The US dollar stayed supported against most of the other major currencies yesterday and today in Asia, with most equity indices finishing another session in the red. It seems that investors are still concerned over the coronavirus and its new variant, but they may have also stayed careful ahead of the FOMC decision.

Market Sentiment Stays Soft Ahead of FOMC Decision

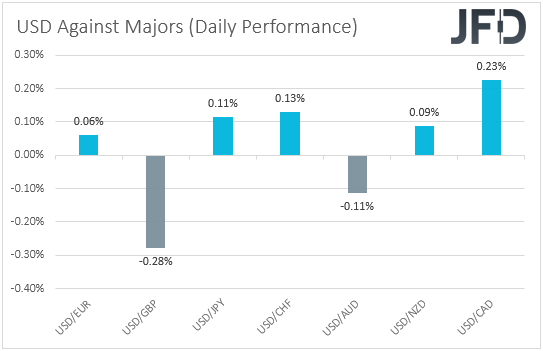

The US dollar traded higher against all but two of the other major currencies on Tuesday and during the Asian session today. It gained ground against CAD, CHF, JPY, NZD, and EUR in that order, while it underperformed versus GBP and AUD.

The strengthening of the dollar and the weakening of the Loonie and Kiwi suggest that markets continued to trade in a risk-off manner. However, the weakening of the yen and franc, combined with the strengthening of the Aussie and the pound, points otherwise.

Therefore, to clarify the broader market sentiment, we prefer to turn our gaze to the equity world. There, most major EU indices continued to slide, with the exceptions being Italy’s FTSE MIB and Spain’s IBEX 35, while all three of Wall Street’s leading indices finished lower. NASDAQ lost the most ground. Appetite stayed soft during the Asian session today as well.

With no new clear catalyst to drive the markets yesterday, we believe that investors may have continued reducing their risk exposures due to fresh concerns over the Omicron coronavirus variant after the UK reported the first death from the strain. Still, also due to expectations over a hawkish Fed later today, especially after data yesterday showed that the US PPIs accelerated by more than anticipated in November, with both the headline and core rates hitting fresh record highs.

A couple of weeks ago, Fed Chair Jerome Powell appeared hawkish before the US Congress, saying that he and his colleagues may need to drop the “transitory” wording regarding inflation from their statement and accelerate the pace of their QE tapering process.

Thus, given that these are the changes already anticipated for today, if indeed delivered, they are unlikely to be the leading cause of market volatility. We believe that this may be the Committee’s updated economic projections, or otherwise the new “dot plot.”

According to the Fed funds futures, market participants believe that US policymakers will deliver their first post-pandemic quarter-point hike in July next year while a factor in another one by the end of the year. Therefore, with that in mind, we believe that the new plot needs to point to two or more interest-rate hikes for 2022 for the US dollar to keep strengthening.

As for the equities, bearing in mind how investors behave ahead of the decision, we believe that a steeper rate path could result in further selling, as higher rates sooner mean higher borrowing costs for companies, as well as lower present values.

NASDAQ 100 – Technical Outlook

The NASDAQ 100 cash index traded lower on Monday and Tuesday, after hitting resistance once again near the critical barrier of 16430, which has been acting as a temporary ceiling since Nov. 25. The price fell below the 16130 zone, which marks the low of Dec. 9 and 10, thereby completing a short-term double top, and thus, although the slide was stopped at 15735, we see decent chances for another round of selling.

A dip below 15735 could confirm that and perhaps allow declines towards the low of Dec. 3, at 15535, the break of which could carry extensions towards the 15310 zone, which provided support between Oct. 21 and 25. Another break, below 15310, could see scope for extensions towards the low of Oct. 18, at 15055.

On the upside, we would like to see a clear rebound above the aforementioned key resistance of 16430 before we start examining whether market participants have become more optimistic. This could pave the way towards the index’s record high of 16770, hit on Nov. 22, the break of which could aim for the psychological round figure of 17000. Another break, above 17000, may allow extensions towards the 17200 zone.

EUR/USD – Technical Outlook

EUR/USD traded lower after hitting resistance at 1.1325. However, the slide was stopped again near the 1.1260 territory, which has been acting as the lower bound of the short-term sideways range the pair has been trading within since Nov. 26.

In the bigger picture, though, EUR/USD is still trading below the downside resistance line taken from the high of May 25, and thus, we would see more chances for the rate to exit the sideways range to the downside rather than to the upside.

A clear and decisive break below 1.1260 could, this time, encourage the bears to dive towards the low of Nov. 24, at 1.1185. If they are unwilling to stop there, a break lower would confirm a forthcoming lower low on the daily chart and perhaps set the stage for declines towards the 1.1100 territory, defined as a support by the low of Jun. 1, 2020.

On the upside, a break above the upper bound of the aforementioned range, at 1.1375, could invite more bulls into the action, but it will not be a trend reversal signal in our view, as the pair would still be trading below the longer-term downside line. We could see advances towards the 1.1432 level, or the 1.1465 zone, or even the downside line taken from the high of May 25.

As for the Rest of Today’s Events

During the early European morning, we already got the UK CPIs for November, with both the headline and core rates rising by more than anticipated. However, the pound added only 15 pips at the time of the release, perhaps as market participants are convinced that the latest COVID-related restrictions in the UK will keep the BoE’s hands off the hike button on Thursday.

Later in the day, ahead of the FOMC decision, we have the US retail sales and Canada’s CPIs, both for November. In the US, both the headline and core sales are expected to have slowed, while in Canada, the headline rate is forecast to have held steady at +4.7% YoY, and the core one to have slid to +3.6%.

Tonight, during the early Asian morning, New Zealand releases its Q3 GDP, while a few hours later, we get Australia’s employment report for November.