EUR/USD: How to turn hawkish in a dovish way?

Macroeconomic overview: The ECB is widely expected to keep policy unchanged today, but important changes to ECB communication should be expected.

The new set of macroeconomic projections will help provide the analytical framework for this more constructive assessment. We expect the GDP forecasts to remain broadly unchanged compared to March, but for the third consecutive quarter, slight upward revisions look more likely than small downward adjustments, mainly due to encouraging developments in global trade. However, if upward revisions do materialize, they would only probably affect the first one-to-two quarters of the forecast horizon.

The inflation outlook is unlikely to materially depart from that envisaged in March either. If anything, risks are for a small downward revision to the near-term trajectory for headline inflation due to lower oil price assumptions. Changes at the policy-relevant horizon are unlikely because there the impact of exogenous variables tends to peter out and price dynamics are largely driven by domestic factors. ECB forecasts for core inflation in 2018-2019 are already quite aggressive and it is unlikely that any moderate upward revision to the growth projections would lead to an even stronger path for underlying price pressure.

Increased confidence in the recovery amid still slow progress on the inflation mandate will have implications for the ECB forward guidance. In particular, the Governing Council is likely to assess four important features of its guidance.

1. The easing bias on policy rates (“We [the Governing Council] continue to expect them to remain at present or lower levels for an extended period of time”); 2. The exit sequence, i.e. the time of QE-end vs. first rate increase; 3. The expected time lag between the end of QE and the first rate hike (“well past the horizon of our net asset purchases”); 4. The easing bias on asset purchases (we stand ready to increase our asset purchase program in terms of size and/or duration).

We think that the main changes will regard #1, with the ECB likely to drop the reference to the possibility of lower policy rates. The exit sequence is not written in stone, but will almost certainly be confirmed. And unless the side effects of negative rates significantly increase, the sequence will not change also in the future. #3 and #4 are trickier to call, but we tend to think that there will be no major changes.

First, if the ECB were to hint at a shorter time lag between the end of QE and the first rate increase, for example by changing the “well past the horizon” language into “past the horizon”, this would start giving an impulse to short-term rates, which the ECB seems unwilling to do at this stage.

Second, if the ECB drops the easing bias on asset purchases, the market may easily start speculating that QE may be reduced already before the end of the year. Instead, the ECB has often hinted they are on autopilot at EUR 60 billion per month until December 2017.

We do not expect the ECB to explicitly start talking down the EUR, but we know that ECB President Mario Draghi is a jawboning master and he certainly will not say anything that could strengthen the EUR. That is why we think there is a risk of a corrective move in the EUR/USD after today’s ECB meeting.

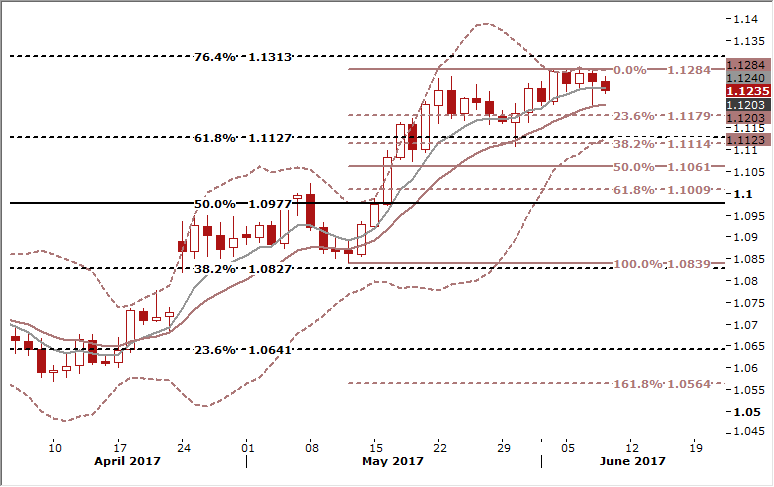

Technical analysis: Strong resistance in the 1.1280s may prove tough to break ahead of the key 1.1300 level. Pullbacks remain shallow so far and the bias is with the bulls. The situation may change after today’s ECB meeting.

Short-term signal: We think that a corrective move is likely in the coming days if the ECB statement is less hawkish than expected. We got short at 1.1235 for the target at 1.1070. But we think the EUR/USD pullback would be only temporary and our long-term outlook remains bullish.

Long-term outlook: Bullish

USD/CAD jumped on lower oil prices

Macroeconomic overview: The Canadian dollar weakened on Wednesday against its U.S. counterpart as oil prices tumbled.

Prices of oil, one of Canada's major exports, fell sharply on Wednesday after the U.S. government reported an unexpected rise in crude and gasoline inventories, which added to concerns that efforts to cut output by the world's biggest oil producers have not made enough impact.

Crude stocks in the United States grew 3.3 million barrels to 513 million barrels, according to the U.S. Energy Information Administration. That confounded forecasters who had predicted a drop of 3.5 million barrels, especially a day after data from the American Petroleum Institute indicated an even bigger fall.

Gasoline inventories also unexpectedly rose, imports increased, and exports dropped, the EIA data showed.

Some in the market remained concerned about the move by OPEC members Saudi Arabia and the United Arab Emirates to cut diplomatic and transport ties with Qatar, an OPEC member that had agreed to cut about 30k barrels a day as part of the Organization of the Petroleum Exporting Countries agreement to reduce output.

The Bank of Canada's review of developments in the financial system is scheduled for today, followed by a news conference with Governor Stephen Poloz. Investors will weigh Poloz's assessment of the housing and mortgage markets in light of recent troubles at non-bank lender Home Capital.

Technical analysis: The USD/CAD fluctuating between 61.8% fibo and 50% fibo of April-May rise, but is still away from 1.3575, which is a very strong resistance level. We think that improving risk sentiment should support the USD/CAD bears.

Short-term signal: Our sell order at 1.3510 was filled yesterday. The target is 1.3310.

Long-term outlook: We think that long-term outlook is slightly bearish now.

TRADING STRATEGIES SUMMARY:

FOREX - MAJOR PAIRS:

Source: GrowthAces.com - your daily forex trading strategies newsletter