Central banks will make a comeback this week, with four major ones deciding on their respective policies. Those are the FOMC, the BoE, the BoJ, and the SNB. Our own view is that market participants will pay more attention to the FOMC and the BoE, as the BoJ and the SNB are widely expected to stick to their dovish narratives. We also have the Canadian elections, as well as the preliminary PMIs for September from the Eurozone, the UK, and the US.

On Monday, we have no major data releases scheduled on the economic agenda. However, loonie traders may lock their gaze on the Canadian federal elections.

Seeking public approval for his handling of the pandemic, PM Justin Trudeau called for elections two year early. That said, Trudeau has struggled to explain why an early election during the worsening forth wave of the virus was a good idea, and thereby, saw his popularity shrinking.

With the opposition Conservative Party wanting to bring under control the massive spending of Trudeau’s government, a Conservative victory could also mean a slower economic recovery, which could result in market participants lowering their rate-hike expectations. So, in our view, a government switch in Canada could prove negative for the local currency.

On Tuesday, Chinese markets will stay closed due to the Mid-Autumn Festival.

As for the events and the data, during the Asian session we get the minutes of the latest RBA meeting, and later in the day, the US building permits and housing starts for August are due to be released.

With the RBA pushing the date for its next policy review from November 2021 to February 2022, we don’t expect to get much new information from the minutes. Therefore, we don’t expect the aussie to react much on this release. As far as the US data is concerned, building permits are forecast to have slid somewhat, but housing starts are expected to have inched slightly up.

On Wednesday, the spotlight is likely to turn to the FOMC monetary policy decision. This is one of the bigger meetings, which will be accompanied by updated economic projections and a new “dot plot/”

Following the weaker-than-expected August employment report, market participants scaled back their expectations that the Fed could indeed start tapering its QE purchases this year. However, a couple of weeks ago, several policymakers signaled that they still expect to begin the process before the end of this year, despite the slowdown in jobs growth seen in August, reviving hopes on that front.

What’s more, the CPIs for August slowed somewhat, but remained well above the Fed’s objective of 2%, keeping questions on whether the inflation surge is transitory, well on the table.

Thus, with that in mind, it would be interesting to see whether this is the opinion held by the majority of policymakers and whether there will be any strong clues on the possible timing of beginning the tapering process. In our view, anything pointing to a November tapering decision may support the US dollar further and perhaps extend the latest setback in equities.

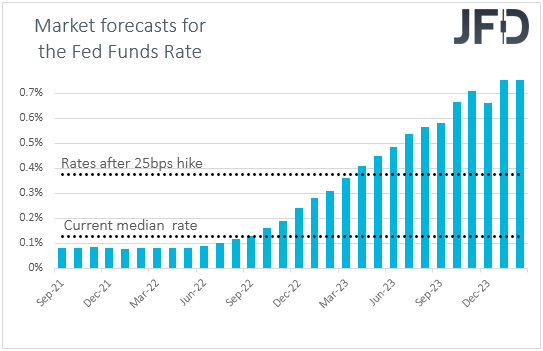

Market participants may also be eager to find out whether this could also result in earlier rate hikes. The June “dot plot” revealed that interest rates are likely to start rising in 2023, with 13 members seeing higher rates through that year, and the median dot sitting at 0.6%, which means two quarter-point hikes.

However, 7 officials saw at least one hike in 2022, and if that number grows, it could consist of another reason for more USD strengthening, and further retreat in stock indices.

Ahead of the Fed decision, we have another Bank deciding on monetary policy and this is the BoJ. The latest gathering of this Bank was back in July, with officials keeping their policy settings unchanged and noting that the risks to the Japanese economic outlook remain skewed to the downside.

The event passed unnoticed by JPY-traders, and we expect the same to happen this week as well. With inflation in Japan failing to catch up with the acceleration in other places of the globe, Japanese policymakers will most likely prefer to maintain their policy extra loose for longer.

As for the data, the only one worth mentioning is the US existing home sales for August, with the forecast pointing to a small decline.

