Equities traded generally higher yesterday, while the US dollar was found lower this morning against its major counterparts, perhaps because, although the Fed acknowledge the economic progress towards its goals, at the press conference after the decision, Fed Chief Powell repeated its “long way to go” mantra. This may have disappointed those expecting to get hints over when policymakers are planning to start withdrawing monetary policy support.

US Dollar Slides, Equities Rebound As Powell Gives No Signal On Tapering

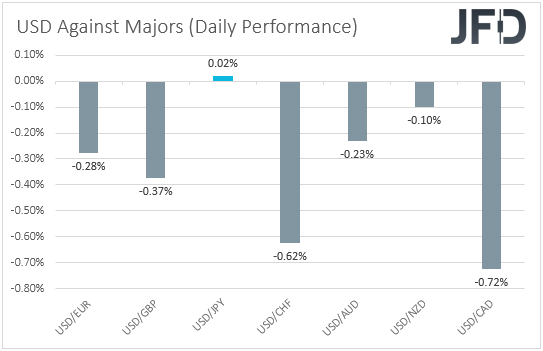

The US dollar traded lower against all but one of the other major currencies on Wednesday and during the Asian morning Thursday. It lost the most ground versus CAD, CHF, and GBP, in that order, while it was found virtually unchanged against JPY.

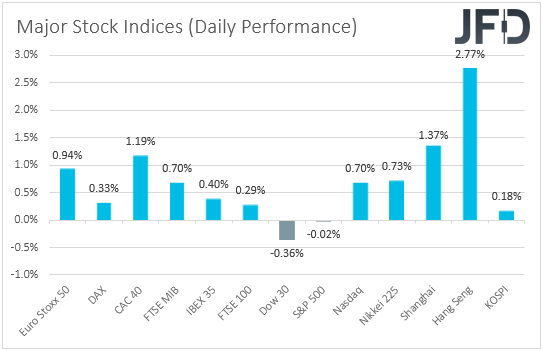

The weakening of the US dollar and the Japanese yen, combined with the fact that the main gainer was the risk-linked Loonie, suggests that the financial world traded in a risk-on manner yesterday and today in Asia. The only variable that does not fit the equation is the depreciation of the Swiss franc, otherwise called a safe haven. In any case, turning our gaze to the equity world, we see that major EU indices traded in the green, and although Wall Street’s Dow Jones and S&P 500 failed to gain, NASDAQ edged 0.70% up, with market sentiment improving further during the Asian session today.

Yesterday, ahead of the FOMC decision, EU shares traded higher, perhaps due to encouraging earnings reports, which may have helped investors look past worries about the tightening regulations in China. Nonetheless, investors in the US did not join the party, perhaps due to the Fed’s relatively hawkish statement. The Committee kept its policy unchanged, but although they repeated that they will keep the pace of their QE purchases unchanged until “substantial further progress has been made” towards their goals, they added that the economy has made such progress, and that they will continue to assess the progress in coming meetings.

Investors may have translated this into willingness to start withdrawing support sooner than previously assumed, and that’s why they slightly reduced their risk exposure. Having said all that though, at the press conference following the decision, Fed Chief Powell said that the labor market has still a long way to go, and that inflation is still expected to fall back to their longer-run goals. He also added that the timing of taper will depend on incoming data and that they will provide advance notice before any changes. This poured cold water on expectations of an early tightening, which may have been the reason why the dollar fell, and equities rebounded during the Asian session.

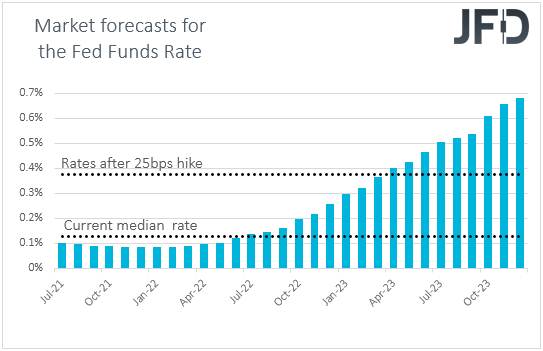

The next FOMC gathering is scheduled for late September and taking into account that we did not get any advance notice yesterday, the earliest policymakers could start scaling back QE is in November or December. And all this, conditional upon further notable strength in the labor market.

As for our view, with Powell refraining from fueling tapering expectations, the dollar may stay under selling interest for a while more, while equities could keep drifting north, also aided by encouraging earnings. The employment reports are now likely to be of more importance than previously, as possible setbacks could push expectations over a potential tapering into next year. Rate-hike expectations could also be pushed back, although they have not changed much after yesterday’s outcome. Still, investors anticipate the first 25bps increase to happen around March or April 2023.

