Some of the USD growth drivers stop working

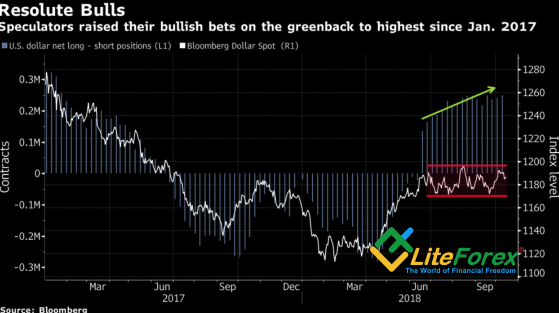

Donald Trump doesn’t cease criticizing the Fed; however, when he was appointing Jerome Powell for the office, the lawyer was the least evil. And Janet Yellen’s concerns about the U.S. inflation rate potential growth amid the lowest unemployment rate for almost five decades indicate that the U.S. president had made the right choice. If the “country teacher” were now the FOMC head, the Fed aggressive monetary restriction would become real. Powell weighs the recession risks and the economy overheating. After all, but the monetary normalization and the U.S. GDP steady growth still support the U.S. dollar. At the same time, as the other dollar advantages stop working, investors may start closing the U.S. dollar greatest net longs since early 2017

.

Dynamics of the U.S. dollar speculative positions and the USD rate

Source: Bloomberg

The drop in the U.S. stock indexes makes investors be extremely careful about investing in the U.S. equities. According to Barclays (LON:BARC), more and more people think 10-year Treasury yield at 3.15% to be too high; and the indicator will soon go down below 3%. This point of view is proved by the weak statistics on the U.S. retail sales and the U.S. inflation failure to move away from its 2% target. At the same time, the widest budget deficit for the past six years, $779 billion (+17% Y-o-Y) and the widening foreign trade deficit put pressure on the dollar. The first indicator is up at 3.9% from GDP in 2018 fiscal year, compared to the previous 3.5%. Last time when the U.S. unemployment rate was less than 4% (in 2000) the budget deficit was 2.3% from GDP; in 1969, (unemployment rate was at 3.7%), it was at 0.3%.

An important growth driver for the greenback in the April-October period was the capital repatriation amid the tax reform; however, its growth pace is down to $169.5 in the second quarter, compared to $294.9 in the first one. The fiscal stimulus effect is fading out, which may set back the U.S. economic expansion and correct the Fed monetary policy. The U.S. midterm election can put additional pressure on the dollar.

The major problem seems to be that no currency can catch up the falling flag. The Euro is pressed down by political problems and the European economy’s failure to recover and catch up after a week start in 2018. Even if the Italy’s finance minister Giovanni Tria is confident that he will justify the deficit of 2.4% from GDP for the European Commission and suggests the idea, that the presented figures will damage the entire Europe, to be irrational, there is still uncertainty. Brussels expressed its discontent even before the budget plan is presented; let’s see its response after the document is complete.

EUR/USD bulls still count on the increasing investors disappointment in the U.S. dollar. However, until there are any real euro advantages, the euro rate will hardly grow high. With this respect, I still suggest that the EUR/USD consolidation in the range of 1.145-1.18 will continue.