On Thursday, the central bank torch will be passed to the SNB and the BoE. The SNB is widely expected to keep its policy unchanged and maintain its dovish stance, repeating that the Swiss franc remains highly valued and that they remain ready to intervene in the FX market when deemed necessary.

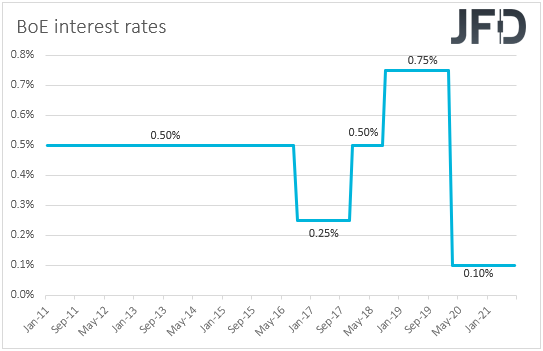

Therefore, all the attention may fall on the BoE decision. At their latest meeting, British policymakers lowered the threshold of when they will start reducing their stock of bonds. Specifically, they said that they will do so when the policy rate hits +0.50%, by not reinvesting the proceeds of maturing debt. The previous guidance was for the Bank to not start unwinding its bond purchases until interest rates were near +1.5%. In our view, this means that QE tapering may start earlier than previously anticipated.

Now, the big question is when the time would be appropriate for officials to start raising interest rates. A couple of weeks ago, BoE Governor Andrew Bailey revealed that, even at the prior gathering, policymakers were split evenly between those who felt the minimum conditions for raising interest rates were met and those who believed that the recovery was not strong enough.

This suggests that a rate hike could take place sooner than many may have been anticipating, and the accelerating inflation last week may have allowed market participants to increase their bets on that front. Therefore, it would be interesting to see whether we will get any clear hints or clues on when officials intend to start raising interest rates.

Recently, BoE MPC member Michael Saunders said that interest rates may need to start rising next year, a view which, if shared among other members as well, could held the pound march higher. At this point it is important to note that in an August Reuter’s poll, no change was expected until 2023.

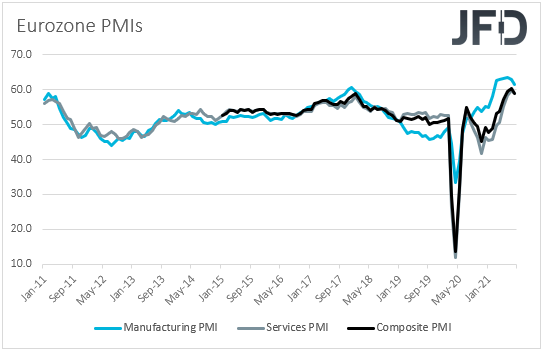

Besides the SNB and the BoE, we will also get the preliminary PMIs for September from the Eurozone, the UK, and the US. In the Eurozone, both the manufacturing and services indices are expected to have declined somewhat, to 60.5 and 58.7, from 60.8 and 59.0, respectively, which will take the composite index slightly down, to 58.8 from 59.0. Despite the slowdown, this will still reflect a decent pace of expansion, and thus, we don’t expect such results to weigh on the euro.

That said, deeper declines could raise questions as to whether the recovery seen after the reopening has reached a ceiling, and perhaps push the common currency lower. No forecast is available for the UK prints, while in the US, the manufacturing index is expected to have inched up to 61.5 from 61.1, and the services one to have ticked down to 55.0 from 55.1.

Finally, on Friday, during the Asian trading, Japan’s National CPIs for August are due to be released, but no forecast is available for neither the headline rate nor the core one.

During the EU session, the German Ifo survey for September is coming out, while later, from the US, we get the new home sales for August. With regards to the Ifo survey, the current assessment index is expected to have inched up to 101.8 from 101.4, while the expectations one is anticipated to have slid to 96.4 from 97.5. This is likely to take the business climate index down to 98.9 from 99.4. New home sales are expected to have increased fractionally.