The USD falls today as investors unwound long bets on the currency, anticipating the Federal Reserve may slow the pace of interest rate hikes after this week's meeting.

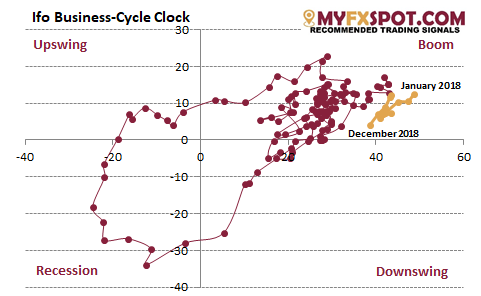

The EUR/USD is likely to gain further to the 1.1516 Fibo, a 50% retrace of the 1.1815 to 1.1216 (September to November) drop. We keep our bullish EUR/USD outlook despite weak German Ifo index. It showed that German economy was on the edge of downswing in December. In our opinion this should not halt EUR/USD rises, because domestic demand should keep German economy afloat in 2019.

The Ifo index in December declined strongly to 101.0 from 102. It was the fourth consecutive monthly decrease and the lowest level since September 2016. Especially the business expectations component deteriorated further to 97.3 from 98.7. The current assessment reading also declined to 104.7 from 105.5.

There is no denying in that the latest business sentiment indicators were worse than expected. The forward-looking business expectations component, our favorite early-bird indicator, declined strongly for the fifth month in a row and hit its lowest level in four years. Especially the export-dependent manufacturing sector took a heavy knock. At year-end 2018, the number of pessimists among business managers was larger than the number of optimists.

Given the latest deterioration, it is important to remain level-headed. To be sure, one should track sentiment indicators closely these days, since both economic and political risks have been rising. However, we think that special circumstances still argue for a rebound in the German economy anytime soon. More important, fundamentals speak against a doom and gloom scenario in 2019. While the signs of weaker momentum are obvious, one should keep a sense of proportion. GDP growth of at least 1.5% next year still seems feasible.

After shrinking economic activity in the third quarter of 2018, many investors have been discussing recession risks. The latest Ifo figures are certainly grist to the mill of growth pessimists. However, as being said previously, we think that the likelihood for a second consecutive quarter in which the German economy shifts into reverse gear is low.

Industrial production in October disappointed. However, this does not call the rebound itself into question. It just needs more time to unfold, as underlying momentum has started building. New orders in the auto sector were nearly 5% above the level in the third quarter. By the way, the latest Ifo business sentiment data for car manufacturers in December also showed a rebound. Business expectations even hit their highest level since the start of 2018.

It is reasonable to assume that private consumer expenditures will continue to grow solidly in the light of sound fundamentals as a further recovery on the labor market and significant wage hikes. Just to give two (backward-looking) figures for the first three quarters of 2018: about 350k jobs liable to social security contributions were created; wages increased by nearly 3% YoY.

What is more, we think that the boom in the construction sector will continue. Despite the recent ramping up of production activities, there is still huge excess demand for houses and condominiums from previous years. The upswing will therefore run its course further.

Fiscal policy should support GDP growth. According to a recent estimate of the German Council of Economic Experts, the growth impulse from fiscal policy could be up to 0.5pp in 2019. Huge fiscal surpluses, the need to spend more money and political considerations among policymakers in the grand coalition play an important role. 2019 is likely to see a paradigm shift in German fiscal policy, a largely underestimated pattern.

The bottom line is that one should not get too pessimistic. While the risks to exports, and hence also to capex spending, are undeniable, domestic demand will keep the economy afloat.