ADP Report on U.S. private sector employment impressed EUR/USD bears more than Fed's hawkish rhetoric

There was a time when the Fed’s hawkish rhetoric and a surge in the Treasury yield resulted in EUR/USD drop by a figure or a figure and a half. Alas, but close end of the U.S. economic cycle and inclusion of the Fed’s aggressive monetary restriction factor into the quotes of dollar pairs made investors far more careful. The Federal Reserve in its accompanying statement after the central bank’s meeting on July 31-August 1 has mentioned the word “strong”, related to the U.S. economy and the labor market, six times; but the major currency pair hasn’t lost even a half of a figure. And that is in the context of 10-year Treasury yield surge above the psychologically important level of 3% for the first time since June!

According to Citigroup, the Fed sounded more hawkish than at the previous FOMC meeting and clearly suggested the federal funds rate hike in September. The derivative market gives 91% probability of this scenario. The chances for four monetary restrictions in 2018 are up to 70%. The central bank’s willingness to continue normalizing its monetary policy and the Treasury minister’s intention to increase the bond issuance up to $329 billion in the third quarter and to $440 billion in the fourth one pushed 10-year Treasury yield up. The securities holders were selling the notes in the secondary markets in order to enter the market at more beneficial rates at auctions.

Remember, in addition to the gaps in economic growth and monetary policies, dollar benefited from trade war escalation in April-June period. In this respect, the rumors about an increase in the tariffs from 10% up to 25% on Chinese imports worth $200 billion were seen as another round of trade the U.S. trade wars. Washington claims that Beijing, with its retaliatory $34-billion, tariffs has just left it no choice. In fact, the reasons are much deeper.

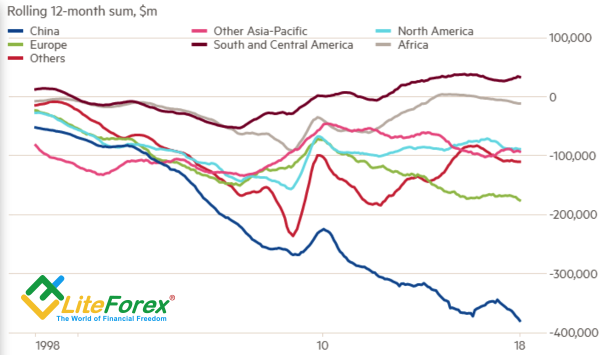

Dynamics of U.S. trade imbalance

Source: Financial Times

First, Steve Mnuchin’s negotiations with China’s officials are not as easy as the White House would like. Second, the USA is obviously annoyed by yuan devaluation; it has been 6% down against the US dollar since early June. This fact compensates the effect of the import tariffs and makes one consider increasing them. It is remarkable that more retaliatory measures slow down China’s economy growth and weaken PBOC monetary policy. Both factors are bullish for USD/CNY. They allow Deutsche Bank to increase its forecast for the pair from 6.8 up to 6.95 in late 2018. In 2019, the bank expects the pair quotes to be up at 7.4. So, Washington is responsible for the current situation, but it doesn’t see that far. Or doesn’t want to see.

After the FOMC meeting, investors are focused on the U.S. employment report. The highest increase in the U.S. private sector employment, reported by ADP, impressed investors stronger than the Fed’s hawkish rhetoric. +241,000 suggest that unemployment rate can well go down, and inflation -up. Will non-farm payrolls and other indicators be the signals, driving EUR/USD outside the short-term trading range at 1.1595-1.1745?