

Instead, central bankers should blame themselves and their insane monetary policy. After all, as the chart below shows, the Fed’s balance sheet has soared $3.4 trillion (or 81%), while the broad money supply (measured by M2) has increased more than $4 trillion (or 26%) from February to date.

They could also blame reckless fiscal policy. Growing government spending, enabled by a rising pile of debts monetized indirectly by the Fed, has headed for Main Street. This, combined with a jump in the broad money supply, is the key change compared to the Great Recession when almost all stimuli flowed into Wall Street and big corporations. Sure, some people use the received money to increase savings and repay debts. But with the reopening economy, some of the pent-up demand will be realized. Actually, many Americans have already started spending free time traveling like crazy after being locked in homes for so long.

And this is very important: consumers are therefore more eager to accept higher prices. It shouldn’t be surprising given all the checks they got and how hungry for normal life they are. As I reported last month, companies are reporting rising prices of commodities and inputs (partially because of the supply disruptions too), but so far their power to pass the producer price inflation to consumers has been limited. However, this is changing. The April report IHS Markit U.S. Services PMI observes:

Rates of input cost and output charge inflation reached fresh record peaks, as firms sought to pass on steep rises in input prices to clients (…) A number of companies also stated that stronger client demand allowed a greater proportion of the hike in costs to be passed through. The resulting rate of charge inflation was the quickest on record.

All these reasons suggest that higher inflation could be more lasting than most of the so-called experts believe (although the officially reported inflation doesn’t have to show it). This is good news for the yellow metal. Higher inflation implies lower real interest rates and stronger demand for gold as an inflation hedge . What is important here is that we have more inflationary pressure in the pipeline exactly at the time when the Fed has become more tolerant of inflation. So, the combination of higher inflation with a passive central bank position sounds bullish for gold. The key issue here is whether the markets believe that the Fed will allow for higher inflation. So far, they have been skeptical, so the expectations of interest rates hikes accumulated and the bond yields rallied. But it seems that the Fed has managed to convince the markets that it’s even more incompetent than it is widely believed. If the distrust in the Fed strengthens, gold should return to its upward trajectory from the last year.