Just when you thought it was safe to get back into the water, along comes a particular wave that sideswipes you and takes you out of the game. The weaker of the dollar bulls were forcibly pushed out in the FX twilight zone – the most illiquid of time zones, the US/Australasia hand over last night. ‘Helicopter’ Bernanke said in response to a question after a speech in Massachusetts that highly “accommodative monetary policy for the foreseeable future is what is needed in the US economy”. The market started to firm as soon as Bernanke began to take questions. He opened by characterizing the US unemployment rate as perhaps “overstating” the strength of the economy and cited that the low US participation rates as perhaps a sign of “internal weakness”. More of a surprise was that he went out of his way to emphasize again the point that the +6.5% unemployment rate is “not a rate that will trigger tightening by itself”.

What was probably new to the markets after digesting his comments was the idea that he believes the current economy to be softer than data would indicate. The dollar, which had been rallying hard since May as markets braced for an early withdrawal of Fed stimulus, managed to pull back hard. Initial reaction saw it fall -3% against the EUR, -2% against Yen. The market has since seen a small dollar pull back which is normally blamed on the initial over exuberant move. EUR/USD" width="400" height="300">

EUR/USD" width="400" height="300">

The FOMC minutes, released earlier in the day, were consistent with September taper, hence, making the overnight fallout more urgent. According to minutes from the June 18-19 FOMC meeting, about half the participants figured it would be appropriate to bring asset purchases to a close late this year, while ‘many’ other participants felt it would be appropriate to continue purchases into 2014. That market interpreted this to be a relatively hawkish balance compared to the timeline Bernanke referred to in his post-FOMC meet press conference last month.

Many saw tapering beginning later this year and drawing to a close around mid-2014 as the US unemployment rate is expected to fall to +7.0%. The minutes also indicated that several voting members stressed the importance of both jobs growth and acceleration in the economy before tapering. Offline Fed rhetoric since the June meet has guided market expectations to September for the start of asset purchase tapering. This is still probably the most likely of scenarios, unless Bernanke changes the game plan at next weeks Semi-Annual Monetary Policy Testimony to the House and the Senate. What happened to all the transparency speaks?

US equities, which had previously been pegged back on fears that the market would be witnessing early withdrawal of stimulus, had also managed to rally sharply in the overnight session. The danger is that this market move may be excessive – what goes up, can come down just as quick! Despite the G10 rally being a big setback for the dollar bulls, the market move can “unravel,” but for now, few will want to stand in the way preferring to see a strong directional indicator before getting burnt again. USD/JPY" width="400" height="300">

USD/JPY" width="400" height="300">

Breaking the monotony of Bernanke’s speech and fallout last evening was the BoJ keeping QE unchanged and the Aussie job numbers surprising. The Japanese central bank kept its asset purchase targets and policy unchanged, in line with consensus expectations. The policy makers maintained their core-inflation forecast at +2.6% in 2015, but revised its 2013 and 2014 projection down a tad to +0.6% and +3.3% respectively. Their real GDP projections were also revised marginally lower versus the April forecasts. What was also interesting was that the Japanese investors bought foreign bonds for the first time in two-months (+¥973b). This follows seven-consecutive weeks of bond repatriation.

Down under, Aussie employment surprised strong on the part-time. The number of people employed rose +10.3k last month. The market was looking for an unchanged print. The gain was driven entirely by part-time, which rose +14.8k in June, while full-time employment declined by -4.4k. The unemployment rate ticked higher to 5.7% from 5.6%, due to a rise in the participation rate to 65.3% from 65.2%.

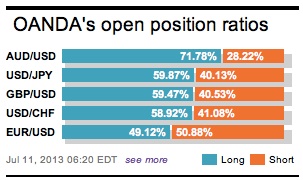

The overnight +3% EUR rally would suggest that this market was very long dollars. However, the latest IMM: FX data would dispel that thought. The aggressive overnight move has been fueled mostly by the action occurring in the most illiquid of time zones, the US/Aussie market handover – a cruel period of time that is infamous for stop-loss hunting. Bernanke’s slight of hand wronged long dollar positions, but not the rates market. The US 10-year benchmark yields a similar +2.56% while the German Bund/US is little changed at 98bps. This is certainly reason enough to fade the dollar mover lower, however, the magnitude of the loss will obviously affect individuals risk appetite. With no ammunition, the market will most likely slither away, lick their wounds and consolidate for the time being.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

For Now, Dollar Bulls Lick Their Wounds

Published 07/11/2013, 07:36 AM

Updated 07/09/2023, 06:31 AM

For Now, Dollar Bulls Lick Their Wounds

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.