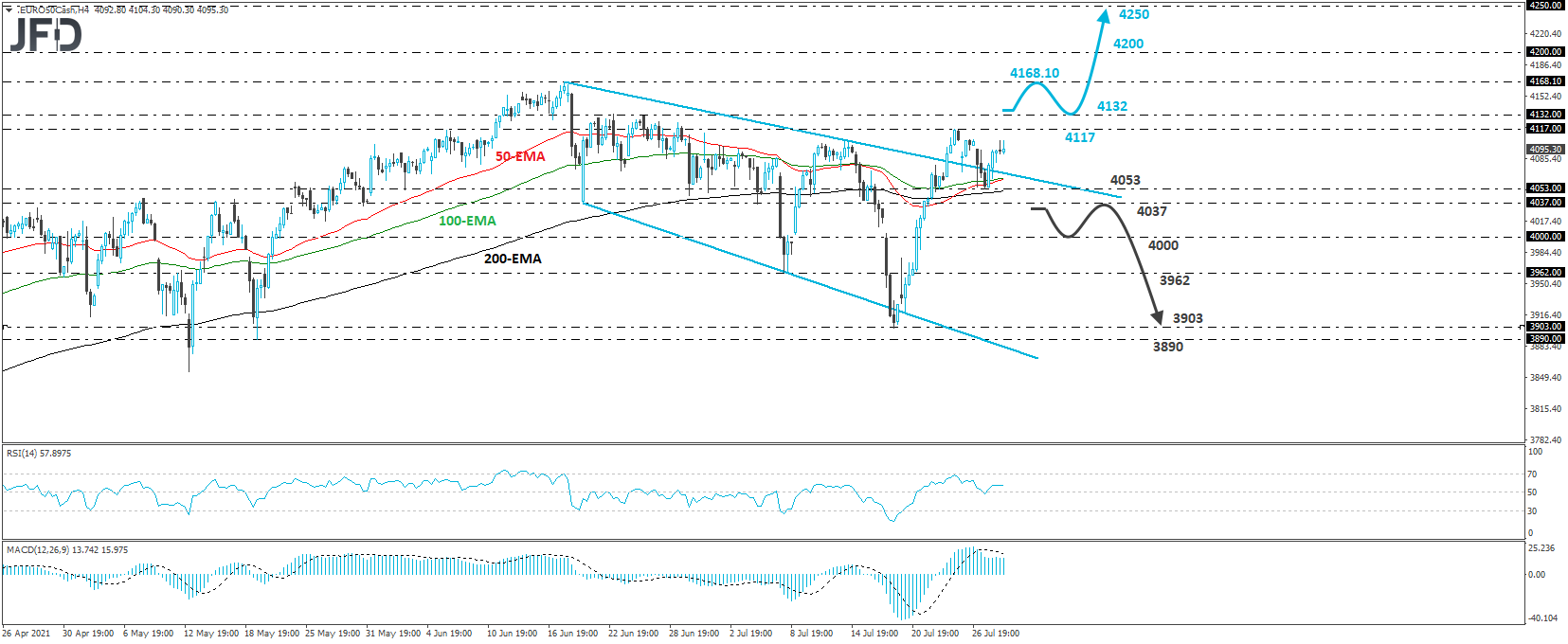

EURO STOXX 50 Technical Outlook

The Euro STOXX 50 cash index traded higher yesterday, breaking back above the downside resistance line drawn from the high of June 17. In our view, this paints a cautiously positive picture, but in order to get confident on more advances, we would like to see a break above the peak of July 23, at 4117, or even better, the 4132 zone, which provided strong resistance between June 22 and 25.

If we do see such a break, then investors may drive the action back to the index’s all-time high, at 4168.10, hit on June 17. If they don’t stop there and decide to take Euro STOXX into uncharted territory, we will mark as potential upcoming resistance zones, the 4200 and 4250 levels.

On the downside, we would like to see a dip below 4037 before we abandon the bullish case. This may confirm the price’s return back below the aforementioned downside line and may initially target the round figure of 4000. A break below that number may see scope for declines toward the 3962 barrier, marked by the low of July 8, the break of which could set the stage for the low of July 19, at 3903.

