The US dollar strengthened while equities slid further yesterday, as the minutes from the latest FOMC meeting revealed that a number of policymakers thought that if the recovery continues, it may be appropriate to “begin discussing a plan for adjusting the pace of asset purchases.”

With that in mind, it would be even more interesting to hear what Fed officials have to say moving forward, especially after the surge in consumer prices for April.

USD Up, Equities Slide As Fed Looks To Taper

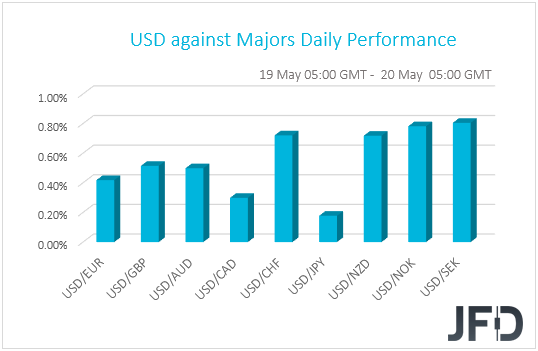

The US dollar traded higher against all the other G10 currencies on Wednesday and during the Asian session Thursday. It gained the most versus SEK, NOK, CHF, and NZD, in that order, while it eked out the least gains against JPY.

The strengthening of the US dollar, combined with the weakening of the oil-related Krone and the risk-linked Kiwi, as well as the relative strength of the safe-haven yen, suggests that markets traded in a risk-off fashion yesterday and today in Asia.

That said, the weakening of the Swiss franc points otherwise and thus, in order to get a clearer picture with regards to the broader market sentiment, we prefer to turn our gaze to the equity world.

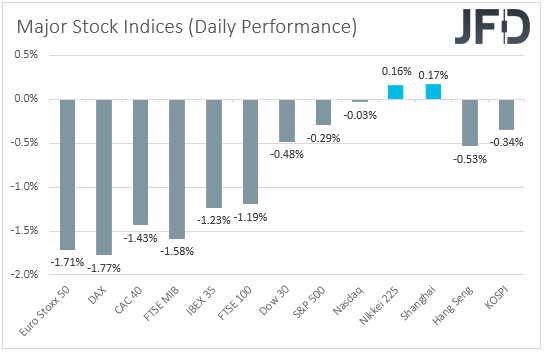

There, major EU and US indices were a sea of red. Appetite was mixed today in Asia. Japan’s Nikkei 225 and China’s Shanghai Composite gained 0.16% and 0.17% respectively, while Hong Kong’s Hang Seng and South Korea’s KOSPI slid 0.53% and 0.34%.

European shares experienced their worst day in a week, perhaps as investors remained concerned over high inflation, after data from the UK showed that the yoy rate of headline consumer prices more than doubled in April.

Later in the day, what may have kept investors on the defensive was the release of the minutes from the latest FOMC gathering. Although, after that meeting, Fed Chair Jerome Powell noted that it is still too early to start discussing withdrawing policy support, the minutes revealed that a number of policymakers thought that if the recovery continues, it may be appropriate to “begin discussing a plan for adjusting the pace of asset purchases.”

Given that the minutes refer to a date before the latest CPI data, it would be even more interesting now to hear what Fed officials have to say moving forward.

The minutes revealed that there was no consensus in the view expressed by Fed Chief Powell and some other Fed officials thereafter, and following the more-than-anticipated surge in US inflation, more members may have been convinced that a discussion over tapering should take place.

In our view, all this increases the importance of the upcoming jobs report, as stellar employment gains may add to speculation that such a discussion may take an official form at the upcoming gathering.

For now, equities and other risk-linked assets are likely to stay under pressure for a while more, while the US dollar and other safe-havens may gain some support.

For that to change, upcoming Fed officials may have to reiterate the view that the current inflation spike is likely to prove to be temporary, and that it is still too early to start discussing policy normalization.

DJIA Technical Outlook

The Dow Jones Industrial Average cash index traded lower yesterday, but hit support at 33475 and then it rebounded to hit resistance at 33930.

Although the index continues to trade above the upside support line drawn from the low of Jan. 31, it is also trading below a new short-term downside line taken from the high of May 10. Given also that the index is well above the former line, we would see decent chances for further downside correction.

If the bears are willing to take charge from near the 33930 barrier, or even the aforementioned downside line, we could see a retreat back near the 33475 zone, where a break may extend the slide towards the low of May 13, at 33285.

If that area is not able to halt the decline either, then its break may set the stage for the 32970 territory, defined as a support by the lows of Mar. 31 and Apr. 1.

Now, in order to start examining the bullish case again, we would like to see a strong recovery back above 34170. This would also place the Dow above the short-term downside line and may initially pave the way towards the 34500 area, near Tuesday’s peak.

If that obstacle is also broken, then the advance may continue towards the all-time high of 35092, hit on May 10.

NZD/USD Technical Outlook

NZD/USD tumbled yesterday, breaking below the upside support line drawn from the low of Apr 1. However, the rate hit support at 0.7150, and then it rebounded.

Overall though, the pair continues to trade below the upside support line and thus, it would be interesting to see whether the bears will jump back into the action soon.

If so, we may see them aiming for another test at 0.7150, the break of which would confirm a forthcoming lower low on the 4-hour chart and may aim for the low of May 4, at 0.7115.

Another break, below 0.7115 could carry larger bearish implications, perhaps setting the stage for the 0.7070 hurdle, defined as a support by the inside swing highs of Apr. 5 and 6.

On the upside, we would like to see the recovery taking the rate back above the pre-mentioned upside line before we get somewhat confident on the resumption of the prior uptrend.

Such a move may encourage the bulls to push the action towards the 0.7255 zone, where another break may see scope for advances towards the peak of May 11, at 0.7290, or the high of the day before, at 0.7305.

As For Today's Events

During the Asian morning, we got Australia’s employment report for April. Although the unemployment rate slid to 5.5% from an upwardly revised 5.7%, the employment change revealed that the economy has lost 30.6k jobs after adding 77.0k in March. The consensus was for a slowdown to 15.0k.

Following Tuesday’s RBA minutes, which confirmed officials’ concerns over low inflation, as well as that wage growth remained subdued during Q1, April’s job losses may have increased the chances for the RBA to proceed with more bond purchases at the July meeting.

Later in the day, the only release worth mentioning is the US initial jobless claims for last week, which are expected to have declined to 450k from 473k.

During the Asian session on Friday, we have Japan’s National CPIs for April. No forecast is available for the headline rate, while the core one is expected to have ticked down to -0.2% yoy from -0.1%.

As for the speakers, we have four on today’s agenda and those are ECB President Christine Lagarde, ECB Executive Board member Philip Lane, BoE MPC member Jon Cunliffe, and BoC Governor Tiff Macklem.