The Hershey Company (NYSE:HSY) HSY is gaining on higher demand for its products amid sustained at-home consumption trend as well as recovery in away-from-home consumption. The company has been undertaking prudent buyouts to augment portfolio strength as well as boost revenues. Its strong brand portfolio and focus on innovation are yielding, though high costs are a concern.

Let’s delve deeper.

Solid Performance & Raised Sales View

Hershey has been benefiting from impressive recovery in away-from-home consumption and international markets. Sustained at-home consumption is also driving growth. These were reflected in the company’s second-quarter 2021 results, with the top and the bottom line surpassing the Zacks Consensus Estimate as well as increasing year over year. Volumes contributed 14.5 point to net sales growth.

On solid second-quarter performance and expected gains from the Lily's Sweets, LLC (Lily's) buyout, the company updated its 2021 net sales outlook upward. Hershey now expects 2021 net sales to increase 6-8%. Earlier, management had guided for net sales growth of 4-6%. The revised outlook takes into account better-than-anticipated recovery in the away-from-home business as well as international markets. The company reiterated its adjusted earnings per share outlook, which is expected in the range of $6.79-$6.92. The projection suggests growth of 8-10% year over year. Management highlighted that gains from higher sales is likely to be countered by incremental tax reserves and greater supply chain costs.

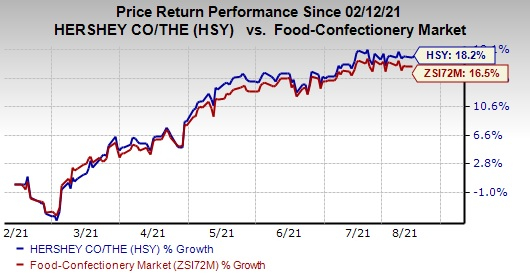

Image Source: Zacks Investment Research

What Else is Driving Growth?

Hershey made several strategic acquisitions to enhance its brand portfolio. On Jun 25, 2021 Hershey concluded the acquisition of Lily's, a leading better-for-you (BFY) confectionery brand. The buyout is in sync with Hershey’s focus on creating an impressive BFY confection portfolio as part of its multi-pronged better-for-you snacking strategy. Expected gains from this buyout were also one of the factors that encouraged management to raise sales view for 2021. In fact, the net impact of acquisitions and divestitures is expected to boost net sales by 0.7 point in 2021.

The company acquired ONE Brands, LLC in September 2019 to solidify its footing in the snacking category. Hershey acquired Pirate Brands in October 2018 to bolster its snacking business. Additionally, the company is gaining from Amplify Snack Brands, which was acquired in January 2018, to expand in the snacking category. During its last earnings call, management highlighted that its Pirate’s Booty and ONE nutrition bar brands increased significantly. The company saw robust rebound in ONE nutrition bars, with retail sales increasing 18% in the last 12 weeks.

Hershey’s core brands — Hershey’s, Reese’s, Hershey’s Kisses, Jolly Rancher, Brookside, Sofit and Ice Breakers — have been growing strongly on the back of advertising investments, in-store merchandising as well as programming and innovation. The company regularly brings innovation to its core brands to meet consumer demand and needs that are not addressed by its current portfolio. Also, the company is committed toward supporting its brands through solid media marketing.

Cost Headwind

Hershey is grappling with higher selling, marketing and administrative expenses for a while. During second-quarter 2021, the metric increased 14.3% year over year mainly due to higher corporate expenses. Advertising and related consumer marketing expenses increased 9.9% thanks to reactivation of important sponsorships in the North America segment. Also, higher investment in core brands in the International & Other unit caused the downside. Selling, marketing and administrative expenses, excluding advertising and related consumer marketing, rose 16.6% due to high incentive compensation accruals, more capability investments and medical claims. Management, in its last earnings call, highlighted that it expects to see increased packaging and freight costs as well as escalated labor expenses in the second half of the year.

Nevertheless, we believe that the aforementioned upsides are likely to help this Zacks Rank #3 (Hold) company stay afloat amid such hurdles. Hershey’s stock has gained 18.2% in the past six months compared with the industry’s growth of 16.5%.

3 Key Food Bets

Pilgrim’s Pride Corporation PPC currently carrying a Zacks Rank #2 (Buy), has a trailing four-quarter earnings surprise of 34%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Darling Ingredients (NYSE:DAR) Inc. DAR, currently carrying a Zacks Rank #2, has a trailing four-quarter earnings surprise of 29.8%, on average.

Hormel Foods Corporation (NYSE:HRL) HRL, currently carrying a Zacks Rank #2, has a trailing four-quarter earnings surprise of 3.1%, on average.

Breakout Biotech Stocks with Triple-Digit Profit Potential

The biotech sector is projected to surge beyond $775 billion by 2024 as scientists develop treatments for thousands of diseases. They’re also finding ways to edit the human genome to literally erase our vulnerability to these diseases.

Zacks has just released Century of Biology: 7 Biotech Stocks to Buy Right Now to help investors profit from 7 stocks poised for outperformance. Our recent biotech recommendations have produced gains of +50%, +83% and +164% in as little as 2 months. The stocks in this report could perform even better.

See these 7 breakthrough stocks now>>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hershey Company The (HSY): Free Stock Analysis Report

Hormel Foods Corporation (HRL): Free Stock Analysis Report

Darling Ingredients Inc. (DAR): Free Stock Analysis Report

Pilgrims Pride Corporation (PPC): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research