China’s economy may not suffer from the trade war as much as it is thought.

Any person is naturally selfish; however, when people love themselves too much, it looks ridiculous. It turns out that, when China is taking retaliatory measures in the trade war, it is taking the revenge against Donald Trump, rather than to the U.S., trying to influence the U.S. mid-term elections in November. Not that long ago, the U.S. president was threatening with the stock indexes crash in case on the impeachment, claiming that no other U.S. president during the past 100 years has ever managed to drive the GDP rate higher than that of unemployment. Actually, it has turned out that the time interval is 10 times shorter, but the U.S. president hasn’t become any less arrogant.

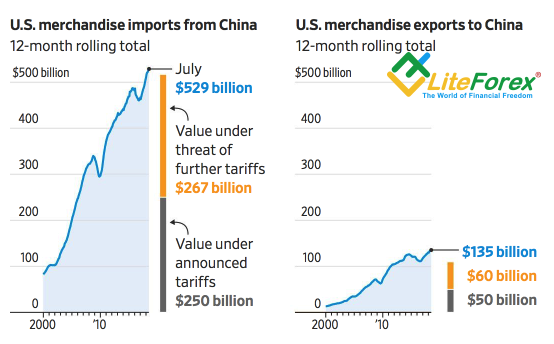

Beijing, as it was expected, has boosted its tariffs on the U.S imports by $60 billion, like the USA, suggesting a less amount of tariffs (10%-15%, instead of 25%, previously announced). Although Washington seems to have an advantage and can do nothing but impose the tariffs on all Chinese imports, time is on China’s side. The idea of $200-billion tariffs came up as early as in June, but they will come into effect only in late September. I don’t think that another $267 billion will be introduced until December. If China rejects the negotiations, proposed by Steven Mnuchin, it is obviously going to hold talks with some other people. With the Democrats, for example. So, there is some sense in Donald Trump’s speculation, but he clearly confuses the reasons and the results.

Imports and tariffs in the USA and China

Source: Wall Street Journal

The markets haven’t been that responsive to the news about the exchange of blows between the USA and China. Shanghai Composite was already 25% down from its January’s high, so the news about lowers tariffs, than it was expected, hasn’t allowed bears to go ahead. The PBOC has injected about $29 billion into the Chinese banking system, the greatest amount of liquidity for the last two months; and the Chinese Premier Li Keqiang has promised that Beijing won’t deliberately devalue the yuan. Fear makes the wolf bigger than he is. However, the trade war’s impact on the Chinese economy is not so disastrous as the media are trying to present. The share of export in China’s GDP is down to 18 in 2018, from 35% in 2006; the China’s exports to the US is only 4% of the China’s GDP.

I, personally, think that investors should pay more attention to the US economy’s outlook and the Fed’s activities. The markets are confident in four fed funds rate hikes in 2018 (CME derivatives suggest 87% probability of this scenario), and two more increases in 2019. But I have strong doubts that the U.S. fiscal stimulus will be able to support the U.S. 4-percent GDP rate next year. As a result, the yield curve is flattening and its correlation to the USD has been the closest since June,2017.

Dynamics of USD and the U.S. yield curve

Source: Bloomberg

According to BNY Mellon, a stronger correlation means that both the debt market and Forex are going to indicate when the U.S. current economic cycle will end.

The escalation of the U.S. trade battle with China hasn’t affected EUR/USD so much; until there are any new drivers, it will be taking a nap in the trading range of 1.15-1.185.