The past few years have seen housing prices skyrocket as flippers, speculators and traditional buyers jump into home buying or selling to relocate to different areas throughout the U.S. One interesting facet of this phenomenon recently hit NBC news over the past few days related to the super-hot Boise, Idaho, and Coeur D'Alene, Idaho, markets. Home prices in the Boise area have skyrocketed higher by more than 30% in just 12 months. In Coeur D'Alene, home prices have risen more than 85% in the past 12 months.

Is Supply-Demand Measure Distorted By Recent Activity?

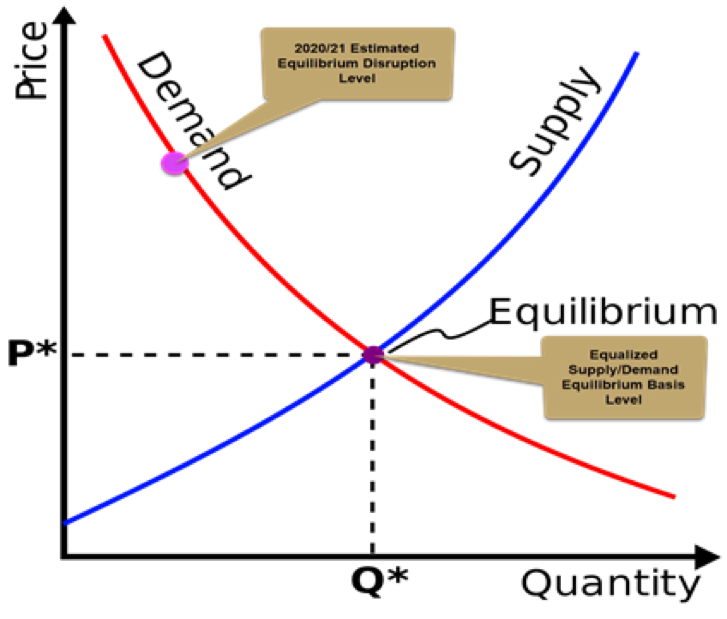

My concern is that the post-COVID buying/relocating trends have pushed the supply/demand pricing factors well past the equilibrium. Simply put, the moratoriums and policies related to home renters and homeowners throughout the COVID-19 crisis have created a supply crisis at a time when many people had the capabilities to sell and relocate into different areas of the U.S. at the same time. Diminishing supply with hyper-active demand pushes price levels upward and to the left, as illustrated on the supply/demand chart below.

The data and activity are supporting a hypothesis that speculators, flippers and homebuyers have chased the rising price levels well past a key equilibrium level, suggesting that a reversion process is very likely in the near future. This reversion event may be similar to the 2008-09 housing crisis as banks suddenly realize they've issued loans to borrowers at extremely high price levels with very little collateral to support these transactions. Or borrowers suddenly realize they are trapped in an overpriced home while the economy reverts to lower output levels. Either way, this seems like a receipt for some type of crisis in the making.

The four basic laws of supply and demand are simple to understand. Basically, the market is always seeking to maintain an equilibrium between buyers and sellers based on supply/demand factors. When extreme events take place to disrupt the equilibrium, these events unfold to push prices higher or lower depending on the event type. Eventually, as prices reach an extreme level, buyers and sellers begin to understand the extreme nature of the price disruption and a process of “reverting” will take place.

Price is always seeking to establish a proper equilibrium between demand and supply as buyers and sellers negotiate fair price levels for transactions. Once buyers or sellers believe the price levels are extreme, they typically become much more hesitant to engage in transactions because the risks become far too excessive as well. This is known as the Law of Supply and Demand, as seen below from Investopedia.

The biggest factor driving this substantial boom cycle is the relocation of people from cities to more rural areas. As COVID-19 hit, a big wave of people suddenly decided to give up their city life and move into more rural areas to avoid close proximity issues. The super low interest rates and the fact that the COVID-19 income disruptions were mostly related to entertainment, retail and restaurant workers prompted those with the capital means to take advantage of somewhat stagnant rural pricing (at the time). Now, about 14+ months later, home prices in these rural areas are rivalling, or beating, price values in some of the most prominent metropolises in the U.S.

This type of pricing activity throughout mostly rural areas seems very reminiscent of the 2005 to 2008 setup of the markets related to the market meltdown (housing/credit crisis) of 2008-09. We are starting to see similarities in the data that may suggest the current housing boom cycle is running on fumes right now (likely driven by speculators, flippers, and super low interest rates). Let's see what the data is showing us and you can draw your own conclusions.

MBA Purchase Index Data Shows Decidedly Lower Trends

The U.S. MBA Purchase Index includes all mortgage applications related to the purchase of single-family homes – covering both conventional and government loan types, and all products offered. This Index is an excellent indicator of demand and activity related to the total U.S. buying trends.

Since mid-February 2021, the MBA Purchase Index has broken downward after reaching what appears to be an excess peak in late 2020 and early 2021. My team and I believe this “rollover” in mortgage purchase activity is similar to the 2006~2007 decline in mortgage activity that happened just before the broad market collapse that took place in 2008-09 (see the left side of the US MBA Purchase Index chart below). Even though mortgage activity shown on this chart suggests that activity levels are peaking near 350 and have historically bottomed near 150, an extreme downturn in the current housing market trends could prompt a pullback closer to the 100 level as buyers pull away from a potentially dangerous real estate market price decline (reversion) event. Buyers of big ticket items, such as a house, tend to wait out big downturns – waiting for the best deals.

This downward trend in mortgage purchases aligns with the supply/demand theory that buyers are becoming hesitant to chase new purchases at these current extreme levels. Are there other data that point to a broader market slowdown in home sales? Do current price levels properly reflect a sufficient supply/demand equilibrium that allows for continued rising price levels?

It appears the housing bubble is starting to stall. What will it take to burst this bubble event? And is the Federal Reserve ready for it?