- ECB’s Lagarde signals another 50bps hike in March

- BoE’s Bailey says inflation is turning the corner

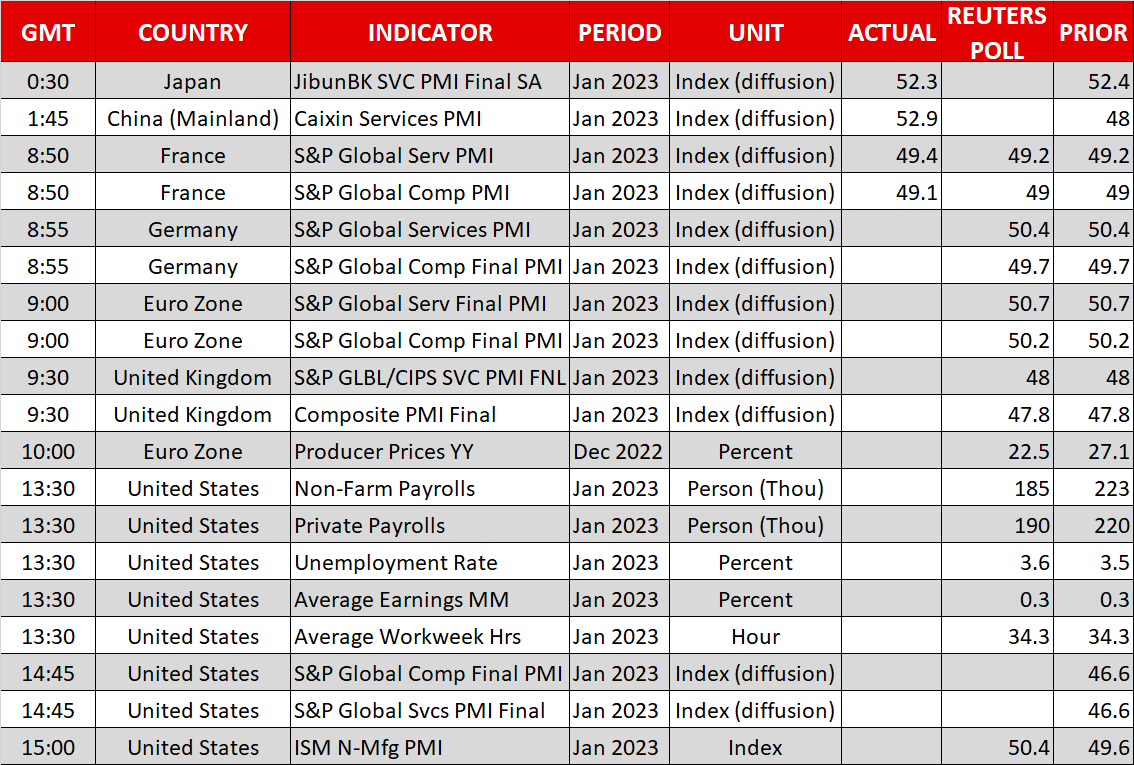

- Investors lock gaze on US jobs data

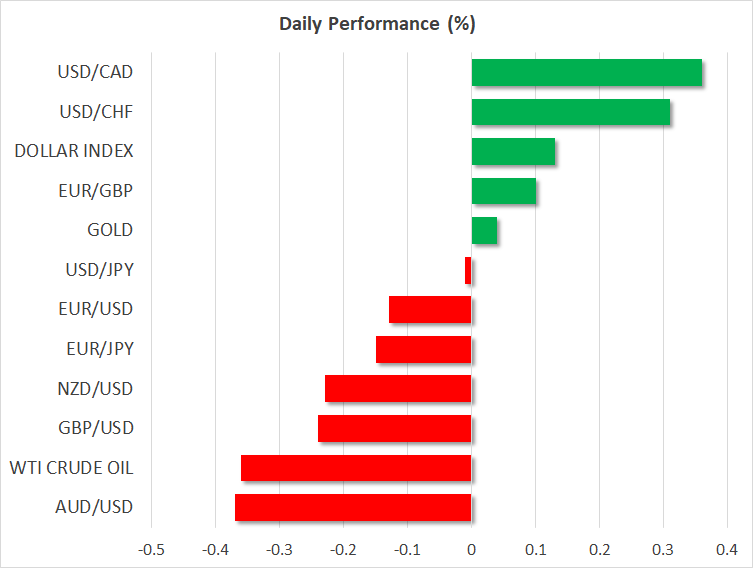

ECB President Lagarde appears in hawkish suit but euro slides

After the Fed, it was the turn of the ECB and the BoE to announce their monetary policy decisions yesterday. Both of them raised interest rates by 50bps as was widely expected but remarks by ECB President Lagarde and BoE Governor Bailey did not bode well for euro and pound traders.

Getting the ball rolling with Lagarde, she explicitly said that they intend to raise rates by another 50 basis points at the next meeting and then evaluate the path of interest rates on a meeting-by-meeting basis based on the data. She also added that supply bottlenecks are gradually easing, but the delayed effects are still pushing up goods price inflation.

Yet, despite Lagarde’s hawkish appearance, the euro slid. Market chatter suggests that investors may have interpreted her remarks as suggesting the tightening cycle is headed to an end. However, with market pricing still pointing to more than 75bps worth of rate hikes hereafter, the selling of the euro looks more like a “sell the fact” market reaction. President Lagarde sounded overly hawkish in Davos and thus, with no surprises yesterday, euro/dollar traders may have taken the opportunity to lock some profits, especially after the post-Fed rally.

Pound suffers as BoE Governor Bailey sees inflation turning the corner

Now passing the ball to the BoE, there was a change in the Bank’s forward guidance, with Governor Bailey saying that the change reflects a turning of the corner in the fight against inflation. Previously, the Bank said that it would “respond forcefully, as necessary”, but now they mentioned that further tightening would be required if there is evidence of more persistent price pressures.

With the UK expected to experience the worst recession among the major economies this year and market participants pricing in only another quarter-point hike by the BoE in this tightening crusade, the pound fell and may continue to suffer for a while longer. Due to similar expectations surrounding the Fed, pound/dollar may not be the best pair to reflect further weakness in the pound, but with the ECB still expected to proceed more aggressively than both the BoE and the Fed, euro/pound may be a better proxy.

