It will be difficult for China to equally retaliate to the U.S. new import tariffs, worth $200 billion

The U.S. trade war with China is not a war; it is a theater performance. You can come across this idea in the market, though, I, personally think it to be rather a poker game. Washington is raising the stakes, Beijing responds; China can do nothing but risk it all. China seems to have run out of guns rather quickly, as it imports a relatively less amount of the US products, worth $130 billion; but it disposes other tools. China may create obstacles to the foreign investors or even sell off the U.S. Treasuries. Finally, it looks like a poker game: it is difficult to see who is bluffing and who has got really good cards. Trump claims the evidence of winning the war to be stock indexes dynamics. China claims its economy to be strong enough to stand up the tariffs, worth 100% of China’s exports to the USA.

The market hasn’t been that responsive to the news about more tariffs, worth $200 billion. I can just wonder what is the reason for the yuan stability; whether it is Shanghai Composite or EURUSD; or, may be, the fact that everybody expected it and so, the news has been already included into the quotes; or, it may be a lower tariff of 10%, rather than the 25-percent duty, as it had been expected before; or it could be the time lag between the introduction of the tariffs and a slowdown in the Chinese economy. According to Citi, Donald Trump’s protectionism will press the China’s GDP rate 0.83 bps down in 2019. The China’s official announce a possible decline by 0.7 bps and are likely to retaliate with more tariffs on the U.S. imports, worth $60. Finally, the duties should cover about 85% of China’s imports from the USA.

The stakes in the U.S. trade war with China

Source: Bloomberg

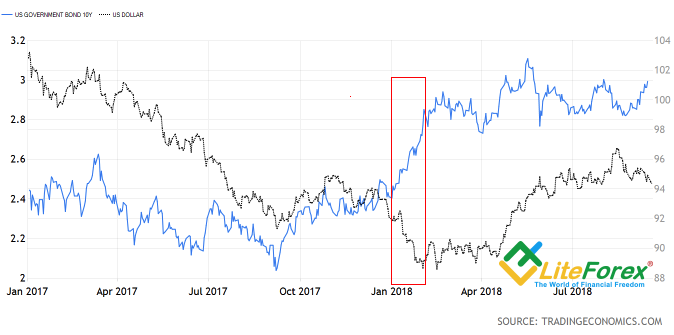

The China’s officials are unlikely to be scared off by Donald Trump’s threats to expand the import tariffs by another $267 billion. They can well deny the negotiations, proposed by Washington, in which the financial markets really believe in. If so, there will be the biggest trade war since the 1930s; its effect on the Forex price is more or less clear; until the China’s retaliatory measure set the U.S. economy back, the growth-gap will be pushing the USD up. As soon as there are any negative consequences, there will be massive sales of the greenback. Anyway, there may be changes in the scheme as well. For example, if China start selling off the U.S. Treasuries. The Treasury yield will be rising, but dollar won’t. Something like this was in early 2017, when the rumours that China was getting rid of the U.S securities were one of the drivers, pressing the U.S. dollar down.

Dynamics of the USD and Treasury yields

Source: Trading Economics

I believe, it looks like the situation in January. Many link the current 10-year yield increase to the soon FOMC meeting in September, where the Fed monetary policy should be tightened; however, remember how often the long-term bond yields used to surge ahead the Fed’s meetings. I wouldn’t say that the EURUSD increase above figure 17 base results from the principle “sell on rumours, buy on facts”. I think the euro still lacks growth drivers to exit the trading range of $1.15- $1.185.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

EUR/USD Dollar Crossed The Line

Published 09/18/2018, 05:29 AM

Updated 11/29/2020, 05:10 AM

EUR/USD Dollar Crossed The Line

Latest comments

All china can do to avert using the only available and nuclear option ( dumping US treasuries ) , is await midterm elections then move based on the outcome,,, its a bad strategy imo as they will have endured enough pain by then that any rash moves will send them in a race downhill with the US ( and rest of the world ) ,,

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.