We believe that Daqo New Energy Corporation (NYSE:DQ) is a solid choice for investors seeking exposure in the chemical space. Anticipated rise in solar PV installations in various countries as well as the company’s initiatives to enhance production capabilities at polysilicon facilities bode well.

The stock has been upgraded to a Zacks Rank #1 (Strong Buy) on Nov 18.

Why the Upgrade?

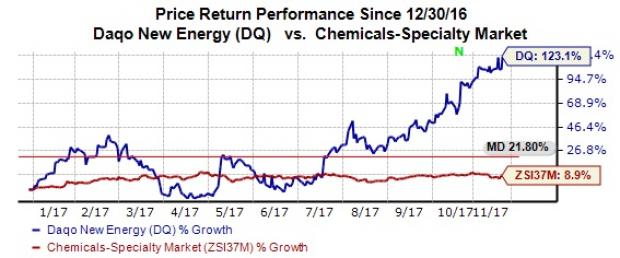

Daqo New Energy has performed well in two of three reported quarters. Year to date, the company’s American Depository Shares have rallied 123.1%, substantially outperforming 8.9% gain of the industry. Notably, in third-quarter 2017 results, it pulled off a positive earnings surprise of 62.07%.

The company’s revenues grew 64.6% year over year on the back of solid customer demand for polysilicon products. As noted, polysilicon sales volume in the quarter totaled 4,500 MT, increasing 58.6% year over year. Gross profit surged 70.8% while margin came in at 41.3% versus 39.9% in the year-ago quarter.

In the quarters ahead, we believe that Daqo New Energy will gain traction from the maintenance works that it completed in two phases at its Xinjiang polysilicon facilities in the past months. These initiatives helped to improve production, expand hydrochlorination capacity and enhance manufacturing efficiency. Additionally, a new Phase 3B expansion plan has been approved to enhance polysilicon annual production capacity by 38.9% to 25,000 MT for the company’s Xinjiang facilities. Also, additional efforts at these facilities are anticipated to raise the annual production capacity to 30,000 MT by 2019. The company expects that enhanced production capacity will cater to the demand from mono-crystalline wafer and semiconductor markets.

Moreover, increasing annual solar PV installation in countries like China, the United States, India and Japan have created healthy demand environment for the company. Notably, annual solar PV installation in 2017 is likely to be approximately 50 GW in China, 12 GW in the United States and 10 GW in India while a double-digit growth is predicted globally.

For 2017, Daqo New Energy anticipates to produce roughly 4,800-5,000 MT of polysilicon while sales to external customers are predicted to be within 4,300-4,500 MT.

The stocks’ Zacks Consensus Estimate currently stands at $7.81 for 2017 and $5.76 for 2018, representing 18.5% and 11.6% increase over their respective estimates 30 days ago.

DAQO New Energy Corp. Price and Consensus

DAQO New Energy Corp. Price and Consensus | DAQO New Energy Corp. Quote

Other Stocks to Consider

Daqo New Energy has a market capitalization of approximately $453 million. Other stocks worth considering in the industry include Kraton Corporation (NYSE:KRA) , Ferro Corporation (NYSE:FOE) and International Flavors & Fragrances Inc. (NYSE:IFF) . While Kraton sports a Zacks Rank #1, Ferro and International Flavors & Fragrances carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Kraton Corporation’s earnings estimates for 2017 and 2018 improved over the last 60 days. Also, the company pulled off an average positive earnings surprise of 32.88% in the trailing four quarters.

Ferro Corporation delivered a positive average earnings surprise of 17.79% in the last four quarters. Its earnings estimates for 2017 and 2018 were revised upward over the past 60 days.

International Flavors & Fragrances witnessed upward earnings estimate revisions for 2017 and 2018, over the past 60 days. The company delivered an average positive earnings surprise of 3.05% in the trailing four quarters.

Wall Street’s Next Amazon (NASDAQ:AMZN)

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Kraton Corporation (KRA): Free Stock Analysis Report

Ferro Corporation (FOE): Free Stock Analysis Report

DAQO New Energy Corp. (DQ): Free Stock Analysis Report

Internationa Flavors & Fragrances, Inc. (IFF): Free Stock Analysis Report

Original post

Zacks Investment Research