Nonfarm payrolls the next big test for the dollar

Today, the financial community will likely turn its gaze to the US employment report for January. Nonfarm payrolls are forecast to have slowed to 185k from 223k in December, while the unemployment rate is anticipated to have ticked up to 3.6% from its five-decade low of 3.5%. Both numbers suggest a still-tight labor market, but with average hourly earnings expected to have slowed, investors may get more confident on a potential pivot by the Fed at some point this year, and thereby enter new short positions in the dollar.

Fed Chair Powell appeared less hawkish than expected on Wednesday, saying that the disinflationary process has started. Although he said that it will not be appropriate to cut rates this year, he added that if inflation comes down faster, that will be incorporated into their policy. This was another victory for investors, as Powell’s remarks added fuel to hopes that at one of the upcoming gatherings, they may eventually admit that rate reductions this year are a possibility.

Despite yesterday’s pullback, euro/dollar is still trading above the key support zone of 1.0800 and a potential rebound after today’s jobs data could well prompt traders to put the 1.1175 territory back on their radars. That zone is marked as resistance by the high of March 31, while it acted as support between November 2021 and February 2022.

Wall Street could also benefit as increasing pivot hopes could result in higher present values for high-growth firms that are valued based on discounted expected cash flows. That said, disappointing earnings results from tech giants Alphabet (NASDAQ:GOOGL), Apple (NASDAQ:AAPL) and Amazon (NASDAQ:AMZN) may evoke a lower opening today before any NFP-related buying pushes prices back up. A weekly close of the S&P 500 above the 4155 territory could brighten the technical picture, while the completion of a double bottom in the Nasdaq on Wednesday suggests that investors are not willing to abandon risky assets even with the likelihood of recession in the US firmly on the table. Maybe they are hoping that an eventual Fed pivot will also result in a soft landing of the economy.