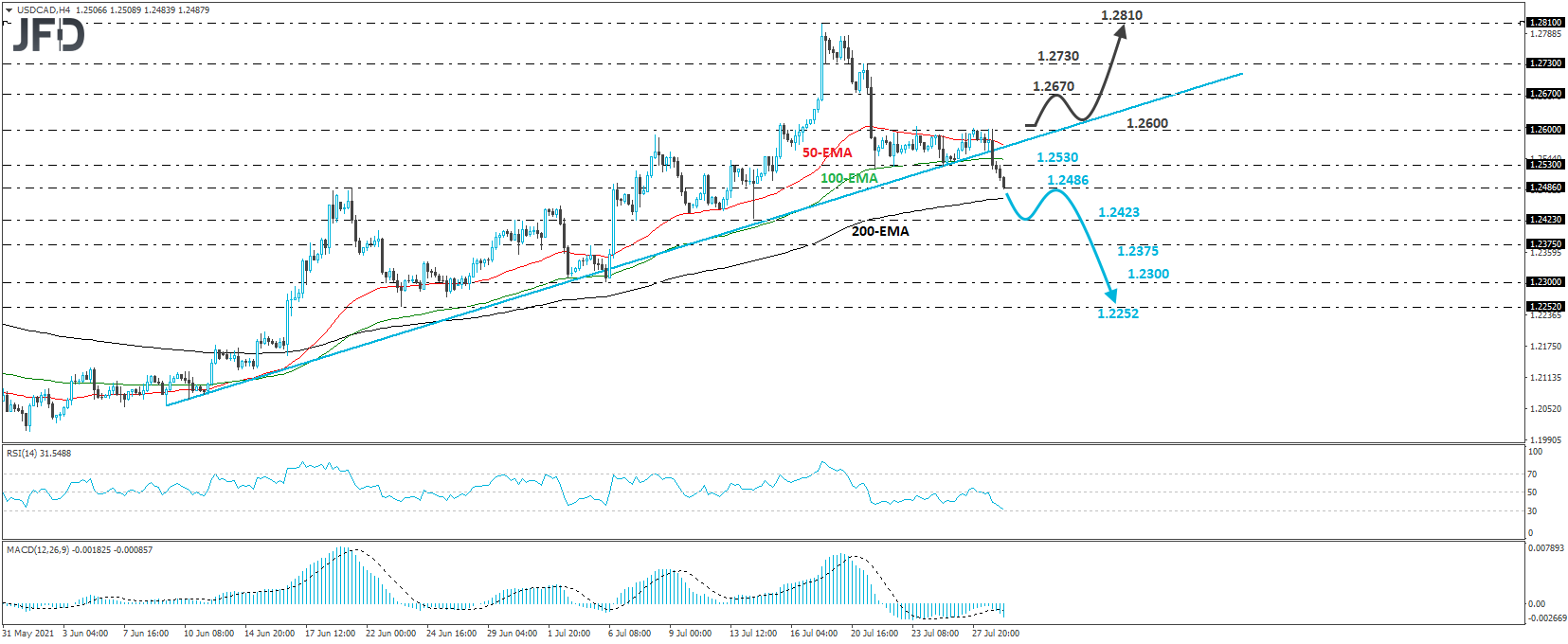

USD/CAD Technical Outlook

USD/CAD edged south yesterday, breaking below the upside support line drawn from the low of June 9, as well as the 1.2530 zone, which was providing decent support since July 21. This confirmed a forthcoming lower low on the 4-hour chart and, in our view, turned the short-term outlook to the downside.

At the time of writing, the rate is trading near the 1.2486 support, where a break may extend the slide towards the low of July 14, at around 1.2423. If that barrier doesn’t hold, then the next stop may be at 1.2375, marked by the inside swing high of July 5. Another break, below 1.2375, could pave the way towards the low of the day after, at around 1.2300.

Now, in order to turn our eyes back to the upside, we would like to see a rebound back above 1.2600, which acted as a strong resistance between July 22 and yesterday. Such a move may also signal the rate’s return above the aforementioned upside line and may carry advances towards the 1.2670 or 1.2730 barriers, marked by the low and the high of July 21. Slightly higher lies the peak of July 19, at 1.2810, which could also get tested. This is the highest point since Feb. 5.

As For Today's Events

Today, we get Germany’s preliminary inflation data for the July, with both the CPI and HICP yoy rates expected to have surged to +3.3% yoy and +2.9% yoy, from +2.3% from +2.1% respectively. This is likely to raise bets that Eurozone’s headline inflation print, due out tomorrow, may also accelerate notably. The 1st estimate of the US GDP for Q2 is also coming out, and the forecast points to a rising growth rate, to +8.5% qoq SAAR from +6.4%.